How do you create a trial balance from a journal entry?

Nathan Sanders

Nathan Sanders

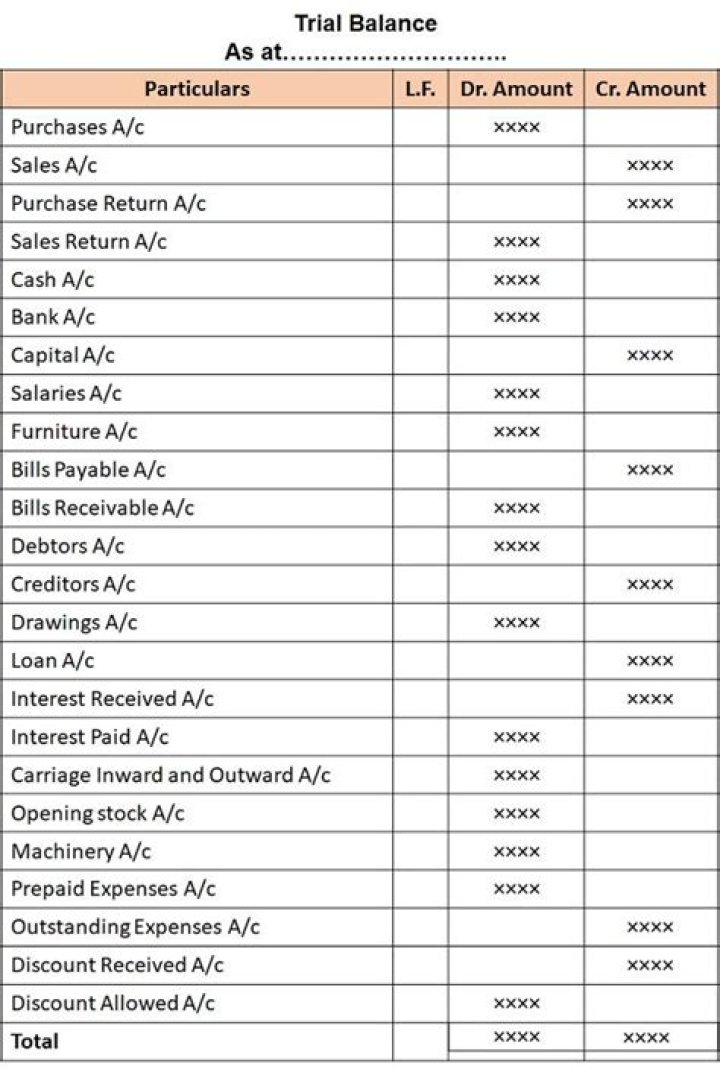

Steps in Preparation of Trial Balance

- Calculate the Balances of Each of the Ledger Accounts.

- Record Debit or Credit Balances in Trial Balance.

- Calculate Total of The Debit Column.

- Calculate Total of The Credit Column.

- Check if Debit is Equal To Credit.

How do you post entries from ledger to trial balance?

To prepare a trial balance we need the closing balances of all the ledger accounts and the cash book as well as the bank book. So firstly every ledger account must be balanced. Balancing is the difference between the sum of all the debit entries and the sum of all the credit entries.

What are the rules of journal entries and trial balance?

All assets must be on the debit side.

What are the steps for posting?

The five steps of posting from the journal to ledger include typing the account name and number, specifying the details of the journal entry, entering the debits and credits for the transaction, calculating the running debit and credit balances, and correcting any errors.

What is the journal entry for balance?

A journal entry is called “balanced” when the sum of debit side amounts equals to the sum of credit side amounts. This form looks like a letter “T”, so it is called a T-account. T-account is a convenient form to analyze accounts, because it shows both debit and credit sides of the account.

How do you post entries in a trial balance?

Post-Closing Trial Balance

- Unadjusted trial balance – This is prepared after journalizing transactions and posting them to the ledger.

- At the end of the period, the following closing entries were made:

- Income Summary is then closed to the capital account as shown in the third closing entry.

How do you prepare journal entries?

4.4 Preparing Journal Entries

- Describe the purpose and structure of a journal entry.

- Identify the purpose of a journal.

- Define “trial balance” and indicate the source of its monetary balances.

- Prepare journal entries to record the effect of acquiring inventory, paying salary, borrowing money, and selling merchandise.

When is trial balance prepared with journal entries?

If there is any error, it is rectified with journal entries. Trial balance can be prepared at any time. Generally, it is prepared at the end of every month. But it can be prepared quarterly or half yearly. It is compulsorily prepared at the close of every accounting period to verify the arithmetical accuracy of the ledger accounts.

How does a journal entry affect an account balance?

A debit is an entry made on the left side of an account, while a credit is an entry on the right side of an account. These entries, which are recorded in chronological order, each have an effect on account balances. Once transactions have been journalized, they’re posted. To post a journal entry means to transfer that entry to the general ledger.

What’s the difference between a general ledger and a trial balance?

In addition, it should state the final date of the accounting period for which the report is created. The main difference from the general ledger is that the general ledger shows all of the transactions by account, whereas the trial balance only shows the account totals, not each separate transaction.

What is the purpose of a second trial balance?

Once all necessary adjustments are done a new second trial balance is prepared to ensure that it is still balanced. This new trial balance is called the adjusted trial balance. Its purpose is to be certain that the total amount of debit balance in the general ledger is equal to the total amount of credit balance in the general ledger.