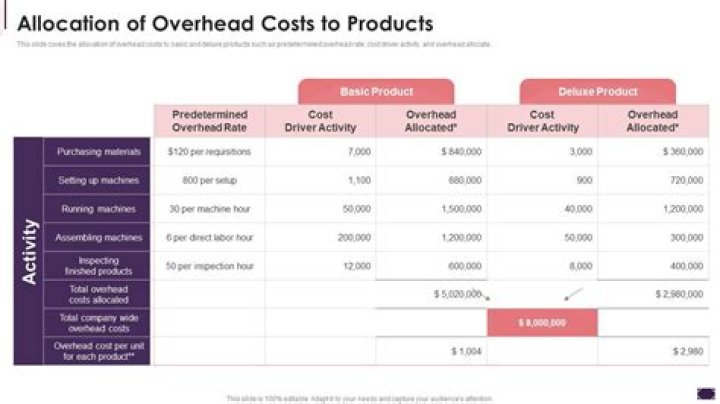

How do you allocate overhead costs for a product?

Nathan Sanders

Nathan Sanders

Allocate Overhead Costs Apply the overhead by multiplying the overhead allocation rate by the number of direct labor hours needed to make each product. If product X requires 50 hours, you must allocate $166.5 worth of overhead (50 hours x $3.33) to this product.

Why are overhead costs allocated to products?

Overhead costs are allocated to products to provide information for internal decision making, to promote the efficient use of resources, and to comply with U.S. Generally Accepted Accounting Principles.

How do you calculate overhead costs?

The overhead rate or the overhead percentage is the amount your business spends on making a product or providing services to its customers. To calculate the overhead rate, divide the indirect costs by the direct costs and multiply by 100.

Why are different ways of allocating overhead costs?

Direct, step-down and reciprocal methods of support department cost allocation gave slightly different total overhead cost and overhead rates for each production department. It is because of the different recognition that each method gives to support relationships.

Which is the correct formula for overhead allocation?

Thus, the overhead allocation formula is: Cost pool ÷ Total activity measure = Overhead allocation per unit. You can allocate overhead costs by any reasonable measure, as long as it is consistently applied across reporting periods.

What are the different types of manufacturing overhead?

Manufacturing overhead also include cost that is more appropriately to be treated as cost of all outputs like overtime premium, cost of idle time, utilities cost. Non-manufacturing cost includes customer service, marketing and research & development cost. Normally, only manufacturing overhead is allocated to products.

How are fixed and variable overhead costs allocated?

The fixed manufacturing overhead costs are not allocated or assigned to (not absorbed by) the products manufactured under variable or direct costing. Variable costing is often useful for management’s decision-making.