Can I have Roth IRA and Roth 401k?

Isabella Wilson

Isabella Wilson

Yes, it is possible to have both a Roth IRA and a Roth 401(k) at the same time. If you don’t have enough money to max out contributions to both accounts, experts recommend maxing out the Roth 401(k) first to receive the benefit of a full employer match.

Is a Roth IRA an individual retirement account?

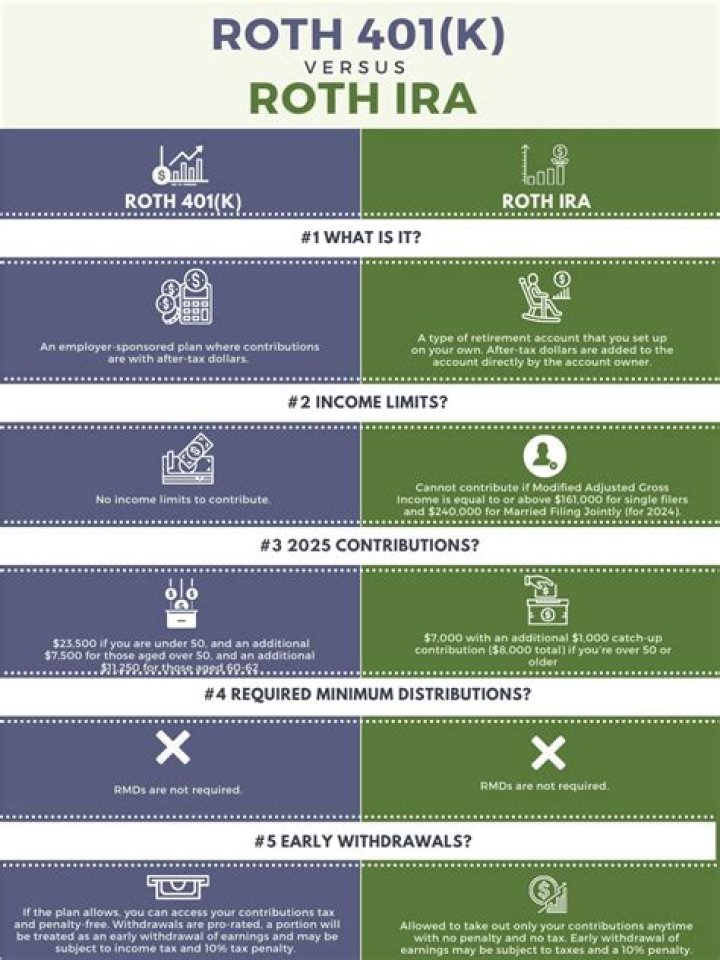

A Roth IRA is an individual retirement account that provides tax-free growth and withdrawals. You can open a Roth IRA at a brokerage or bank. The 2021 contribution limit is up to $6,000 ($7,000 if 50 or older) for modified adjusted gross incomes below $140,000 (single filers) or $208,000 (married filing jointly).

How do I choose between 401k and Roth IRA?

The main difference between a Roth IRA and 401(k) is how the two accounts are taxed. With a 401(k), you invest pretax dollars, lowering your taxable income for that year. But with a Roth IRA, you invest after-tax dollars, which means your investments will grow tax-free.

What’s the difference between a 401k and a Roth IRA?

Both 401 (k)s and Roth IRAs are popular tax-advantaged retirement savings accounts that differ in tax treatment, investment options, and employer contributions. Both accounts allow your savings to grow tax-free.

Can a deductible 401k be put into a Roth IRA?

Whether your traditional IRA contributions are deductible, however, will depend on your income. 2 Your income will also affect how much money, if any, you can put into a Roth IRA. 4

What’s the income limit for a Roth 401k?

In 2020, as per the IRS, contributions go up to $19,500 and an additional $6,500 catch-up contribution for those age 50 and older. Unlike Roth IRAs, Roth 401 (k)s do not have an income limit, allowing high-wage earners to contribute to one. Another advantage to Roth 401 (k)s is those matching contributions.

Can a 401k contribution be made to a traditional IRA?

Contributions to a traditional IRA are often tax-deductible. But if you are covered by a 401(k) or any other employer-sponsored plan, your modified adjusted gross income (MAGI) becomes a factor how much of your contribution to a traditional IRA account you can deduct—or whether none of it is deductible.