How do you calculate call option using Black-Scholes?

Isabella Wilson

Isabella Wilson

The Black-Scholes call option formula is calculated by multiplying the stock price by the cumulative standard normal probability distribution function.

How do you use Black-Scholes?

Black Scholes Formula

- S0 is the stock price;

- e is the exponential number;

- q is the dividend yield percentage;

- T is the term (one year will be T=1, while six months will be T=0.5);

- N(d1) is the delta of the call option, meaning the change in the call price over the shift in the stock price;

- K is the strike price;

What is Q in Black-Scholes formula?

Black-Scholes Inputs r = continuously compounded risk-free interest rate (% p.a.) q = continuously compounded dividend yield (% p.a.) t = time to expiration (% of year)

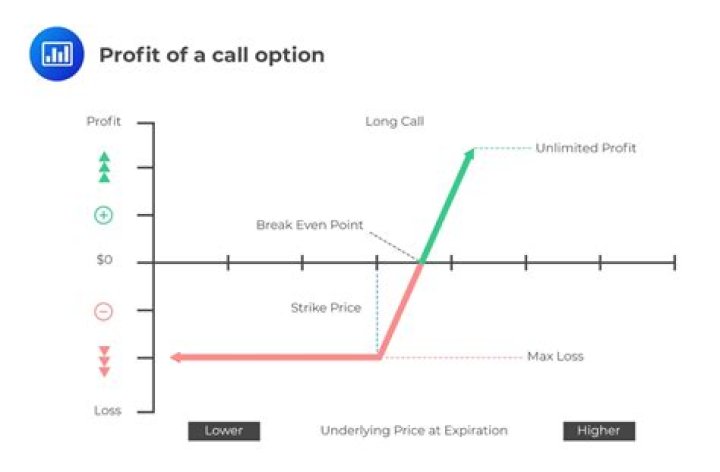

How is call price calculated?

Calculate the call price by calculating the cost of the option. The bond has a par value of $1,000, and a current market price of $1050. This is the price the company would pay to bondholders. The difference between the market price of the bond and the par value is the price of the call option, in this case $50.

Does Black-Scholes model work?

The Black-Scholes model does not account for the early exercise of American options. In reality, few options (such as long put positions) do qualify for early exercises, based on market conditions. Traders should avoid using Black-Scholes for American options or look at alternatives such as the Binomial pricing model.

What is Black-Scholes used for?

Definition: Black-Scholes is a pricing model used to determine the fair price or theoretical value for a call or a put option based on six variables such as volatility, type of option, underlying stock price, time, strike price, and risk-free rate.

What are the limitations of Black-Scholes model?

Some of the standard limitations of the Black-Scholes model are: Assumes constant values for risk-free rate of return and volatility over the option duration. None of those may remain constant in the real world. Assumes continuous and costless trading—ignoring liquidity risk and brokerage charges.

What is call and put price?

From a buyer’s perspective, a call gives you the right to buy an underlier at a predetermined price from the seller on a particular date. A put gives you the right to sell an underlier at a preset price on a particular date to the seller. Currently, only the difference is exchanged between the buyer and the seller.

How accurate is Black-Scholes model?

Regardless of which curved line considered, the Black-Scholes method is not an accurate way of modeling the real data. Due to these differences between the Black-Scholes prices and those of the actual stocks, the conclusion can be made that the model is not too accurate in pricing call options.

What is Black Scholes used for?

Why is Black-Scholes not accurate?

Limitations of the Black-Scholes Model Assumes constant values for risk-free rate of return and volatility over the option duration. None of those may remain constant in the real world. Assumes no early exercise (e.g., fits only European options). That makes the model unsuitable for American options.