At what income level can you no longer deduct mortgage interest?

Isabella Wilson

Isabella Wilson

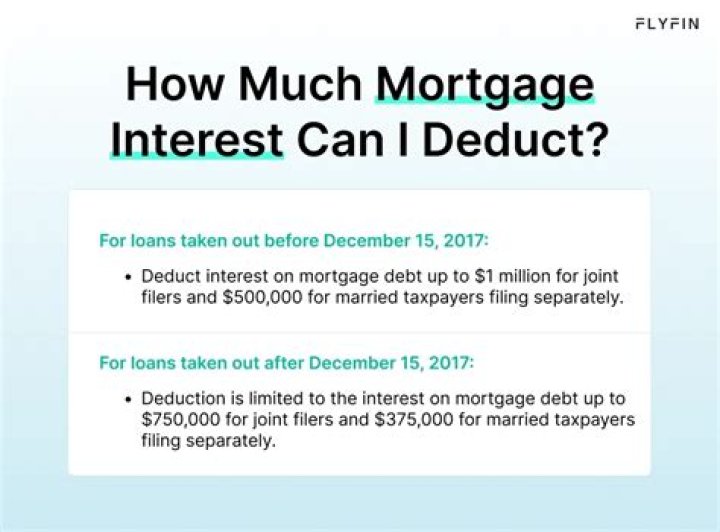

Yes, your deduction is generally limited if all mortgages used to buy, construct, or improve your first home (and second home if applicable) total more than $1 million ($500,000 if you use married filing separately status) for tax years prior to 2018. Beginning in 2018, this limit is lowered to $750,000.

Is mortgage interest deducted from gross income?

Both the property tax deduction and the mortgage interest deduction are itemized deductions that are subtracted from your adjusted gross income to figure your taxable income. If your adjusted gross income is too high, even if your mortgage interest deduction would decrease it to below the limit, you don’t qualify.

Are there any restrictions on the mortgage interest deduction?

First, the mortgage interest deduction includes that which you paid on loans to buy a home, on home equity lines of credit, and on construction loans. But the TCJA placed a significant restriction on home equity debt beginning with the 2018 tax year.

What kind of mortgage is eligible for tax deduction?

There are a few types of home loans that qualify for the mortgage interest tax deduction. These include a home loan to buy, build or improve your home. While the typical loan is a mortgage, a home equity loan, line of credit or second mortgage may also qualify.

What are the mortgage interest deductions for 2020?

For the 2020 tax year, which will be the relevant year for April 2021 tax payments, the standard deduction is: If you choose an itemized deduction, you can pick and choose from various deductions. These include mortgage interest, student loan interest, charitable contributions, medical expenses and more.

Do you get a mortgage interest deduction when you sell your home?

As with property taxes, you can deduct the interest on your mortgage for the portion of the year you owned your home.