Can all NOL be carried back 5 years?

Aria Murphy

Aria Murphy

A1. Yes. Generally, you are required to carry back any NOL arising in a taxable year beginning in 2018, 2019, or 2020, to each of the five taxable years preceding the taxable year in which the loss arises.

How many years can you carryback an NOL?

5 years

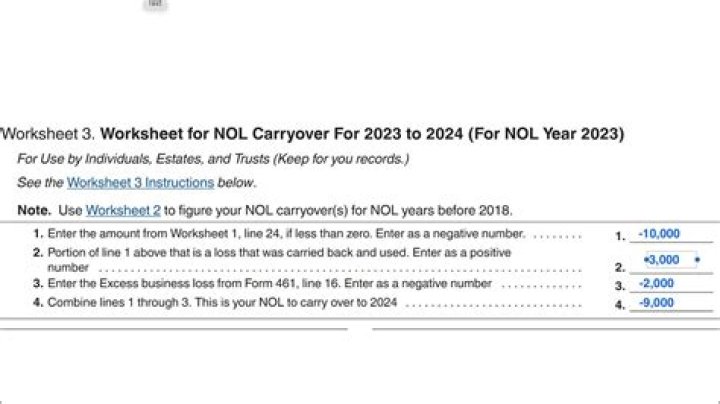

New rules for NOL carrybacks. Section 2303 of the CARES Act amended section 172 as revised by the Tax Cuts and Jobs Act (TCJA), section 13302, for tax years 2018, 2019, and 2020. Taxpayers can carry back NOLs, including non-farm NOLs, arising from tax years beginning in 2018, 2019, and 2020 for 5 years.

How far back can you carry losses?

Companies that cease to trade additionally have access to Terminal Loss relief (section 39 CTA10) which allows unlimited carry back of trading losses of the final accounting period to set off against profits of the previous 3 years (provided that the company was carrying on the trade in the accounting period or period( …

Are there Nol carrybacks for 2018 and 2019?

In addition, taxpayers carrying back NOLs to 2018 and 2019 should consider the potential interaction of NOL carrybacks with the base erosion and anti-abuse tax (BEAT).

Can You forego carrybacks for 2018 to 2020?

Specifically, a separate election to forego carrybacks may be made for each of 2018, 2019 and 2020 without binding the taxpayer as to any other year. For example, assume a calendar year corporate taxpayer has an NOL in 2019 and expects another NOL in 2020, but had taxable income in years 2014 through 2018.

When does the Care Act allow for carryback?

The Act amends section 172 (b) to allow for the carryback of losses arising in a taxable year beginning after Dec. 31, 2017, and before Jan. 1, 2021, to each of the five taxable years preceding the taxable year of the loss.

Can a carry back to a 965 year be carried back?

However, please be aware that under the CARES Act, section 172 (b) (1) (D) (iv) has been added to provide that a taxpayer who has a carryback to a section 965 year is deemed to have made a section 965 (n) election that limits the amount of the loss that can be carried back to each such 965 year.