How do you calculate interest capitalization?

Aria Murphy

Aria Murphy

You can use a capitalized interest calculator, but the formula for figuring interest capitalization is straightforward. Multiply the average amount borrowed during the time it takes to acquire the asset by the interest rate and the development time in years.

What assets qualify for interest capitalization?

When to capitalize interest cost

- Assets constructed for an entity’s own use.

- Assets constructed for an entity by a supplier, with deposits or progress payments having been made.

- Assets intended for sale or lease that are constructed as discrete projects (such as a cruise ship).

When Should interest be capitalized?

Interest is only capitalized during the period under which the asset is being prepared for its intended use. The purpose of this is to obtain a more accurate representation of the full costs incurred in acquiring or constructing the asset.

Is capitalized interest an intangible asset?

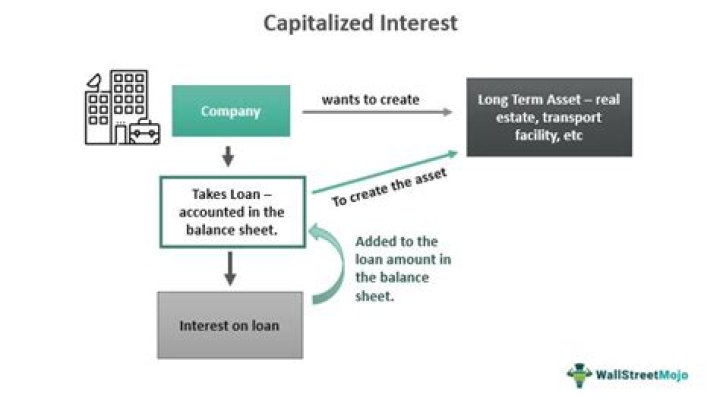

Accounting for Capitalized Interest This interest is added to the cost of the long-term asset, so that the interest is not recognized in the current period as interest expense. Instead, it is now a fixed asset, and is included in the depreciation of the long-term asset.

Why do companies capitalize interest?

Because many companies finance long-term assets with debt, companies are allowed to expense the assets over the long-term. By capitalizing the interest expense, companies are able to generate revenue from the asset in order to pay for it over time.

Can a bank capitalize interest?

Capitalization of interest should be based upon the borrower’s ability to discharge the indebtedness in the normal course of business. Capitalized interest on loans is generally defined as uncollected interest which is added to unpaid principal in accordance with the contractual loan agreement.

Is it permissible to capitalize interest cost of assets?

However, interest cannot be capitalized for inventories that are routinely manufactured or otherwise produced in large quantities on a repetitive basis. The amount capitalized is to be an allocation of the interest cost incurred during the period required to complete the asset.

Is capitalized interest an expense?

Capitalized interest is an accounting practice required under the accrual basis of accounting. Capitalized interest is interest that is added to the total cost of a long-term asset or loan balance. This makes it so the interest is not recognized in the current period as an interest expense.

How is capitalized interest treated?

Instead, capitalized interest is treated as part of the fixed asset or loan balance and is included in the depreciation of the long-term asset or loan repayment. Capitalized interest appears on the balance sheet rather than the income statement.

What does capitalize interest mean?

Interest capitalization occurs when unpaid interest is added to the principal amount of your student loan. Interest is then charged on that higher principal balance, increasing the overall cost of the loan (since interest will now be charged on the higher principal amount).

What is capitalization journal entry?

When you capitalize an asset in the period you added it, Oracle Assets creates the following journal entries: When you capitalize an asset in a period after the period you added it, Oracle Assets creates journal entries that transfer the cost from the CIP cost account to the asset cost account.

What is my capitalization limit?

A capitalization limit (“cap limit”) is the threshold above which an entity capitalizes purchased or constructed assets. Below the cap limit, you generally charge purchases to expense instead.

How do I get rid of capitalized interest?

You can avoid capitalized interest on student loans in the following ways: Make interest payments monthly while you’re in school. Paying the interest on unsubsidized loans during an in-school deferment will help you avoid capitalization costs, as will avoiding deferment or forbearance altogether.

Why is capitalization important?

They have three main purposes: to let the reader know a sentence is beginning, to show important words in a title, and to signal proper names and official titles. This is a stable rule in our written language: Whenever you begin a sentence capitalize the first letter of the first word.

Interest is capitalized in order to obtain a more complete picture of the total acquisition cost associated with an asset, since an entity may incur a significant interest expense during the acquisition and start-up phases of the asset.

Is capitalized interest a fixed asset?

What are the types of capitalization?

Capitalisation may be of 3 types. They are over capitalisation, under capitalisation and fair capitalisation. Among these three over capitalisation is likely to be of frequent occurrence and practical interest.

Is it better to capitalize or expense?

When a cost that is incurred will have been used, consumed or expired in a year or less, it is typically considered an expense. Conversely, if a cost or purchase will last beyond a year and will continue to have economic value in the future, then it is typically capitalized.

Is interest capitalization legal?

Understanding Capitalized Interest Capitalizing interest is not permitted for inventories that are manufactured repetitively in large quantities. U.S. tax laws also allow the capitalization of interest, which provides a tax deduction in future years through a periodic depreciation expense.

What is the definition of capitalized interest in accounting?

Capitalized interest. Capitalized interest is the cost of the funds used to finance the construction of a long-term asset that an entity constructs for itself.

When to capitalize interest cost in an ACQ?

Interest is capitalized in order to obtain a more complete picture of the total acquisition cost associated with an asset , since an entity may incur a significant interest expense during the acquisition and start-up phases of the asset. Interest expense should be included in the cost of acq

When to capitalize interest under avoided cost method?

Capitalization of interest under the avoided cost method described in § 1.263A-9 is required with respect to the production of designated property described in paragraph (b) of this section. (2) Treatment of interest required to be capitalized.

How is interest capitalized in a designated property?

Interest capitalized with respect to designated property that includes both components subject to an allowance for depreciation or depletion and components not subject to an allowance for depreciation or depletion is ratably allocated among, and is treated as a cost of, components that are subject to an allowance for depreciation or depletion .