Can an S Corp have a simple plan?

John Peck

John Peck

That’s pretty good. As with a SEP-IRA, an employee controls the Simple-IRA account. This subtlety means that as compared to something like a SEP-IRA or, possibly, a 401(k) plan, an S corporation using a Simple-IRA will need to pay shareholder-employees more money subject to payroll taxes.

How do S corporations maximize benefits?

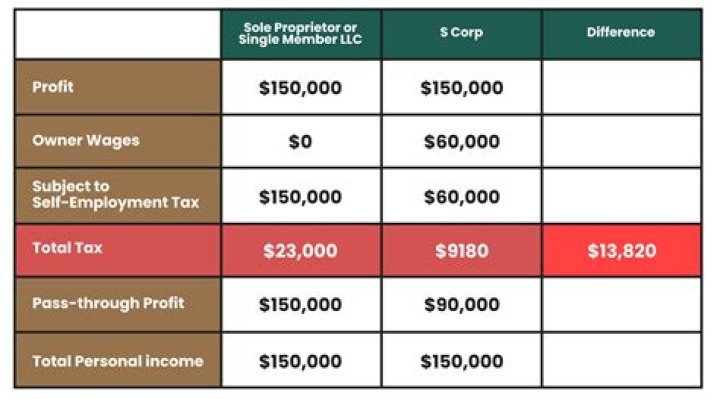

Slash S-Corp Taxes for Good

- #1 Reduce Owner’s Wages.

- #2 Cover Owner’s Health Insurance Premiums.

- #3 Employ Your Child.

- #4 Sell Your Home to Your S-Corp.

- #5 Home-Office Expenses.

- #6 Rent Your Home to Your S-corp.

- #7 Use of an Accountable Plan to Reimburse Travel Expenses.

How do you terminate a simple plan?

To terminate a SIMPLE IRA plan, notify the financial institution that you will not make a contribution for the next calendar year and that you want to terminate the contract or agreement. You must also notify your employees that the SIMPLE IRA plan will be discontinued.

What do you need to know about closing a s Corp?

How To Close an S Corp: Everything You Need to Know. Check your state’s business codes to make sure you comply with the necessary procedures to legally end the business.3 min read. Knowing how to close an S Corp correctly will ensure you dissolve your business legally. You’ll have to do the following: Obtain a shareholder vote to dissolve.

When does A S corporation terminate in a reorganization?

The specific accounting method, which is made via an election to close the books of the corporation at the end of the S short year (Sec. 1362(e)(3)). If the reorganization has caused a termination of S status and an exchange of 50% or more of the corporation’s stock,…

What do you need to dissolve a S corporation?

In most states, an S corporation requires shareholder authorization to dissolve. Regardless of the steps taken to dissolve the company, they must be documented and filed in writing with the Secretary of State in all states where you are registered to do business.

When does the s short year end in a reorganization?

If an S corporation terminates its S status as the result of a merger or other tax-free reorganization, the S corporation year (the S short year) ends on the day before the terminating event. If the corporation remains in existence as a C corporation, it must determine which method will apply for allocating income to the S short year: