How do you find variance of expected return?

Nathan Sanders

Nathan Sanders

Variance is calculated by calculating an expected return and summing a weighted average of the squared deviations from the mean return.

Is distribution the same as variance?

They each have different purposes. The SD is usually more useful to describe the variability of the data while the variance is usually much more useful mathematically. For example, the sum of uncorrelated distributions (random variables) also has a variance that is the sum of the variances of those distributions.

What is the variance of the stock’s returns?

A stock’s historical variance measures the difference between the stock’s returns for different periods and its average return. A stock with a lower variance typically generates returns that are closer to its average.

What is the standard deviation of the return on asset 1 and on asset 2?

The standard deviation of Asset 1 is 31.94%and the standard deviation of Asset 2 is 29.24%.

How do you find the variance of a distribution?

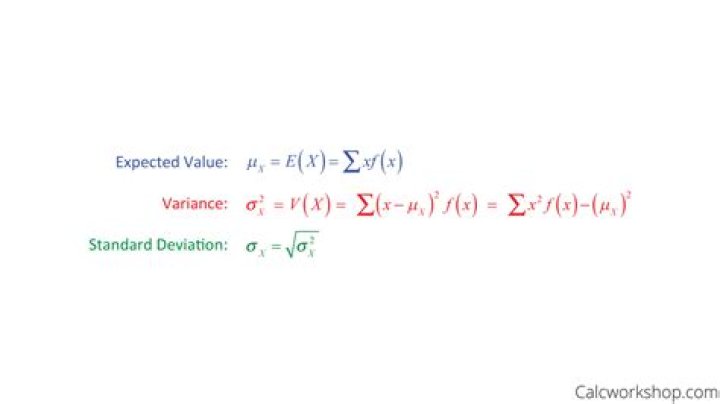

The variance (σ2), is defined as the sum of the squared distances of each term in the distribution from the mean (μ), divided by the number of terms in the distribution (N). You take the sum of the squares of the terms in the distribution, and divide by the number of terms in the distribution (N).

How do you find the variance of a normal distribution?

To calculate the variance follow these steps:

- Work out the Mean (the simple average of the numbers)

- Then for each number: subtract the Mean and square the result (the squared difference).

- Then work out the average of those squared differences. (Why Square?)

How do you calculate the variance of a three asset portfolio?

Variance of individual assets

- Calculate the arithmetic mean (i.e. average) of the asset returns.

- Find out difference between each return value from the mean and square it.

- Sum all the squared deviations and divided it by total number of observations.

How can portfolio variance be reduced?

Modern portfolio theory says that portfolio variance can be reduced by choosing asset classes with a low or negative correlation, such as stocks and bonds, where the variance (or standard deviation) of the portfolio is the x-axis of the efficient frontier.

What is a good portfolio standard deviation?

Standard deviation allows a fund’s performance swings to be captured into a single number. For most funds, future monthly returns will fall within one standard deviation of its average return 68% of the time and within two standard deviations 95% of the time.

What does the minimum variance portfolio tell us?

Definition: A minimum variance portfolio indicates a well-diversified portfolio that consists of individually risky assets, which are hedged when traded together, resulting in the lowest possible risk for the rate of expected return.

What is the variance of a distribution?

How do you find the mean and variance of a normal distribution?

We write X∼N(μ,σ2). If Z is a standard normal random variable and X=σZ+μ, then X is a normal random variable with mean μ and variance σ2, i.e, X∼N(μ,σ2). =Φ(x−μσ). =1σ√2πexp{−(x−μ)22σ2}….Let X∼N(−5,4).

- Find P(X<0).

- Find P(−7

- Find P(X>−3|X>−5).

What is the mean and variance of a normal distribution?

The normal distribution is the only distribution whose cumulants beyond the first two (i.e., other than the mean and variance) are zero. It is also the continuous distribution with the maximum entropy for a specified mean and variance.

What is the minimum variance set?

Minimum Variance Set: Identifies those portfolios that have the lowest level of risk for a given expected rate of return.