Can I be on a car title but not the loan?

Isabella Wilson

Isabella Wilson

Can I add another person to my car title if they aren’t on the loan? An auto title indicates who legally owns a vehicle. Some lenders will allow loan holders to add another person to the title that isn’t a part of the original loan and some will not. Check with your lender for details.

What happens when you use your car as collateral for a loan?

Loans using cars as collateral tend to have a lower interest rate. If a car has been put up as collateral and the loan is not paid, the bank will repossess the car and sell it to pay off the loan. Because the loan is guaranteed by the collateral, the interest rate is often less than an unsecured loan.

What does it mean when your auto loan is closed?

“Paid,” or “paid in full,” is the term applied to installment accounts, like car loans, after the last payment is made and you have completed repayment of the loan as agreed. Since you can’t use the account for anything else, once a loan is paid in full, it is essentially closed.

What does title holding state mean?

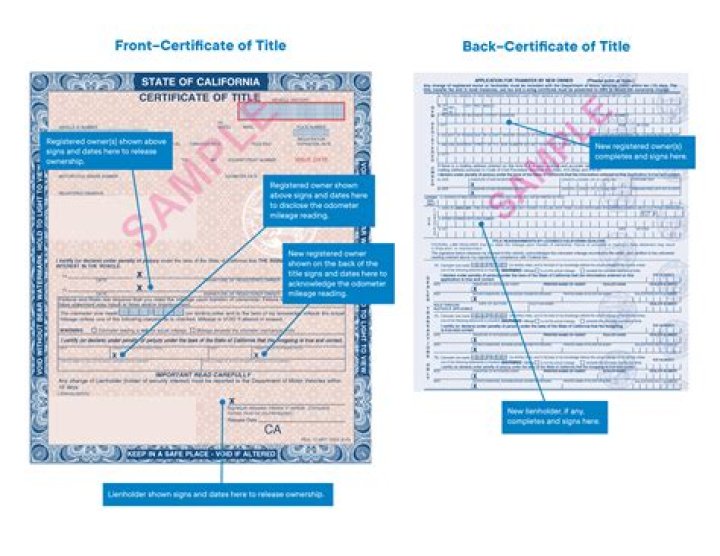

A title-holding state is one where the lienholder (your lender) keeps the title until you’ve paid off the auto loan. If you’re financing, your lender is listed on the title, too. The nine non-title holding states are: Michigan, Minnesota, New York, Arizona, Kentucky, Oklahoma, Wisconsin, Maryland, and South Dakota.

Can someone be added to car loan?

Adding a co-borrower to an existing auto loan can help you out. In order for someone to be a co-borrower, in most cases, they must have a credit score that’s as least as good as yours. Once your co-borrower signs the loan papers, they have equal ownership of the vehicle.

What does it mean to use my car as collateral?

Vehicle collateral loans, or car title loans, use the equity of your car or automobile as the collateral securing the money you borrow. For example, a lender may not agree to write the loan for less than a specified amount. If your car is not worth this lending threshold, then you may not qualify for the loan.

What states are title holding?

Though your lien holder will receive a separate document verifying their connection to the loan, you will be in possession of the title itself. There are only nine title-holding states: Kentucky, Maryland, Michigan, Minnesota, Missouri, Montana, New York, Oklahoma, Wisconsin.

How long does it take to get a title after paying off a loan?

Typically, getting a signed title out to you after you make the final payment can take up to 30 days. If you’re pressed for time, take the released title to the DMV after you obtain it so you can do the transfer immediately. If time isn’t an issue, you can mail the paperwork to the DMV.

Can I get a title loan if I have not transferred the title yet?

While you can’t get a title loan without a title, you can actually get a new title document through your local DMV. A car title loan is a fast and easy way to get money.

Can someone else put up collateral for my loan?

They can. It is called fraud and/or breach of fiduciary duty. If you pledge something you do not own the creditor cannot successfully seize the item if you default on the loan.

Can you sell a car privately if its on finance?

Yes, you can sell a car with a loan on it. But as long as the loan exists, the lender has a lien on the car, meaning the lender has first rights to the car until you fully pay off the loan. If you default on your loan after selling the car, the car could get repossessed from the person you sold it to.

Can you sell a car if you have a car loan?

The lender is listed on the front of the title as a lien holder. They hold the title so you can’t sell the car until you pay off your car loan. Vehicle titles are electronic when held by the bank and must be printed once the loan is paid off.

When do lenders hold title to your car?

Lenders often hold title when there’s a lien against a vehicle, even if the registration is in your name. Your first step should be to reach out to your lender if there’s a loan against your car. In fact, most states require this.

Can you sell a car with a lien on the title?

If you fail to do this, the lender will still hold the title, and you cannot legally transfer the title to a buyer without having the title to sign it over. The lender is listed on the front of the title as a lien holder. They hold the title so you can’t sell the car until you pay off your car loan.

Is the title of a car still tied to the bank?

I still have the vehicle and due to the account no longer being an auto loan but an account with the collections agency, I feel the title wouldn’t be tied to the bank anymore.