Can you deduct full mortgage interest?

John Peck

John Peck

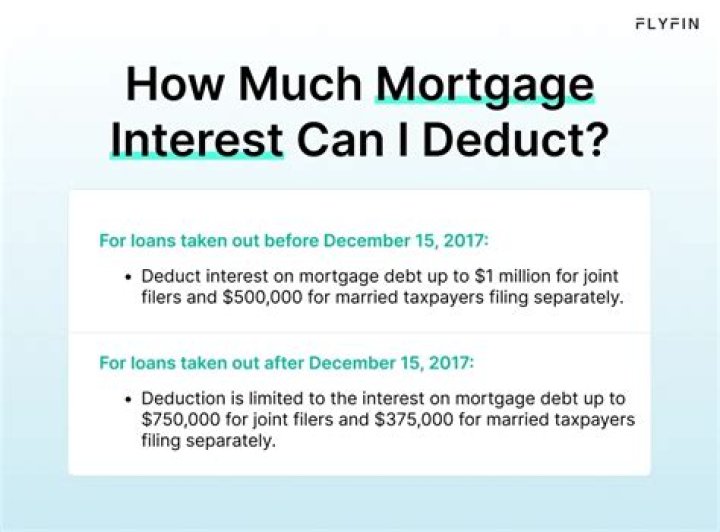

The mortgage interest deduction allows you to reduce your taxable income by the amount of money you’ve paid in mortgage interest during the year. As noted, in general you can deduct the mortgage interest you paid during the tax year on the first $1 million of your mortgage debt for your primary home or a second home.

Can you deduct mortgage interest if you don’t itemize?

You Don’t Itemize Your Deductions The home mortgage deduction is a personal itemized deduction that you take on IRS Schedule A of your Form 1040. If you don’t itemize, you get no deduction. This means far few taxpayers will benefit from the mortgage interest deduction.

When do I have to deduct interest on my mortgage?

You can only deduct interest on the first $375,000 of your mortgage if you bought your home after December 15, 2017. Home mortgage interest.

Where to claim mortgage interest on a schedule a?

Eligible taxpayers may deduct the interest they paid on a mortgage on line 8 of the Schedule A. This deduction applies to any mortgaged property that you use personally.

Can you deduct mortgage interest on both schedule a and E?

The law allows you to deduct this interest on a Schedule A when it’s a personal expense and on a Schedule E when the expense relates to a rental property. If you use one property as both a personal residence and a rental property, you can take a mortgage interest deduction on both a Schedule A and a Schedule E. You can’t double dip, though.

What are the categories for mortgage interest deductions?

The Internal Revenue Service (IRS) uses three categories to determine how much mortgage interest you can deduct: Category 1. Any mortgage taken out on or before October 13, 1987, which is called grandfathered debt. All interest paid on this category of mortgage is fully deductible regardless of your mortgage amount. Category 2