Do you get Form 1099 when your house is foreclosed?

Emma Jordan

Emma Jordan

Homeowners will typically receive an IRS Form 1099-A from their lender after their home has been foreclosed upon. The information on the form is necessary to report the foreclosure on your tax return—and yes, unfortunately, you must do so.

When to use 1099-a acquisition or abandonment of secured property?

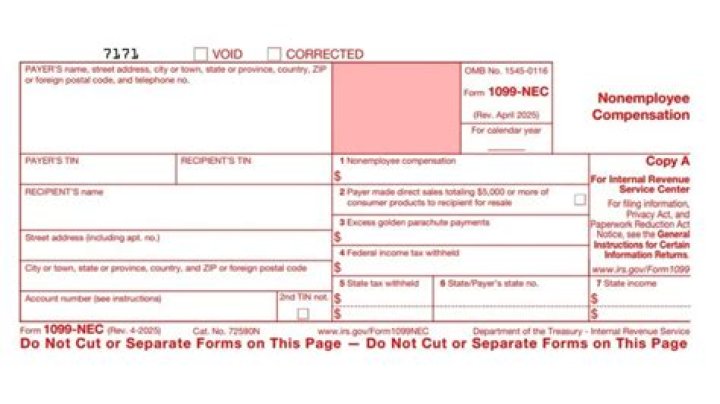

Form 1099-A: Acquisition or Abandonment of Secured Property is one of a series of 1099 forms used by the Internal Revenue Service (IRS) to report various non-wage payments and transactions. Form 1099-A is typically used when a property has been transferred due to foreclosure . Whenever a property is sold or transferred, the IRS must be informed.

What do lenders report on form 1099-a?

On Form 1099-A, the lender reports the amount of the debt owed (principal only) and the fair market value (FMV) of the secured property as of the date of the acquisition or abandonment of the property.

What to do if you lose your home to foreclosure?

Check with your lending institution to see if you qualify. Form 1099-A reports the “Acquisition or Abandonment of Secured Property” to the IRS when you lose a property to foreclosure. The lender must send a copy to both the IRS and to each borrower on the loan.

What kind of tax form do I get after foreclosure?

You’ll receive one of two tax forms after foreclosure, or perhaps both: Form 1099-A is issued by the bank after real estate has been foreclosed upon. This form reports the date of the foreclosure, the fair market value of the property, and the outstanding loan balance immediately prior to the foreclosure.

Where do I find the sale price on a Form 1099?

The Information on Form 1099-A. You’ll need the selling date and the selling price of the foreclosed property to properly report its “sale” to the IRS, and you’ll find this information on Form 1099-A. For the sales price, you’ll use either the fair market value of the property or the outstanding loan balance at the time of the foreclosure.

How much can you exclude from income from foreclosure?

The amount on line 6 is your gain from the foreclosure of your home. If you have owned and used the home as your principal residence for periods totaling at least two years during the five year period ending on the date of the foreclosure, you may exclude up to $250,000 (up to $500,000 for married couples filing a joint return) from income.

What do you need to know about form 1099-a?

Key Takeaways 1 All real estate sales and transfers must be reported to the IRS. 2 Form 1099-A is typically used to report the transfer of foreclosed property. 3 The IRS treats capital gains from foreclosure the same as gains from a traditional sale.

Do you have to report a foreclosure on your tax return?

The information on the form is necessary to report the foreclosure on your tax return—and yes, unfortunately, you must do so. You might receive multiple Forms 1099-A for a single property if you had more than one mortgage or lien against it and more than one lender was involved in the foreclosure.

How does the IRS take income from a foreclosure?

In this case, the IRS takes the position that you received income from the foreclosure because you received money from the lender to purchase your home and you did not pay all that money back. It became money in your possession that you kept.

How much can you exclude on a 1099-a?

You can exclude up to $250,000 of gains ($500,000 for married couples filing jointly) from the sale or exchange of property owned and used as a principal residence. You will use the information on Form 1099-A to report the foreclosure on your tax return.

What’s the difference between Form 1099 a and 1099 C?

Form 1099-A vs. Form 1099-C . You might receive Form 1099-C instead of or in addition to Form 1099-A if your lender both foreclosed on the property and canceled any remaining mortgage balance that you owed. Forgiven debt reported on Schedule 1099-C is unfortunately taxable income.

What should be included on a 1099-a statement?

You can also contact the lender if you think the information on your form is incorrect. The 1099-A statement should include the identity and contact information for an individual with the institution who you can reach out to with questions.

When do you not need to file Form 1099-a?

If, in the same calendar year, you cancel a debt of $600 or more in connection with a foreclosure or abandonment of secured property, it is not necessary to file both Form 1099-A and Form 1099-C, Cancellation of Debt, for the same debtor. You may file Form 1099-C only.

What does a 1099 form stand for in real estate?

A 1099-A form stands for Acquisition or Abandonment. Acquisition or abandonment applies to secured property. Individuals typically receive these in association with a mortgage that is canceled by a lender in part or completely.

When do you have to file Form 1099-a?

The IRS advises lenders to file Form 1099-A in the year following the calendar year in which you acquire an interest in the property, or first know—or have reason to know—that it has been abandoned. 2

What are the specific instructions for form 1099-a?

Specific Instructions for Form 1099-A File Form 1099-A, Acquisition or Abandonment of Secured Property, for each borrower if you lend money in connection with your trade or business and, in full or partial satisfaction of the debt, you acquire an interest in property that is security for the debt, or you have reason to

When does a lender send you a form 1099-a?

If the lender acquires the secured property from you or has reason to know that you abandoned or stopped using the secured property, the lender should send you a Form 1099-A.pdf, Acquisition or Abandonment of Secured Property.

What happens if you receive more than one 1099-a form?

If you had more than one mortgage or loan for a single property, you may receive multiple 1099-A forms. To calculate the gain or loss, subtract the tax basis in the home (the purchase price less any improvements you made) from its fair market value.

What to do if you receive a form 1099-a?

If you received a Form 1099-A, the first thing you must do is determine whether there has actually been a cancellation of debt. The lender should have sent you a Form 1099-C Cancellation of Debt if any debt was canceled. If you have not received a Form 1099-C, you may want to contact your lender to determine if any debt has been canceled.

How to request a 1099 tax return transcript?

Request for Taxpayer Identification Number (TIN) and Certification Form 4506-T Request for Transcript of Tax Return Form W-4 Employee’s Withholding Certificate

When do I get a 1099 from the IRS?

1099-C. If you had more than $600 worth of debt canceled, the creditor will typically file this form with the IRS, and you will receive a copy. You may have a tax bill related to the amount forgiven.

How is the sale of a property reported on a 1099?

Depending on the type of loan, the taxpayer will utilize either the fair market value of the property or the outstanding loan balance on the property for the selling price. Both of these figures are reported on Form 1099-A.

Can a loss be reported on a 1099-a?

However, you cannot use any loss reported on Form 1099-A that represents an unforgiven deficiency to reduce your tax liability. If the mortgage lender forgives a deficiency after a foreclosure, you also will receive a 1099-C form.

Where can I Find my 1099-C tax form?

To review all of the IRS rules and regulations regarding the filing of your 1099-C, please visit the following link: June 5, 2019 10:19 PM I received a 1099-C form for a home that was foreclosed on15+ years ago.

When to use Form 1099 a or 1099 C?

If you have property that is both foreclosed on and the debt is cancelled, you’ll get both Form 1099-A and Form 1099-C. If you only get Form 1099-A, that probably means the debt has not been cancelled. Look out. Depending on the state you’re in, the lender may have as long as 4 years to come after you for that debt.

Who is required to send a 1099 to each person on a mortgage?

Per Citimortgage, they are REQUIRED by the IRS to send a 1099-C to each person on the mortgage but use only ONE for taxes. Citimortgage quoted some IRS code. The person at Citimortgage who handles 1099’s is Michelle Parker or Judy Campbell.

Is the forgiven debt on a 1099-C considered ordinary income?

This means that the amount forgiven that is included on your 1099-C form, will not be treated as ordinary taxable income to you on your tax return. This provision applies to debt forgiven in calendar years 2007 through 2017.

What does the lender indicate on form 1099-a?

The lender also indicates on form 1099-A whether you are liable for repayment of the debt. By filing Form 1099-A, the lender alerts the IRS of a potentially taxable event.

What happens if you do not receive a 1099-C form?

Apparently you did not receive a Form 1099-C Even with the Form 1099-C, there may be no tax consequences, such as in the case of personal residences under a certain amount or in the situation of bankruptcy. But certain income tax forms would still need to be filled out for IRS.

What do you do with a 1099-a form?

Lenders could send a Form 1099-A, Acquisition or Abandonment of Secured Property, or Form 1099-C, Cancellation of Debt, or both. If you received a 1099-A because you have abandoned personal property, such as a car, you don’t need to report it in your return.

What do you do with a 1099-a after bankruptcy?

At the end of the day, there is nothing you need to do with a 1099-A relative to your taxes if the 1099-A is from a foreclosure on your primary residence and you received a bankruptcy discharge. The 1099-A is simply a reporting document letting the IRS know that a disposition of real estate occurred.

Do you need to file Form 982 on a 1099-a?

So, in the normal circumstance, no action is required on a 1099-A when the property was foreclosed or otherwise abandoned. However, if you receive a 1099-C you need to file IRS form 982 to show the IRS that you don’t owe tax on the deficiency.

When to use Form 1099 C or 1099-a?

On Form 1099-C, the lender reports the amount of the canceled debt. If the lender’s acquisition of the secured property (or the debtor’s abandonment of the property) and the cancellation of the debt occur in the same calendar year, the lender may issue a Form 1099-C only.

What do you need to know about the 1099-a form?

Answer. Regarding 1099-A reporting, Form 1099-A reports the sale of your home in foreclosure. To figure the gain or loss: See 1099-A, Box 5 to figure the sales price — also called the amount realized. If the box is marked “Yes,” you have a recourse loan.

Where is the outstanding loan balance on a 1099-a?

The outstanding loan balance is found in box 2 of the 1099-A, and the property’s fair market value is found in box 4. The date of the foreclosure is indicated in box 1, and this will be used as the “sale date.”

What do you need to know about a 1099 sale?

Unlike an ordinary sale, there is no ‘selling price’ and the Form 1099-A information is relevant to determine this value. The taxpayer will need to find the ‘selling price’ so the gain or loss can be calculated.

Where does FMV go on a 1099-a form?

Both figures are reported on Form 1099-A; the outstanding loan balance is in Box 2 and the property’s FMV is in Box 4. Which box value you’ll use depends on your states lending laws.