Can retirement accounts be seized?

Emily Baldwin

Emily Baldwin

The general answer is no, a creditor cannot seize or garnish your 401(k) assets. 401(k) plans are governed by a federal law known as ERISA (Employee Retirement Income Security Act of 1974). One exception is federal tax liens; the IRS can attach your 401(k) assets if you fail to pay taxes owed.

Are IRAs protected from creditors in New York?

In New York, for the most part your retirement accounts (like 401(k)s and IRAs) are safe from judgment creditors. If you live in New York and a creditor gets a judgment against you, that judgment creditor will probably not be able to collect from your retirement account.

Can I lose my retirement in a lawsuit?

Whether your individual retirement account (IRA) can be taken in a lawsuit depends largely on your state of residence and the judgment in question. There are no federal protections in place shielding your IRA from seizure in a lawsuit.

Are IRAs safe from creditors?

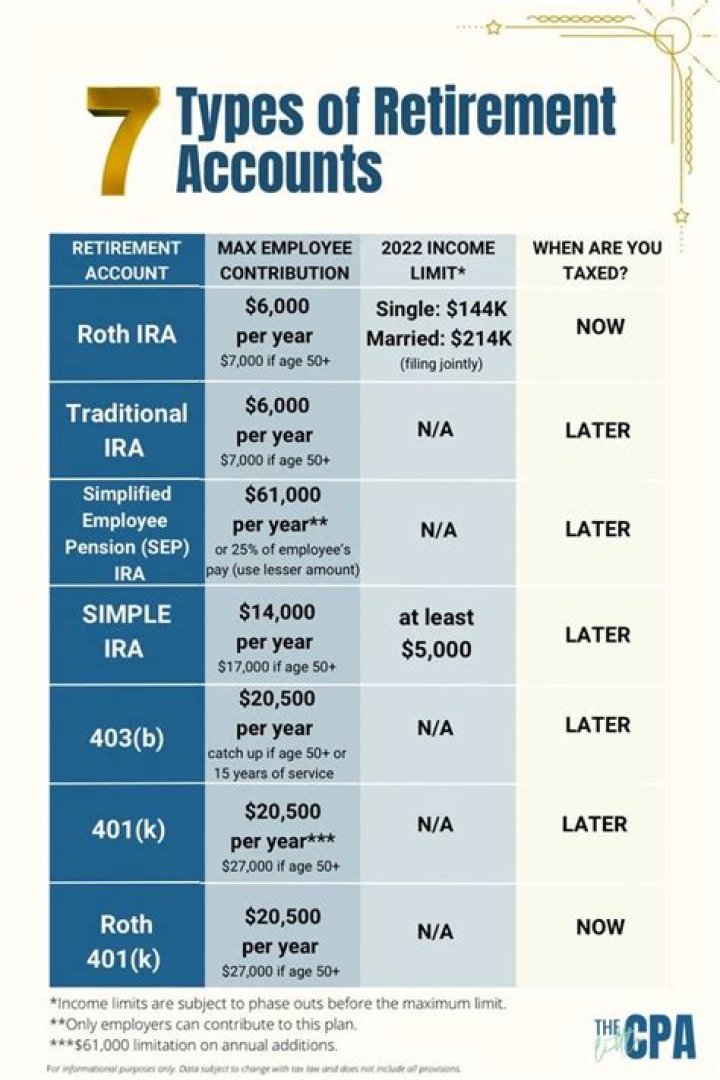

Assets in an IRA and/or Roth IRA are protected from creditors up to $1,283,025. All assets held in ERISA plans are protected from creditors even after they are rolled over to an IRA. Retirement assets are not protected from an IRS levy.

When do you have to take money out of an IRA in New York?

Withdrawals from a traditional IRA must start by the time the account holder reaches the age of 70 1/2. New York State determines your adjusted gross income for taxes by using your federal AGI. However, New York does offer an exclusion for up to $20,000 of income for pensions and annuities, including IRAs, under certain circumstances

Can a person contribute to an IRA at any age?

You can do this at any age. When you transfer money from one IRA to another IRA it is called an IRA transfer and you can also do this at any age. In contrast, a contribution is new money that was not previously in a tax-deferred account and that you are now putting into an IRA. Do not confuse Roth conversions with contributions, either.

How is a traditional IRA related to employment in New York?

The traditional IRA is not related to employment in New York. The taxpayer must accrue the conversion income to the nonresident period. Accordingly, the taxpayer would include in New York adjusted gross income the $40,000 conversion income, and no amount of the conversion income would be included in New York source income.

How much can you contribute to an IRA in New York?

However, New York does offer an exclusion for up to $20,000 of income for pensions and annuities, including IRAs, under certain circumstances. Roth IRA contributions are made with post-tax dollars, so you can’t claim a federal tax deduction.