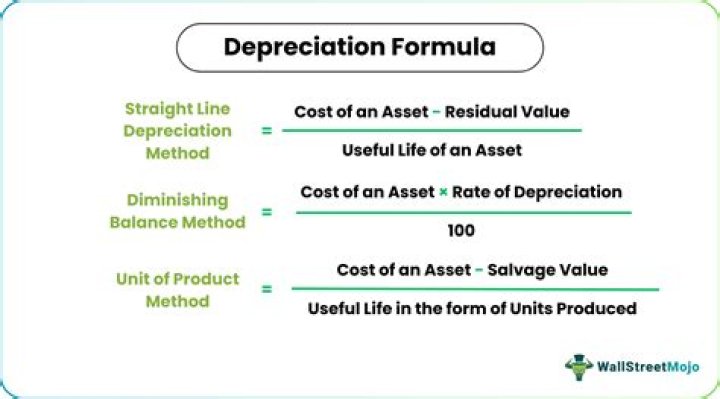

Can you change the depreciation method of an asset?

Emma Jordan

Emma Jordan

Taxpayers can request an automatic method change for depreciation and amortization if the requirements are met to do so. Taxpayers may change from an impermissible method of accounting to a permissible method of accounting or from one permissible method of accounting to another permissible method of accounting.

How do you account for a change in depreciation method?

For example, an entity changing from the reducing balance method to a straight line basis of depreciation, should account for this as a change in accounting estimate, in line with FRS 102 paragraph 10.16, by applying the change prospectively from the date of the change.

Do you need to file Form 3115 to correct depreciation?

That would actually be counter to the established procedure for rectifying the failure to take depreciation deductions over two or more tax years. If you are going to amend your 2018 return, then you also need to file Form 3115 since you used an improper method of accounting in previous years.

How to file Form 3115 for automatic change?

Automatic change requests. Except if instructed differently, you must file Form 3115 under the automatic change procedures in duplicate as follows. Attach the original Form 3115 to the filer’s timely filed (including extensions) federal income tax return for the year of change. The original Form 3115 attachment does not need to be signed.

Do you need to sign the form 3115 attachment?

The original Form 3115 attachment does not need to be signed. File a copy of the signed Form 3115 to the address provided in the address chart on this page, no earlier than the first day of the year of change and no later than the date the original is filed with the federal income tax return for the year of change.

Who is eligible for a reduced form 3115?

Reduced Form 3115 filing requirement. A qualified small taxpayer qualifies for a reduced Form 3115 filing requirement for the following DCNs: 7, 8, 21, 87, 88, 89, 107, 121, 145, 157, 184–193, 198, 199, 200, 205, 206, 207, and 222. A qualified small taxpayer is a taxpayer with average annual gross receipts