How do you calculate the basis of replacement property in a 1031 exchange?

Aria Murphy

Aria Murphy

Your basis is equal to the amount you originally paid for the property, plus any improvements you made, minus depreciation deductions. For example, say you have a rental house located at 589 Santa Sophia Ave. You bought the property for $80,000 and paid a total of $40,000 for foundation and roof work.

What’s the replacement property in a 1031 tax deferred exchange?

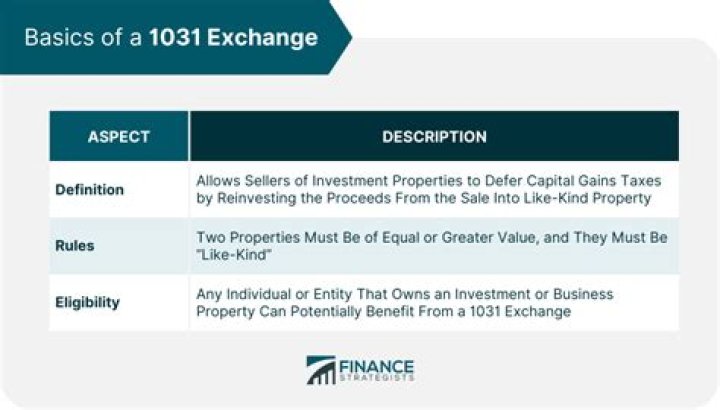

In real estate, a 1031 exchange is a swap of one investment property for another that allows capital gains taxes to be deferred. The term, which gets its name from the Internal Revenue Service (IRS) code Section 1031, is bandied about by realtors, title companies, investors, and soccer moms.

Do you get a step up in basis on a 1031 exchange?

If you are holding investment property that had been part of a 1031 Exchange, upon your death, your heirs get the Stepped-Up Basis. All of the built in gain disappears upon the taxpayer’s death. What that means is the value of the property at the date of your death would pass through your estate to your heirs.

Who is the same taxpayer in a 1031 exchange?

In a 1031 exchange, the taxpayer who owns the relinquished property must be the same taxpayer who takes ownership of the replacement property.

How is the tax basis of a replacement property calculated?

In an IRC §1031 tax-deferred exchange, the tax basis in the replacement property is reduced using a formula that takes into account the adjusted basis of the relinquished property sold in the exchange. Treas.

How many replacement properties can a taxpayer buy?

The rule most commonly used by taxpayers is the “three property rule.” Under this rule, a taxpayer can identify up to three like-kind properties as replacement property without regard to value. Since our taxpayer intends to acquire more than three replacement properties, the three property rule would not work.

Is there an exception to IRC Section 1031?

IRC Section 1031 provides an exception and allows you to postpone paying tax on the gain if you reinvest the proceeds in similar property as part of a qualifying like-kind exchange.