Can a 1099-C prove that a debt was canceled?

Nathan Sanders

Nathan Sanders

Bank argues that the 1099-C does not cancel the debt or prove that it canceled the debt. Bank argues that it stopped collection activity and issued the 1099-C simply to comply with IRS regulations. Bank argues that the 1099-C form alone is not sufficient to prove that it canceled the debt.

How is a 1099 C treated by the IRS?

It feels unfair to many, but a 1099-C is treated by the IRS as ordinary income. There’s nothing you can do about receiving the 1099-Cs, since the creditors are required to report canceled debt exceeding $600. But you can educate yourself about the legitimate options for relief on the tax bill associated with cancelation of debt income (CODI).

When do I get Form 1099-C from my lender?

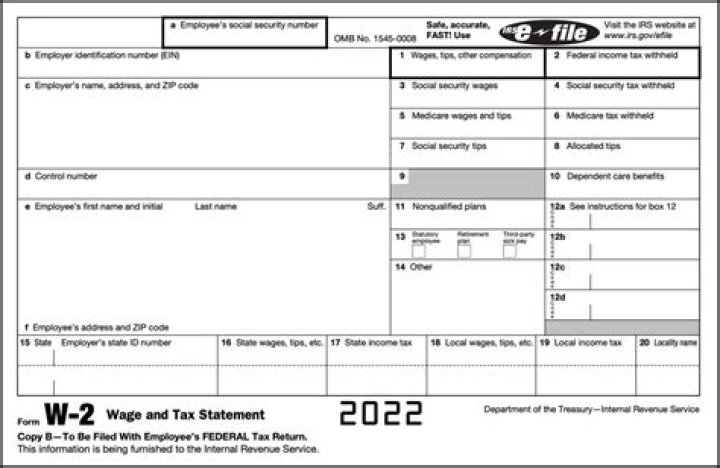

If you borrowed money from a commercial lender and at least $600 of that debt was canceled or forgiven, you should receive Form 1099-C from the lender (the IRS also receives a copy).

What happens when you get a 1099 for a foreclosure?

Debt reduced through mortgage restructuring, as well as mortgage debt forgiven in connection with a foreclosure (or short sale), qualify for this relief. This means that the amount forgiven that is included on your 1099-C form, will not be treated as ordinary taxable income to you on your tax return.

Why did the bank issue a 1099-C?

Bank asserts that it issued the 1099-C to comply with Internal Revenue Service regulations. The purpose of forms 1099-C are to show canceled or discharged debt as income to the borrower. When Debtors filed a subsequent tax return, they included the $59,667.34 of canceled debt from Bank as income and paid taxes on it.

Is the forgiven debt on a 1099-C considered ordinary income?

This means that the amount forgiven that is included on your 1099-C form, will not be treated as ordinary taxable income to you on your tax return. This provision applies to debt forgiven in calendar years 2007 through 2017.

When do creditors have to file a 1099-C?

Until 2016, IRS rules allowed creditors to file a 1099-C if no payments had been made on a debt for 36 months. This resulted in many 1099-C forms being issued for debts that were delinquent but not actually forgiven.

What do you have to report on Form 1099-C?

The only forgiven debt that must be reported on Form 1099-C is the debt principal then owed. This is consistent with the IRS explanation to borrowers quoted above where the IRS says “ [w]hen you borrow money, you don’t include the loan proceeds in gross income because you have an obligation to repay . . ..”

What is the purpose of a 1099-C tax return?

The purpose of forms 1099-C are to show canceled or discharged debt as income to the borrower. When Debtors filed a subsequent tax return, they included the $59,667.34 of canceled debt from Bank as income and paid taxes on it.

Can a 1099-C cancel an in rem obligation?

Bank argues that, even if the 1099-C does cancel the debt as to Debtors, it does not cancel the in rem obligation of the property. The parties agree on the underlying facts. In 2009, Debtors entered into a $62,000 mortgage loan with Bank secured by their home. That mortgage was behind a senior mortgage.