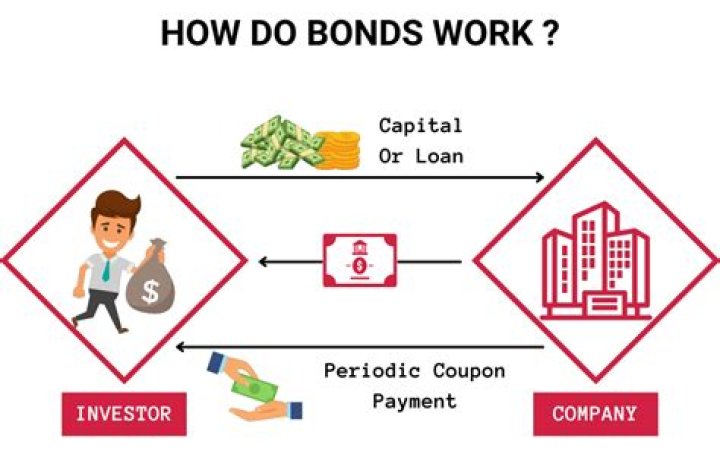

How do bonds work coupon?

Isabella Wilson

Isabella Wilson

A coupon payment on a bond is the annual interest payment that the bondholder receives from the bond’s issue date until it matures. For example, if a bond has a face value of $1,000 and a coupon rate of 5%, then it pays total coupons of $50 per year. Typically, this will consist of two semi-annual payments of $25 each.

What is a coupon in bond?

A coupon or coupon payment is the annual interest rate paid on a bond, expressed as a percentage of the face value and paid from issue date until maturity. It is also referred to as the “coupon rate,” “coupon percent rate” and “nominal yield.”

Which of the following is true for a coupon bond?

The correct answer to the given question is option A. When the coupon bond is priced at its face value, the yield to maturity equals the coupon rate.

How do you find the coupon rate of a bond?

A bond’s coupon rate can be calculated by dividing the sum of the security’s annual coupon payments and dividing them by the bond’s par value. For example, a bond issued with a face value of $1,000 that pays a $25 coupon semiannually has a coupon rate of 5%.

When yield curves are steeply upward sloping?

when the yield curve is steeply upward-sloping, short-term rates are expected to rise in the future. relatively stable in the future. A) 1 year.

How does coupon rate affect bond price?

The coupon rate on a bond vis-a-vis prevailing market interest rates has a large impact on how bonds are priced. If a coupon is higher than the prevailing interest rate, the bond’s price rises; if the coupon is lower, the bond’s price falls.

What is a zero-coupon bond example?

A zero-coupon bond is a bond that pays no interest and trades at a discount to its face value. It is also called a pure discount bond or deep discount bond. U.S. Treasury bills. are an example of a zero-coupon bond.

How do you calculate a zero-coupon bond?

The basic method for calculating a zero coupon bond’s price is a simplification of the present value (PV) formula. The formula is price = M / (1 + i)^n where: M = maturity value or face value. i = required interest yield divided by 2.