Can you take standard deduction from capital gains?

Aria Murphy

Aria Murphy

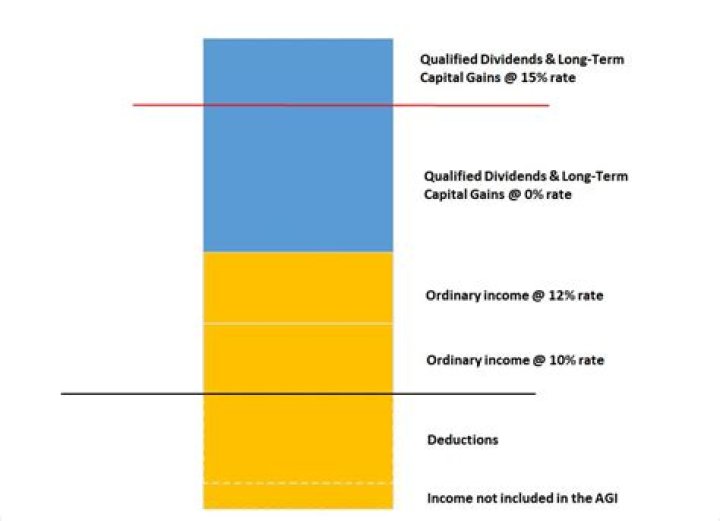

His adjusted gross income (including long-term capital gains and dividends) is $69,700. After claiming the standard deduction of $18,000, his taxable income is $51,700, which is the top of the 0% bracket for heads of households….

| Ordinary Income Tax Rate | Long-Term Capital Gains and Qualified Dividends Tax Rate |

|---|---|

| 39.6% | 20% |

What is the Colorado capital gain subtraction?

You may subtract certain net capital gain income to the extent the gains are included in your federal taxable income. This subtraction is available if you meet specific qualifications. See Colorado Income Tax FYI Publication Income 15 and Form 1316 for additional details.

Are state capital gains taxes deductible?

Taxpayers who itemize deductions on their federal income tax returns can deduct state and local real estate and personal property taxes, as well as either income taxes or general sales taxes. Initially, all state and local taxes not directly tied to a benefit were deductible against federal taxable income.

Does Colorado have a tax deduction for 529 contributions?

Tax Advantages If you are a Colorado taxpayer, every dollar you contribute to a CollegeInvest 529 can be deducted from your Colorado state income tax return. When you file your taxes, you also have the option to direct deposit your refund to your CollegeInvest account. More information can be found here.

What is Colorado state tax on capital gains?

4.55 percent

State Taxes on Capital Gains Colorado taxes its capital gains at the same rate as ordinary income: 4.55 percent. Colorado could raise its income tax rate on capital gains, in line with the federal income tax code, which taxes long-term capital gains at 0-20 percent depending on your income bracket.

Does Colorado have capital gains tax?

Capital Gains Tax Rates In Colorado, you’ll pay capital gains taxes at the same rate you pay on your general income. This is 4.63 percent, putting it on the lower end of the states that do tax residents on capital gains. California is the highest, at 12.3 percent, while North Dakota is the lowest, at 2.9 percent.

Can a grandparent contribute to a 529 plan and claim a tax deduction in Colorado?

Yes, grandparents can claim the deduction for contributing to a 529 if they live in one of the 34 states that offer a state income tax deduction for 529 college-savings plan contributions. The only question is whether you must own the account or whether you can contribute to one set up by, say, the child’s parents.

Do you get a capital gains tax deduction in Colorado?

The good news is, Colorado lets you deduct capital gains tax you paid on a federal level, so you may find that you don’t owe as much as you thought you did. The State of Colorado refers to these as “subtractions” and they can save you money, as long as you qualify.

How to report capital gain income in Colorado?

You’ll report the income on Form DR 1316, which is the Colorado Source Capital Gain Affidavit. This form will help you calculate how much you owe based on the asset you sold during the tax year.

Can you deduct capital gains from state taxes?

AL, AR, DE, HI, IN, IA, KY, MD, MO, MT, NJ, NM, NY, ND, OR, OH, PA, SC, and WI either allow taxpayer to deduct their federal taxes from state taxable income, have local income taxes, or have special tax treatment of capital gains income. This material is for general information and educational purposes only.

How to calculate capital gains tax for 2020?

Includes short and long-term Federal and State Capital Gains Tax Rates for 2020 or 2021. Calculate the capital gains tax on a sale of real estate property, equipment, stock, mutual fund, or bonds. Requires only 7 inputs into a simple Excel spreadsheet.