Can a loan company freeze your bank account?

Joseph Russell

Joseph Russell

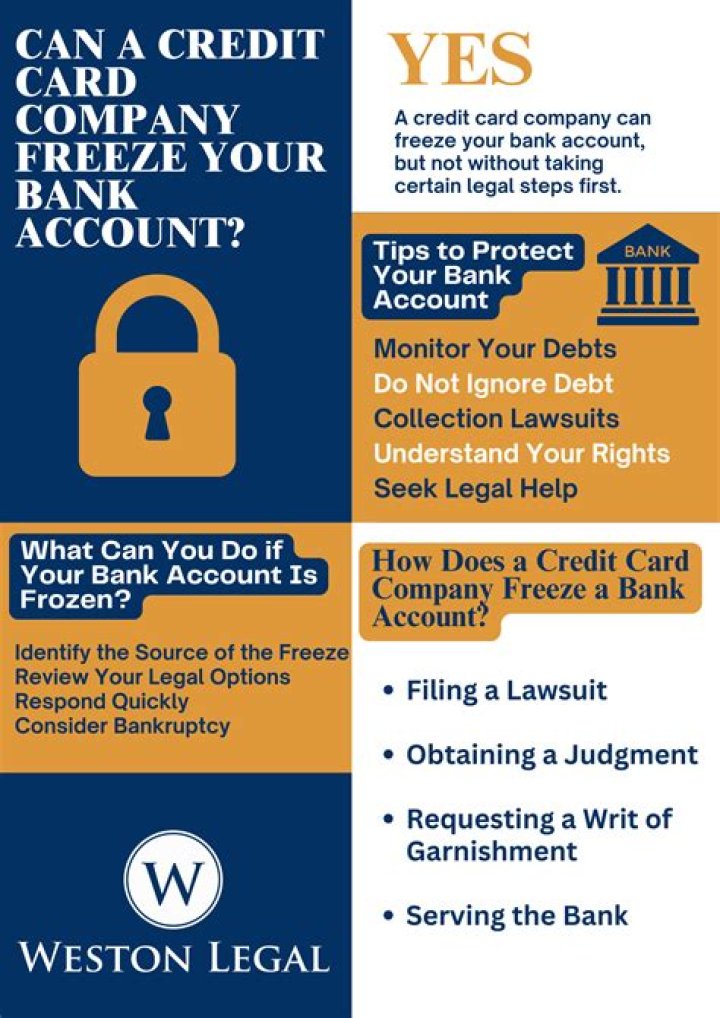

A creditor or debt collector cannot freeze your bank account unless it has a judgment. Judgment creditors freeze people’s bank accounts as a way of pressuring people to make payments.

Who can legally freeze your bank account?

Banks may freeze bank accounts if they suspect illegal activity such as money laundering, terrorist financing, or writing bad checks. Creditors can seek judgment against you which can lead a bank to freeze your account. The government can request an account freeze for any unpaid taxes or student loans.

Can I sue my bank for freezing my account?

Why Bank Accounts Get Frozen Creditors can sue you and, if successful, obtain a legal judgment from a state court awarding them powers to collect what they are owed. Creditors can place a hold on the account for as much as double the actual judgment.

Can your bank account be frozen without notice?

Can the bank freeze my account without notice? Yes, if your bank or credit union receives an order from the court to freeze your bank account, it must do so immediately, without notifying you first.

Can a bank deny you access to your money?

Banks are able to place “holds” on deposits, preventing you from using all or part of the total amount you put in. The bank makes it so that you cannot withdraw the money or use it for payments, even though those funds appear in your account.

Can banks take your money in a recession?

The Federal Deposit Insurance Corp. (FDIC), an independent federal agency, protects you against financial loss if an FDIC-insured bank or savings association fails. Typically, the protection goes up to $250,000 per depositor and per account at a federally insured bank or savings association.

Can my bank account be frozen without notice?

Why would a bank freeze my account?

To protect your account On occasion, a bank will freeze your account if it thinks that someone is trying to gain unauthorised access to it or trying to make some kind of fraudulent payment.

How do you keep money safe in a recession?

7 Ways to Recession-Proof Your Life

- Have an Emergency Fund.

- Live Within Your Means.

- Have Additional Income.

- Invest for the Long-Term.

- Be Real About Risk Tolerance.

- Diversify Your Investments.

- Keep Your Credit Score High.

Can you sue a bank for not refunding your money?

Unfortunately, banks are a business and are sometimes more interested in holding onto their own profits than doing what’s right for their customers. So, if you’ve been a victim of fraud and the bank does not cooperate, can you sue them? In most cases, the answer is, sadly, no.

Can a company seize your bank account?

Answer. Bad news: It’s legal for a creditor with a court judgment against you to freeze or “attach” your bank account. Some creditors, like the IRS, can attach your account even without a court judgment.

Can a debt collector freeze your bank account in Texas?

However, Texas does allow for a bank account to be frozen. Once your wages are deposited into your bank account, the funds can be frozen and possibly seized. In order to do this, a debt collector must have won the lawsuit and had an order issued by the court.

Can a bank freeze your account for unpaid debt?

If you have any unpaid debts, your creditors can get the bank to freeze your account in order to satisfy your obligations. But they must first get approval from the courts before taking this action. 1 They do this by getting a judgment against you. This is then sent to the bank and is kept on file.

Can a bank freeze an account with a levy?

A bank can still receive a levy and freeze an account with funds from any of these sources. Bank accounts that receive deposits from multiple sources will have to wait until the bank can separate the income that can and cannot be garnished. How Long Can Creditors Collect on a Business Debt?

Can a creditor file a car repossession in Texas?

A creditor can file a lawsuit seeking an order to begin the car repossession process. However, automobile repossession laws in Texas allow creditors with valid liens on vehicles to use “self-help” methods when a borrower is behind on loan payments.