Does Chapter 13 affect cosigner credit?

Nathan Sanders

Nathan Sanders

The Chapter 13 Codebtor Stay In Chapter 13 bankruptcy, the automatic stay protects your cosigners from creditors unless: the cosigner became liable for the debt in the ordinary course of the cosigner’s business, or. your Chapter 13 case gets dismissed, closed, or converted to a Chapter 7 or Chapter 11 bankruptcy case.

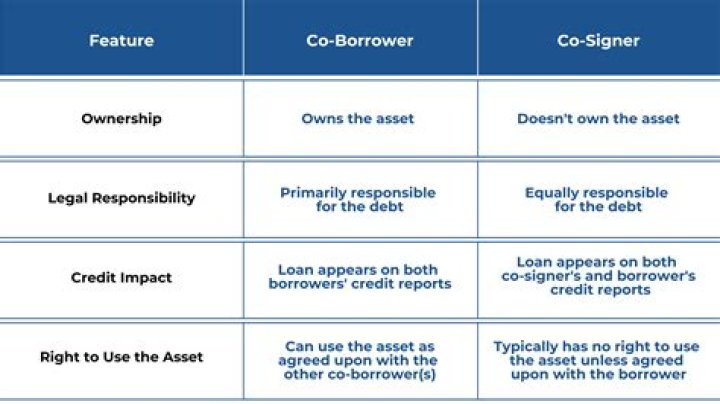

Is the cosigner the guarantor?

The most important difference between a cosigner and a guarantor is that a cosigner is immediately responsible for paying rent, just as the tenant is. A guarantor is only responsible for paying rent when the tenant fails to do so themselves.

Is it better to have a cosigner or guarantor?

Co-signers can help you secure a lease while also helping save money because you’re splitting the rent equally. A guarantor is a good option when you’re looking to live alone or don’t want a roommate but need someone to back you up financially in order to obtain the lease.

Can you cosign for a car while in Chapter 13?

With a Chapter 13 bankruptcy filing, the automatic stay extends to cosigners, too. In fact, if the borrower’s repayment plan doesn’t say they’re repaying the debt in full, the collector can petition the court to lift the automatic stay so they can pursue you even before the bankruptcy is complete.

Will Chapter 13 lower my car payment?

Your best chance of reducing your car payment is through Chapter 13 bankruptcy. This is known as a “cram down.” In a cram down, if the balance of your loan is more than your car is worth, then you can pay back the balance based on the current value rather than the contracted loan balance.

Can I pay cash for a car while in Chapter 13?

A bankruptcy debtor may buy a car with cash during an open Chapter 13 case without permission from the trustee or bankruptcy court. As always, it is advisable to speak with your attorney before making a large cash purchase during Chapter 13 bankruptcy.

What happens to the cosigner of a car loan in bankruptcy?

After you file bankruptcy, the co-signer becomes liable for the debt. At that point, the co-signer must either pay the debt off or can file for bankruptcy themselves to no longer be liable for the loan on the vehicle. If you are the co-signer of a loan and you file bankruptcy,…

What happens to your car when you file Chapter 13 bankruptcy?

Here are a few that apply to vehicles. You can stop a repossession. When you file for Chapter 13 bankruptcy, most creditors must stop any collection efforts against you as the result of an order called the “automatic stay.”. If you’ve already filed for Chapter 13 bankruptcy, a car lender can’t repossess your car.

How does Chapter 13 affect cosigners and joint accounts?

Your Chapter 13 repayment plan does not propose to pay the cosigned debt. The creditor’s interest will be irreparably harmed if the codebtor stay remains in effect. Further, the Chapter 13 codebtor stay will end if your case is closed, dismissed, or converted to a Chapter 7 bankruptcy.

What happens to my brother in Chapter 13 bankruptcy?

Dan’s Chapter 13 plan does not propose to repay the car loan. The creditor can lift the codebtor stay. Example 3. Again, Dan takes out a car loan and his brother Ken cosigns on the loan. Dan files Chapter 13, but six months into his plan, he stops making his payments, and the creditor is not getting paid. The car is rapidly depreciating in value.