How do I calculate cost basis for investment property?

Robert Harper

Robert Harper

How Do I Calculate Cost Basis for Real Estate?

- Start with the original investment in the property.

- Add the cost of major improvements.

- Subtract the amount of allowable depreciation and casualty and theft losses.

How do you calculate asset basis?

To calculate an asset’s or security’s adjusted basis, you simply take its purchase price and then add or subtract any changes to its initial recorded value. Capital gains tax is paid on the difference between the adjusted basis and the amount the asset or investment was sold for.

What can be included in cost basis of property?

What is your cost basis?

- title fees,

- legal fees,

- recording fees,

- survey fees, and.

- any transfer or stamp taxes you pay in connection with the purchase.

How is a property owner’s adjusted basis in the property calculated?

The adjusted basis is calculated by taking the original cost, adding the cost for improvements and related expenses and subtracting any deductions taken for depreciation and depletion. Then check out how to determine the cost basis of a subdivided property.

What happens if you don’t have cost basis for stock?

If options 1 and 2 are not feasible and you are not willing to report a cost basis of zero, then you will pay a long-term capital gains tax of 10% to 20% (depending on your tax bracket) on the entire sale amount. Alternatively, you can estimate the initial price of the share.

What if cost basis is unknown?

To find an unknown cost basis for stocks and bonds, you first must determine the purchase date. If no purchase records exist, take an educated guess about when you might have bought the securities based on life events happening when they were purchased. If you inherited the stocks or bonds, find the date of death.

Why is there no cost basis on my 1099 B?

No, The cost basis is the amount that you paid for the investment. If you leave it blank you will be taxed on 100% of the proceeds. You will have to determine the basis yourself.

How do I find missing cost basis?

Subtract the amount paid at the time of purchase from the amount received at the time of sell to determine your missing cost basis.

At what age do you not pay capital gains?

The over-55 home sale exemption was a tax law that provided homeowners over the age of 55 with a one-time capital gains exclusion. The seller, or at least one title holder, had to be 55 or older on the day the home was sold to qualify.

What is adjusted basis of property sold?

Your adjusted basis is generally your cost in acquiring your home plus the cost of any capital improvements you made, less casualty loss amounts and other decreases. You may be able to exclude from income all or a portion of the gain on your home sale.

How is investment property classified under IAS 40.6?

Property held under an operating lease. A property interest that is held by a lessee under an operating lease may be classified and accounted for as investment property provided that: [IAS 40.6] An entity may make the foregoing classification on a property-by-property basis.

How is the sale of an investment property taxed?

When you sell investment property, all of your profits are subject to either capital gains tax or depreciation recapture tax, which is a special type of capital gains tax. Your tax gets calculated on the difference between your cost basis and your selling price.

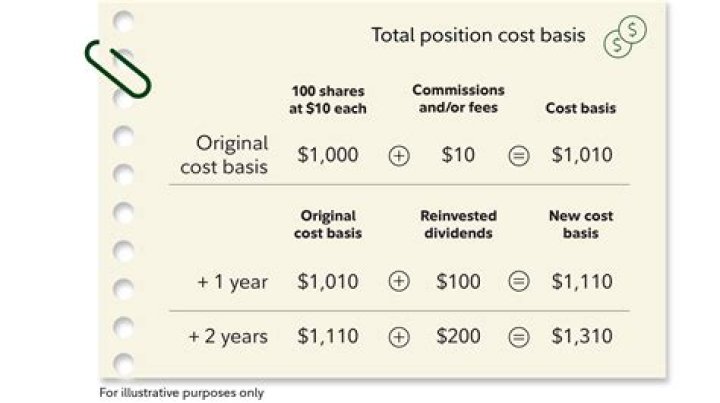

How is cost basis of investment property calculated?

Taking the apartment building as an example, a $50,000 roof and $115,000 in kitchen and bathroom renovations would count as improvements and increase your cost basis to $1.1815 million. While you own your investment property, the tax code lets you claim a small portion of its cost basis every year as a depreciation write-off.

How is investment property remeasured in the market?

Investment property is remeasured at fair value, which is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.