Can you withdraw a Tax Court petition?

Robert Harper

Robert Harper

7 (Mar. 4, 2021), the Tax Court held that a Tax Court petition to review the denial of interest abatement can be withdrawn by the taxpayer without the Tax Court entering a decision in the IRS’s favor.

How do I petition Tax Court?

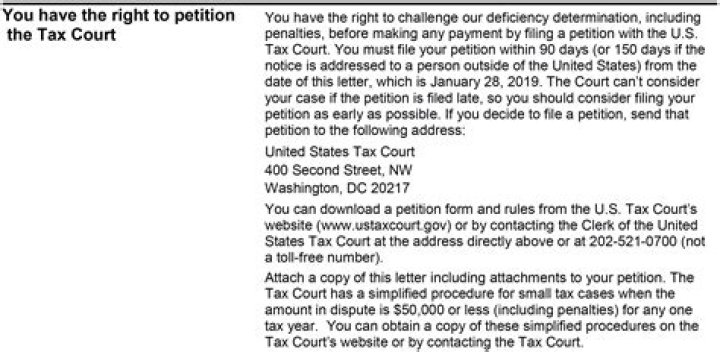

If you want to file a petition with the U.S. Tax Court You can download a petition form PDF and rules from the U.S. Tax Court. You have 90 calendar days from the date of your CP3219N to file a petition with the Tax Court. The last day to file a petition is stated in your CP3219N.

Can a CPA represent in Tax Court?

CPAs or Enrolled Agents who are seeking to have greater interaction with the Internal Revenue Service (IRS) or the right to practice in U.S. Tax Court can pursue a tax specialty designation referred to as “Admitted to Practice, U.S. Tax Court” by successfully passing the Tax Court Exam.

Which is one of the three actions the Supreme Court may take when it reviews a case?

he three actions the US Supreme Court may take when it reviews a case: The Supreme Court of the United States of America can choose to not hear a case. The Supreme Court can also send the case back to a lower court. Or, the US Supreme Court Judges can choose to proceed to hear the case and issue a ruling.

Who can file a petition with the Tax Court?

You must file a petition to begin a case in the Tax Court. A party who files a petition in response to an IRS notice of deficiency, notice of determination, or notice of certification is called the petitioner. The Commissioner of Internal Revenue is referred to as the respondent in Tax Court cases. Who can file a petition with the Tax Court?

Who is the respondent in a tax court case?

A party who files a petition in response to an IRS notice of deficiency, notice of determination, or notice of certification is called the petitioner. The Commissioner of Internal Revenue is referred to as the respondent in Tax Court cases.

When do you need to file answers in Tax Court?

Tax Court Rule 173 (b) as amended now requires answers to be filed in all “S” cases. The amendment is effective for all petitions filed after March 13, 2007. This change will assist petitioners and low−income taxpayer clinics in contacting the attorney assigned to the case and result in the earlier consideration of small tax cases.

When to file a petition for tax settlement?

It is difficult to know the circumstances in which you believe your case was settled. Because the IRS issued a notice, the IRS may be proceeding as if there is no settlement. To protect yourself against an unagreed assessment of tax or collection action, you should file a petition within the period set forth in the notice.