How are loans to S corporation shareholders accounted for?

Robert Harper

Robert Harper

Loans to S Corporation Shareholder. Often times a payment or payments to S corporation shareholders will be booked or accounted for as a loan to shareholder. Sometimes this is purposefully, other times, it may be due to lack of options.

How do I record the payments SBA is making?

I have an EXISTING SBA loan I”m NOT referencing the PPP or EDL loan. SBA is making six months of payments directly to the bank under the CARES Act. How do I record those payments in QB?

How are capital accounts reported in a S corporation?

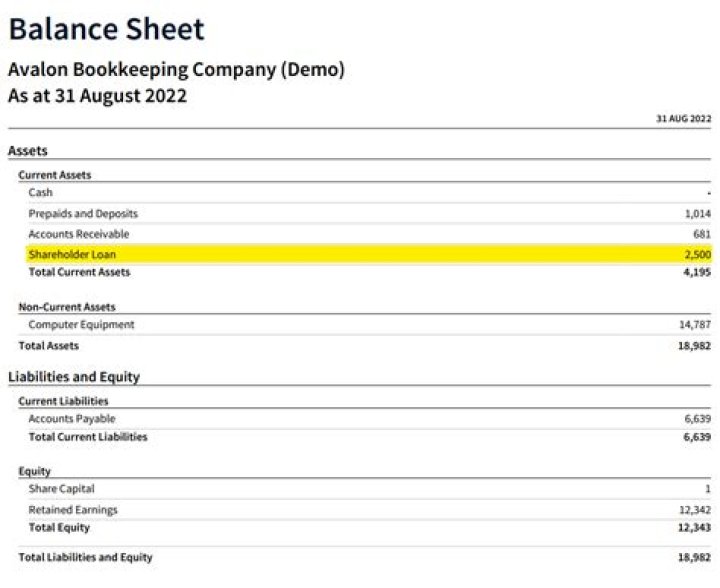

S Corporation Capital Accounts The capital accounts come into play in two crucial aspects of an S corporation’s financial and tax reporting. First, the capital accounts are reported on the company’s balance sheets as shareholder equity and loans from shareholders. Then each shareholder’s capital account can be summarized on Form 1120S Schedule K-1.

Who are the owners of an S corporation?

Credibility: Corporations are often perceived as a more legitimate entity than a sole proprietorship or general partnership. Have no more than 100 employees. Owners must be US citizens or permanent residents. Unlike a C corporation, an S corporation is not eligible for a “dividends received” deduction.

Do you have to pay taxes on a shareholder loan?

The IRS may be critical of shareholder loans and argue that payments made to shareholders should be reclassified as salary (which incurs payroll taxes) or as an equity transaction. For example, the IRS might say the payments from a C corporation are actually dividends which are taxable to the owner personally as ordinary income.

What are the rules for loaning money to shareholders?

If your business loans are more than $10,000 to a shareholder, you must charge what the IRS considers an “adequate” rate of interest. If not, payments to shareholders may be subject to a complicated set of below-market interest rules.

What are the benefits of loan to shareholders?

The benefit of making a loan comes in the form of getting the money repaid without the need to disburse money to other shareholders. However, repayment of the loan has to be handled carefully as it can cause the shareholder to be responsible for taxes on that income. The S corporation has the option to pass through losses to the owners.

Can a sole shareholder get an interest free loan?

An interest-free loan from an S corporation to its sole shareholder would, absent earnings and profits, have no effect on the shareholder or the corporation.

How does a shareholder acquire a S corporation basis?

A shareholder acquires S corporation basis through the original purchase of stock; additional equity contributions; and cumulative net income, less distributions passed through to the shareholder during the time the stock is owned. Additionally, a shareholder acquires debt basis from loans made to the S corporation.

Can a shareholder take out a personal loan?

Another alternative is making the corporation wait to repay the shareholder debt until there is a year with positive net income to restore most or all of the loan basis. Or the shareholder can take out a personal loan that’s separate from the business and avoid repayment from the corporation in a year that shows a loss.

Can a noncontrolling shareholder impute interest under Sec 7872?

Observation: The Tax Court has made it clear that the IRS can impute interest under Sec. 7872 on below-market loans from a corporation to noncontrolling shareholders ( Rountree Cotton Co., 113 T.C. 422 (1999), aff’d, 12 Fed. App’x 641 (10th Cir. 2001)).

When to seek outside counsel for a s-Corp loan?

Nevertheless, they will try to help the shareholder and S-Corp avoid unintended tax consequences by consulting with an attorney. In cases where a shareholder has transferred, distributed, or lent money to themselves, family members, or other related corporations it is important to seek outside counsel.

How are S-Corp owners get themselves into trouble?

There are a number of ways S-Corp owners get themselves into trouble when it comes to distributing money to and from their corporation. 1. Took distributions throughout the year but did not classify anything as reasonable compensation