Can corporations carry back net operating loss?

David Craig

David Craig

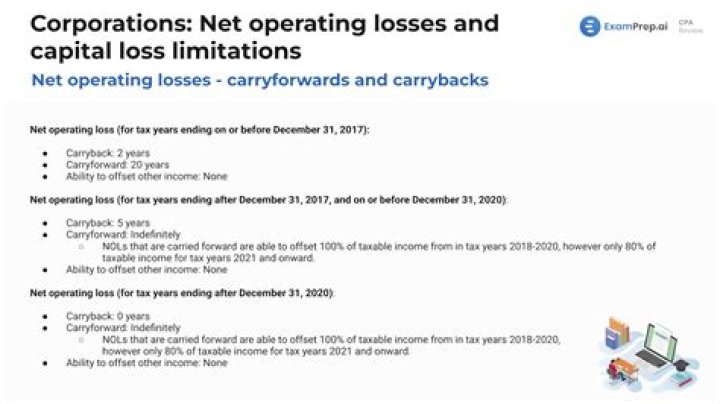

To the extent the NOL is a farming loss, the carryback period is 2 years. Any such loss not applied in the 2 preceding years can be carried forward indefinitely (subject to limitations). See the instructions for line 14. The corporation can make an irrevocable election to forgo the 2-year carryback period.

Can a company sell NOLs?

The IRS (in Section 382 of the tax code) generally limits NOL carryforward for corporations that have ownership changes greater than 50%. They do this because they don’t want the owners of corporations to sell NOLs. We call this a Section 382 NOL limitation—or, simply, a 382 limitation.

Can corporations carry forward losses?

At the federal level, businesses can carry forward their net operating losses indefinitely, but the deductions are limited to 80 percent of taxable income. Prior to the Tax Cuts and Jobs Act (TCJA) of 2017, businesses could carry losses forward for 20 years (without a deductibility limit).

Can a corporation carry forward losses?

What is the value of NOLs?

Net operating loss (NOL) carryforwards are a valuable asset because they can lower a company’s taxable income. Under IRS Section 382, the amount of taxable income, which a corporation may offset with NOLs arising before the ownership change, may be subject to a limitation.

What is an example of a NOL for a business?

An NOL is the excess of a business’s tax deductions for the tax year over its taxable income for that year. Example. For tax year 1, A has $100,000 of gross income and $125,000 of tax deductions.

How are NOLS used in mergers and acquisitions?

Mergers and Acquisitions Tax Services Past losses, future gains Tax attributes such as net operating losses and built-in losses (assets with a tax basis higher than value) can provide a tax shield against future taxable income. These tax attributes will be referred to as NOLs in this discussion.

When to use net unrealized built in gain ( Nol )?

But the analysis does not stop there. Having a full understanding of a company’s status as a Net Unrealized Built-in Gain (NUBIG) or Net Unrealized Built-in Loss (NUBIL) corporation is critical. The annual utilization of NOLs can be increased significantly if the acquired company is a NUBIG corporation.

Is the net operating loss included in the NOL?

Certain types of losses and deductions are generally excluded from the NOL calculation, including: Most net operating losses are related to business losses. To take the loss, you must include it on your personal tax return.