How do you calculate a zero-coupon bond?

Emma Jordan

Emma Jordan

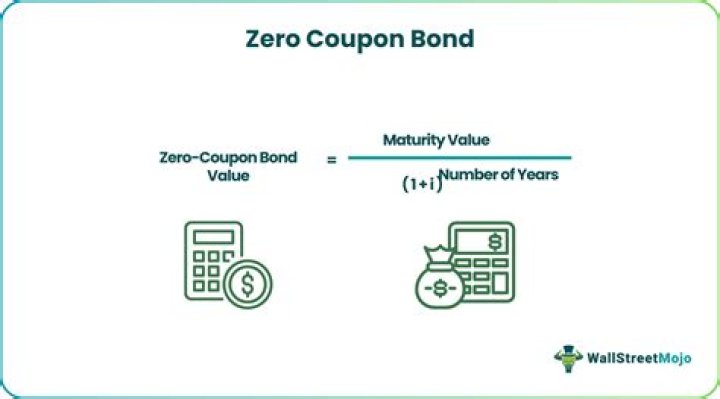

The basic method for calculating a zero coupon bond’s price is a simplification of the present value (PV) formula. The formula is price = M / (1 + i)^n where: M = maturity value or face value. i = required interest yield divided by 2.

Can you sell zero coupon bonds?

Like virtually all bonds, zero-coupon bonds are subject to interest-rate risk if you sell before maturity. If interest rates rise, the value of your zero-coupon bond on the secondary market will likely fall.

Can you lose money on a zero-coupon bond?

Since a zero coupon bond does not pay interest at the end of every quarter, the difference between the amount you receive at maturity and the amount you paid represents the interest payment. However, if you do sell prior to maturity, you could lose money because of market fluctuations.

What is the tax treatment of zero coupon bonds?

Maturity, redemption or otherwise transfer of zero coupon bonds shall be treated as transfer in the hands of investor for the purpose of capital gains tax under Section 2 (47) (iva). Income arising from zero coupon bonds as defined in Section (48) (2) shall be taxed only in the year in which same is transferred or redeemed or matured.

What’s the time horizon for a zero coupon bond?

Suitable Tenure for Zero Bond Coupon The time and the maturity value of Zero Coupon bonds share a negative correlation. The longer until the maturity date, the less the investors have to pay for it. Therefore, the Zero Coupon bonds generally come with a time horizon of 10 to 15 years.

How is the yield on a zero coupon bond calculated?

The annually Zero Coupon Bond and the semi-annual Zero Coupon Bond can be measured using two simple formulas, which are mentioned below: Both the formulas are similar except for the r or the required rate of return being divided by two and the n or years until maturity being multiplied by two for measuring the price of bond semi-annually.

When do you pay taxes on deep discount bonds?

The difference between the bid price of a deep discount bond and its redemption price, which is actually paid at the time of maturity, will continue to be subject to tax deduction at source under section 193 of the Income-tax Act.