How do you extend an extended trial balance?

Aria Murphy

Aria Murphy

Study tips: How to successfully extend a trial balance

- Divide the ETB into the accounts that go on each financial statement.

- Extend the highlighted SPL accounts across to the SPL columns, adjusting them as required.

- Calculate the profit or loss.

- Extend the SFP rows, adjusting as necessary.

Is cash recorded in trial balance?

A trial balance is a conglomerate of or list of debit and credit balances extracted from various accounts in the ledger including cash and bank balances from cash book. The rule to prepare trial balance is that the total of the debit balances and credit balances extracted from the ledger must tally.

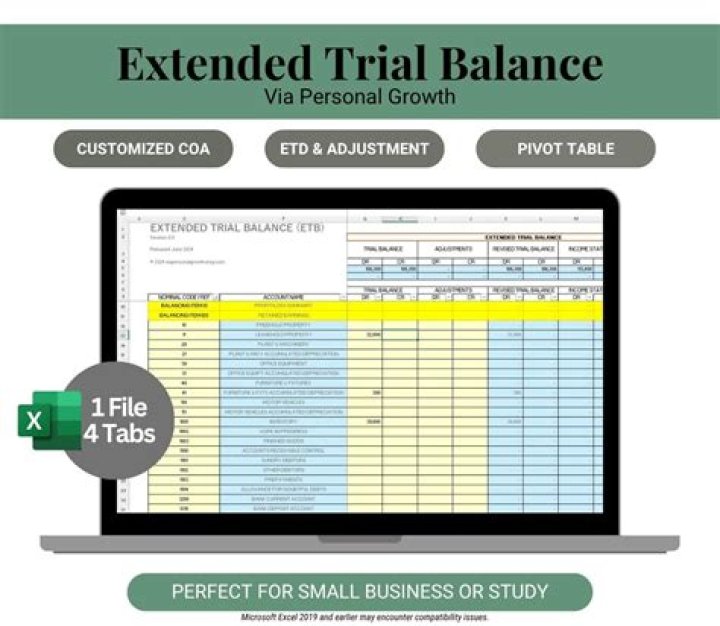

How does extended trial balance work?

An extended trial balance is a standard trial balance to which are added columns extending to the right, and in which are listed the following categories: Initial balances per general ledger. The total of all initial balance debits should equal the total of all initial balance credits. Adjusting journal entries.

Why would you use an extended trial balance?

Use the extended trial balance to see the sum of the movements (adjustments) made to each nominal account in the current set of accounts. This view helps you see what adjustments have been made and how they have affected the profit.

Why is extended trial balance used?

Where are the adjusting entries recorded?

general ledger

Adjusting journal entries are recorded in a company’s general ledger at the end of an accounting period to abide by the matching and revenue recognition principles. The most common types of adjusting journal entries are accruals, deferrals, and estimates.

Which of the following error in the journal entry will not be detected by trial balance?

The following errors will not be disclosed by the trial balance: Errors of complete omission (transaction is not recorded) Errors of commission (transaction credited to wrong account, but correct amount and correct side) Recording wrong amount in subsidiary book (wrong amount on both the debit and credit sides)