Can S Corp take Qbi deduction?

John Peck

John Peck

S corporations and partnerships generally aren’t taxpayers and, therefore, can’t take the deduction themselves. The QBI deduction isn’t allowed in calculating the non-corporate owner’s adjusted gross income (AGI), but it reduces taxable income. In effect, it is treated the same as an allowable itemized deduction.

Does S Corp qualify for Qbi?

QBI is the net amount of qualified items of income, gain, deduction and loss from any qualified trade or business, including income from partnerships, S corporations, sole proprietorships, and certain trusts.

Does 1120S qualify for Qbi?

The QBID allows owners of pass-through businesses to deduct up to 20 percent of the qualified business income from their taxable income. It is this information from Box 17 of the Schedule K-1 (Form 1120S) that should be used by the Shareholder to calculate any 199A Deduction on their individual return.

Does all Schedule C qualify for Qbi deduction?

A sole proprietorship (or single member LLC) reports the information needed for the taxpayer to calculate any Qualified Business Income on Schedule C and the Net Profit or (loss) that is reported on Line 31 of Schedule C will be the starting point for the QBI coming from each sole proprietorship.

How to calculate qualified business income on Form 1120S?

If the taxpayer receives a Schedule K-1 (Form 1120S) with Section 199A Income in Box 17, Code V that income amount may be subject to certain deductions to determine the Qualified Business Income (QBI) from that business. Items that reduce QBI from a S Corporation are the following:

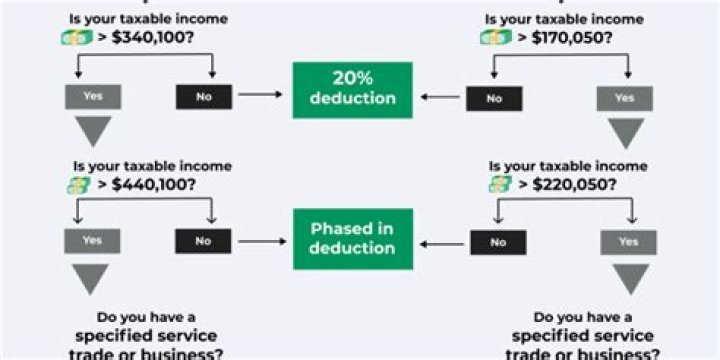

How much qualified business income can I deduct?

Code V. Section 199A information. Generally, you may be allowed a deduction of up to 20% of your net qualified business income (QBI) plus 20% of your qualified REIT dividends, also known as section 199A dividends, and qualified publicly traded partnership (PTP) income from your S corporation.

How does making QBID entries involving an S-Corporation ( Form 1120S ) work?

Making QBID entries involving an S-Corporation (Form 1120S) As a pass-through entity, the income (or loss) from a Subchapter S-Corporation (Form 1120S) is treated on the tax return of its owner (s) as Qualified Business Income (or Loss) under the Section 199A deduction.

Where does the S-corporation report on the Form 1120S?

The S-Corporation reports this information on the Schedule K-1 (Form 1120S) in Box 17, Codes V through Z. It is this information from Box 17 of the Schedule K-1 (Form 1120S) that should be used by the Shareholder to calculate any 199A Deduction on their individual return. The Box 17 information that is used in the QBID calculation is the following: