How do you calculate market risk premium for CAPM?

Joseph Russell

Joseph Russell

The market risk premium can be calculated by subtracting the risk-free rate from the expected equity market return, providing a quantitative measure of the extra return demanded by market participants for the increased risk. Once calculated, the equity risk premium can be used in important calculations such as CAPM.

What is risk-free rate and risk premium?

The risk-free rate refers to the rate of return on a theoretically riskless asset or investment, such as a government bond. All other financial investments entail some degree of risk, and the return on the investment above the risk-free rate is called the risk premium.

How do you calculate risk-free rate using CAPM?

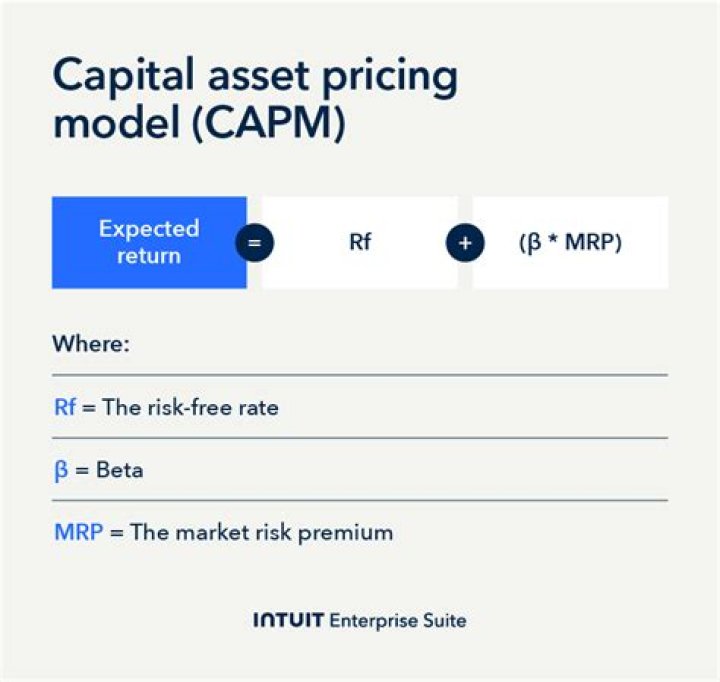

The amount over the risk-free rate is calculated by the equity market premium multiplied by its beta. In other words, it is possible, by knowing the individual parts of the CAPM, to gauge whether or not the current price of a stock is consistent with its likely return.

What is a market risk premium?

The market risk premium is the rate of return on a risky investment. The market risk premium is used by investors who have a risky portfolio, rather than assets that are risk-free. It is part of the Capital Asset Pricing Model which is used to work out rates of return on investments.

What is the current market risk premium 2021?

The average market risk premium in the United States declined slightly to 5.5 percent in 2021. This suggests that investors demand a slightly higher return for investments in that country, in exchange for the risk they are exposed to. This premium has hovered between 5.3 and 5.7 percent since 2011.

What is nominal risk-free rate?

nominal risk-free interest rate. Essentially, the real risk-free interest rate refers to the rate of return required by investors on zero-risk financial instruments without inflation. Since this doesn’t exist, the real risk-free interest rate is a theoretical concept.

What is the current market risk premium 2020?

Duff & Phelps Recommended U.S. Equity Risk Premium Increased from 5.0% to 6.0% Effective March 25, 2020.

Can the market risk premium be negative?

A negative risk premium occurs when a particular investment results in a rate of return that’s lower than that of a risk-free security. And it isn’t just low-risk investments that can have a negative risk premium. During the 20-year period from 1963 to 1983, the stock market had a negative risk premium.

What is the long term market risk premium?

Historical market risk premium refers to the difference between the return an investor expects to see on an equity portfolio and the risk-free rate of return. The historical market risk premium can vary by as much as 2% because investors have different investing styles and different risk tolerance.

Can you lose money on T-bills?

Treasury bonds are considered risk-free assets, meaning there is no risk that the investor will lose their principal. In other words, investors that hold the bond until maturity are guaranteed their principal or initial investment.

What should I use as the risk-free rate?

Most often, either the current Treasury bill, or T-bill, rate or long-term government bond yield are used as the risk-free rate. T-bills are considered nearly free of default risk because they are fully backed by the U.S. government.

Where can I find risk-free rate?

The risk-free rate represents the interest an investor would expect from an absolutely risk-free investment over a specified period of time. The real risk-free rate can be calculated by subtracting the current inflation rate from the yield of the Treasury bond matching your investment duration.

Is a higher risk premium better?

As a rule, high-risk investments are compensated with a higher premium. Most economists agree the concept of an equity risk premium is valid: over the long term, markets compensate investors more for taking on the greater risk of investing in stocks.

Is higher market risk premium better?

A higher premium implies that you would invest a greater share of your portfolio into stocks. The capital asset pricing also relates a stock’s expected return to the equity premium. A stock that is riskier than the broader market—as measured by its beta—should offer returns even higher than the equity premium.