Can excess business losses be carried back?

Sophia Bowman

Sophia Bowman

For businesses, net operating losses from the 2018, 2019, and 2020 tax years can now be carried back. The excess business loss rules have been suspended temporarily for individuals. The adjusted taxable income limit of 30% for the limitation is raised to 50% for 2019 and 2020.

What is the excess business loss limitation 2021?

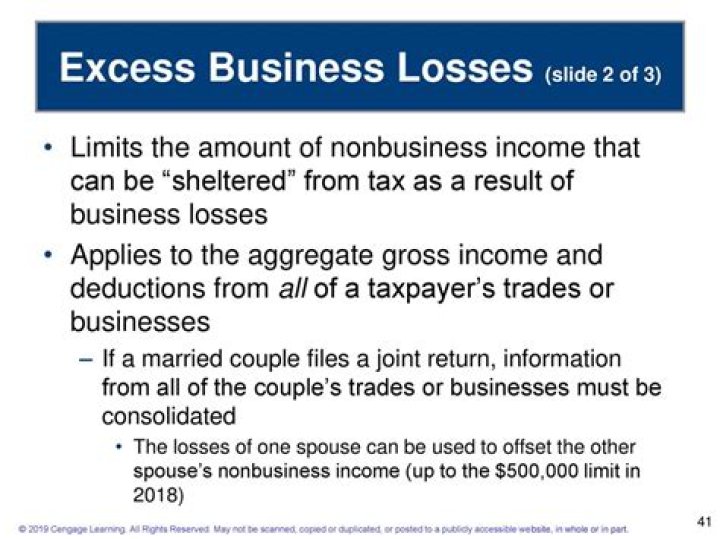

An excess business loss is one that exceeds $250,000 ($500,000 for a married joint-filing couple). These limits are adjusted annually for inflation. Barring a further tax-law change, the excess business loss disallowance rule will come back into play for losses that arise in tax years beginning in 2021 through 2025.

What is excess business loss limitation?

An excess business loss is the amount by which the total deductions attributable to all of your trades or businesses exceed your total gross income and gains attributable to those trades or businesses plus a threshold amount adjusted for cost of living.

What is a loss limitation?

Loss Limitation — an optional feature of a retrospective rating plan that limits or “caps” the amount of loss (usually at the $100,000 level, or more) that would otherwise be applied to the calculation of premium. An additional premium is charged for this feature by means of an “excess loss premium” (ELP) factor.

How many years can you show a loss on your business?

The IRS will only allow you to claim losses on your business for three out of five tax years. If you don’t show that your business is starting to make a profit, then the IRS can prohibit you from claiming your business losses on your taxes.

When to deduct business losses under the CARES Act?

Section 2304 (a) of the CARES Act retroactively suspends this rule. Now noncorporate taxpayers can deduct excess business losses arising in 2018, 2019, and 2020. However, for any tax years beginning after Dec. 31, 2020, and before Jan. 1, 2026, excess business losses will not be allowed (Sec. 461 (l) (1) (B)).

What does the CARES Act mean for net operating losses?

The CARES Act temporarily suspends retroactively changes made to the treatment of net operating losses by the 2017 Tax Cuts and Jobs Act (the “2017 Tax Act”). It also suspends retroactively the limitation on excess business losses added to the Internal Revenue Code (the “Code”) by the 2017 Tax Act.

Is there a limitation on excess business losses?

The Coronavirus Aid, Relief, and Economic Security Act (CARES Act), amended section 461 (l) to restrict the limitation on excess business losses of noncorporate taxpayers to tax years beginning after 2020 and before 2026. The Act repealed the limitation for tax years 2018, 2019, and 2020.

When is the CARES Act going to take effect?

The CARES Act retroactively removes that impact by providing those taxpayers with refunds for 2018 and 2019, and removes excess business loss limits in 2020. The Act specifically accomplishes this by: