How do you find the coefficient of variation?

John Peck

John Peck

The formula for the coefficient of variation is: Coefficient of Variation = (Standard Deviation / Mean) * 100. In symbols: CV = (SD/x̄) * 100. Multiplying the coefficient by 100 is an optional step to get a percentage, as opposed to a decimal.

What is a good coefficient of variation?

Basically CV<10 is very good, 10-20 is good, 20-30 is acceptable, and CV>30 is not acceptable.

What is the investment’s coefficient of variation?

The coefficient of variation (COV) is the ratio of the standard deviation of a data set to the expected mean. Investors use it to determine whether the expected return of the investment is worth the degree of volatility, or the downside risk, that it may experience over time.

Why do we calculate coefficient of variation?

The coefficient of variation shows the extent of variability of data in a sample in relation to the mean of the population. In finance, the coefficient of variation allows investors to determine how much volatility, or risk, is assumed in comparison to the amount of return expected from investments.

Can coefficient of variation be more than 100?

For the pizza delivery example, the coefficient of variation is 0.25. This value tells you the relative size of the standard deviation compared to the mean. Analysts often report the coefficient of variation as a percentage. If the value equals one or 100%, the standard deviation equals the mean.

What is coefficient skewness?

The coefficient of skewness is a measure of asymmetry in the distribution. A positive skew indicates a longer tail to the right, while a negative skew indicates a longer tail to the left. A perfectly symmetric distribution, like the normal distribution, has a skew equal to zero.

What is a bad coefficient of variation?

As a rule of thumb, a CV >= 1 indicates a relatively high variation, while a CV < 1 can be considered low. This means that distributions with a coefficient of variation higher than 1 are considered to be high variance whereas those with a CV lower than 1 are considered to be low-variance.

Can coefficient of variation be greater than 1?

The coefficient of variation is common in applied probability fields like renewal theory, queuing theory, and reliability theory. Distributions with a coefficient of variation to be less than 1 are considered to be low-variance, whereas those with a CV higher than 1 are considered to be high variance.

What is a risky coefficient of variation?

Coefficient of variation is a measure used to assess the total risk per unit of return of an investment. It is calculated by dividing the standard deviation of an investment by its expected rate of return. Sharpe ratio is a similar statistic which measures excess return per unit of risk. …

Can coefficient of variation be greater than 100?

Variance of a Dara set can be more than 1 or any positive number. It depends on the data values. However, if the variable is Normal and has been changed to a Standard Normal Variate by standardizing it, then the variance ( or the Std. Deviation) cannot be more than 1 by definition.

Is high coefficient of variation good or bad?

Is a high coefficient of variation good?

The higher the coefficient of variation, the greater the level of dispersion around the mean. When we are presented with estimated values, the CV relates the standard deviation of the estimate to the value of this estimate. The lower the value of the coefficient of variation, the more precise the estimate.

Can coefficient of variation be less than 1?

Distributions with a coefficient of variation to be less than 1 are considered to be low-variance, whereas those with a CV higher than 1 are considered to be high variance.

What is Kelly’s coefficient of skewness?

A left-skewed distribution. Kelly’s Measure of Skewness is one of several ways to measure skewness in a data distribution. Bowley’s skewness is based on the middle 50 percent of the observations in a data set. Kelly’s measure is based on P90 (the 90th percentile) and P10 (the 10th percentile).

How do you interpret the skewness coefficient?

Interpretation

- The direction of skewness is given by the sign.

- The coefficient compares the sample distribution with a normal distribution.

- A value of zero means no skewness at all.

- A large negative value means the distribution is negatively skewed.

- A large positive value means the distribution is positively skewed.

How do you interpret standard deviation and coefficient of variation?

If you know nothing about the data other than the mean, one way to interpret the relative magnitude of the standard deviation is to divide it by the mean. This is called the coefficient of variation. For example, if the mean is 80 and standard deviation is 12, the cv = 12/80 = . 15 or 15%.

How is risk coefficient calculated?

A quantitative and practical method is the following: we attributed a number from 1 (lowest risk aversion) to 5 (highest risk aversion) to an investor. We then assign this number the letter A, which is called the “risk aversion coefficient”. To get it, we use the following utility formula 1: U = E(r) – 0,5 x A x σ2.

Can coefficient of variance be greater than 1?

The standard deviation of an exponential distribution is equivalent to its mean, the making its coefficient of variation to equalize 1. Distributions with a coefficient of variation to be less than 1 are considered to be low-variance, whereas those with a CV higher than 1 are considered to be high variance.

What is a small coefficient of variation?

The coefficient of variation (CV) is the ratio of the standard deviation to the mean. The higher the coefficient of variation, the greater the level of dispersion around the mean. The lower the value of the coefficient of variation, the more precise the estimate.

How is Kelly’s coefficient of skewness calculated?

Kelly’s Measure Formula. Kelley’s absolute measure of skewness (Sk)is: Sk=P90 + P10 – 2*P50 = D9 + D1-2*D5.

How do you find the variance and coefficient of variation?

Variance: The variance is just the square of the SD. For the IQ example, the variance = 14.42 = 207.36. Coefficient of variation: The coefficient of variation (CV) is the SD divided by the mean. For the IQ example, CV = 14.4/98.3 = 0.1465, or 14.65 percent.

What is coefficient of variation class 11?

The coefficient of variation (relative standard deviation) is a statistical measure of the dispersion of data points around the mean. The metric is commonly used to compare the data dispersion between distinct series of data.

In this example, the standard deviation is 25% the size of the mean. If the value equals one or 100%, the standard deviation equals the mean. Values less than one indicate that the standard deviation is smaller than the mean (typical), while values greater than one occur when the S.D. is greater than the mean.

What is the range of coefficient of variation?

How do you find coefficient of variation in SAS?

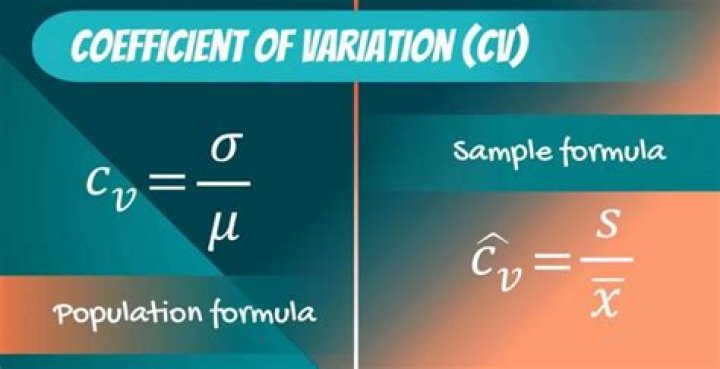

For a distribution, the coefficient of variation is the ratio of the standard deviation to the mean: CV = σ/μ. You can estimate the coefficient of variation from a sample by using the ratio of the sample standard deviation and the sample mean, usually multiplied by 100 so that it is on the percent scale.

What is the use of coefficient of variation?

The higher the coefficient of variation, the greater the level of dispersion around the mean. It is generally expressed as a percentage. The lower the value of the coefficient of variation, the more precise the estimate.

When do you use the coefficient of variation?

The coefficient of variation (CV), also known as the relative standard deviation (RSD) is commonly used in probability.

Is the coefficient of variation a unitless measure?

The coefficient of variation (CV) is a relative measure of variability that indicates the size of a standard deviation in relation to its mean. It is a standardized, unitless measure that allows you to compare variability between disparate groups and characteristics. It is also known as the relative standard deviation (RSD).

How to calculate the pooled coefficient of variation?

where V1 and V2 are the coefficients of variation for the two samples of size n1 and n2 and the pooled coefficient of variation is The 1 – α confidence interval for the difference between the population coefficients of variation is The test works best when the sample sizes are at least 10 and the population coefficients are at most .33.

When to use the coefficient of variation ( RSD )?

It is a standardized, unitless measure that allows you to compare variability between disparate groups and characteristics. It is also known as the relative standard deviation (RSD). In this post, you will learn about the coefficient of variation, how to calculate it, know when it is particularly useful, and when to avoid it.