How do I calculate depreciation on a 1031 exchange?

Robert Harper

Robert Harper

Simply take its acquisition cost and subtract the capital gain you’re deferring in the exchange. In our example, the $200,000 acquisition cost minus the $65,000 capital gain on the relinquished property gives the same $135,000 cost basis.

How does depreciation work on a 1031 exchange?

The basic concept of a 1031 exchange is that the basis of your Old Property rolls over to your New Property. In other words, you continue your depreciation calculations as if you still own the Old Property (your acquisition date, cost, previous depreciation taken, and remaining un-depreciated basis remain the same).

Is there depreciation recapture on a 1031 exchange?

1031 Exchanges allow you to defer both the capital gains tax and depreciation recapture from the sale of a property and invest the proceeds into another “like-kind” property, often called “trading up.”

How do you depreciate like-kind exchange property?

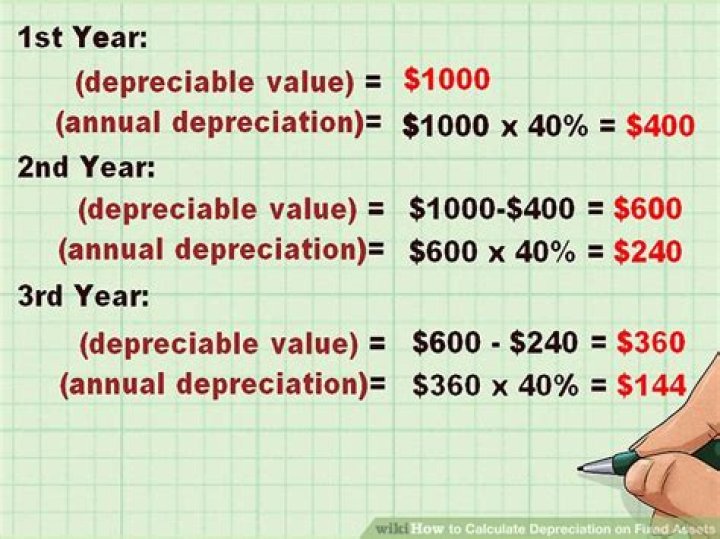

Option 1: Generally, taxpayers must depreciate the carryover basis of property acquired in a like-kind exchange during the current tax year over the remaining recovery period of the property exchanged. They must use the same depreciation method and convention that was used for the relinquished property.

Does depreciation reset?

Due to the stepped-up basis your heirs receive, that depreciation is wiped clean, and their cost basis will be the fair market value at the date of death. Even better, if it’s still a rental, they can begin depreciating it all over again.

What is the basis of the new property in a 1031 exchange?

The basic idea is that a 1031 exchange lets an investor sell one property and reinvest the proceeds into another property. They then defer paying capital gains tax. Since you’re deferring the tax liability from one property to another, this affects the cost basis (for tax purposes) of the new property you acquire.

How is depreciation recapture calculated in a 1031 exchange?

Tax deferral for both taxes is dependent upon a successful 1031 exchange. Depreciation recapture deferrals are however somewhat more nuanced than gains. With you as the exchanger, we’ll outline how depreciation recapture is calculated and deferred in a 1031 Exchange.

What kind of property is excluded from 1031 exchanges?

The tax code specifically excludes some property even if the property is used in trade or business or for investment. These excluded properties generally involve stocks, bonds, notes, securities and interests in partnerships. Property held “primarily for sale” is also excluded.

How long does it take to replace a property in a 1031 exchange?

From the time of closing on the relinquished property, the investor has 45 days to nominate potential replacement properties and a total of 180 days from closing to acquire the replacement property. Identification requirements: The investor must identify the replacement property prior to midnight on the 45th day.

What happens if there is a failed 1031 exchange?

Failed exchanges often happen if the exchanger doesn’t meet the 45 day 1031 exchange property identification period rule or other requirements. After 10 years, e.g., you sell a 39-year rental property costing $390,000 for $490,000.