Do you have to file a 940 if you have no payroll?

Emily Baldwin

Emily Baldwin

It’s important to note that not all employers in the U.S. are required to file Form 940… but most are. If you’ve: Paid $1,500 or more in wages to any W-2 employee (not a contractor) OR. Had one or more W-2 employees (full-time or part-time) for at least 20 weeks out of the past year.

Can you file Form 940 online?

More In File You can e-file any of the following employment tax forms: 940, 941, 943, 944 and 945. Benefits to e-filing: It saves you time. It’s secure and accurate.

How do I pay my 940 tax online?

If you file Form 940 electronically, you can e-file and use EFW to pay the balance due in a single step using tax preparation software or through a tax professional. However, don’t use EFW to make federal tax deposits. For more information on paying your taxes using EFW, go to

Is there a line on the Form 940?

Note: Form 940 does not have a line on it relative to the “state credit” because it is not a tax credit, per se, but Part 1 of this form does show state-specific information relative to the state or states to which an employer remits state unemployment tax. We’ll go over filing instructions for IRS Form 940 below.

Is there a Form 940 for correcting employment taxes?

Correcting Employment Taxes. In addition, there is no “X” form for the Form 940, and taxpayer will continue to use a Form 940 for amended returns. For overpayments: Employers correcting an overpayment must use the corresponding “X” form. Employers can choose to either make an adjustment or claim a refund on the form.

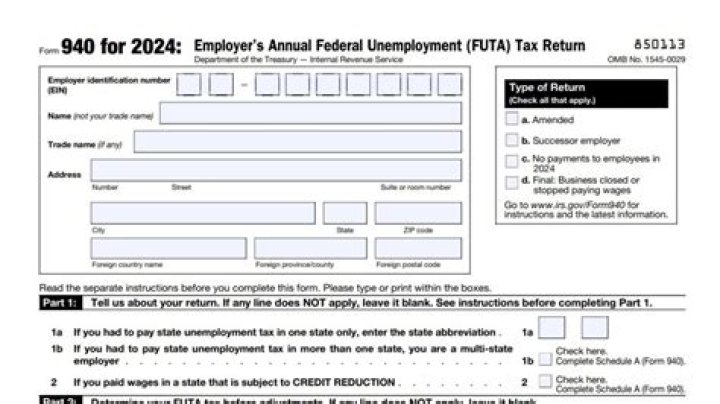

What is the federal unemployment Form 940 for 2019?

Form 940 for 2019: Employer’s Annual Federal Unemployment (FUTA) Tax Return Department of the Treasury — Internal Revenue Service. 850113. OMB No. 1545-0028. Employer identification number (EIN) — Name (not your trade name) Trade name (if any) Address

How is Futa calculated on IRS Form 940?

Part 3 calculates any addition to the FUTA tax that may be determined based on relevant state-specific information. Part 4 depicts the FUTA tax, deposits made during the year, and any balance due with Form 940, or any overpayment applied to the next years’ return.