How do you get possessions from a repossessed car?

Robert Harper

Robert Harper

You have the right to get your items back even after your car is repossessed. You also have options with the vehicle itself. You can try to get the car back by paying off the amount due, making a new loan agreement with the lender to continue paying for the car, or filing for bankruptcy to get rid of the debt.

Can repo enter private property?

Q: Can a repo man enter private property? A: The repo man isn’t legally allowed to enter locked and secured private property – such as a garage – to take away your vehicle. But they can repossess your car, without a court order, if it’s sitting in your driveway, outside your home, or in a public space.

How long does a car repossession stay on your record?

seven years

A repossession can stay on your credit report for up to seven years, making it harder for you to qualify for other loans. Repossessions have a severely negative impact on your credit and can show lenders that you may not be able to make payments on the property you purchase.

How do I get my stuff back from a repossession?

During the act of repossession, you should ask the agent to return your goods. If he refuses or wants convenience money, call the cops. If you find that your vehicle is towed away with things inside, contact the lender immediately. Go to where the car is garaged, and ask them to return your belongings.

What happens to the stuff in your car when it gets repossessed?

If your car is repossessed, you have a right to get back your personal belongings that were in the car. If you default on your car loan, the lender has the right to repossess and sell your vehicle because your car is the collateral for the loan. So, you have a right to get your personal belongings back.

What are typical repossession fees?

Some agents told us that they charge $375 and up for repossessing a vehicle. Agencies typically charge storage fees on a daily basis, which can add up quickly. We spoke with companies in Florida, Kansas, and Oregon, and their fees ranged between $20 and $50 per day for storage.

How long does a repo hurt your credit?

A repossession takes seven years to come off your credit report. That seven-year countdown starts from the date of the first missed payment that led to the repossession. When you finance a vehicle, the lender owns it until it is completely paid off.

Can I buy a house with a repo on my credit?

The short answer is yes, you can still get a loan after a repossession. However, there are very few lenders who are willing to take a risk on someone with bad credit or negative marks on their credit report. Those who are willing may require you to pay higher interest rates and fees.

What happens to my personal property when my car is Repo?

If your car is repossessed, you have a right to get back your personal belongings that were in the car. If your car is repossessed and you have personal belongings in the car, what happens to that property? When a car loan lender repossesses your car, it doesn’t have a right to any personal property you have inside the car.

Can you take your things back from an impound lot?

State law says the impound lot has to give you a way to get the things in your car back. This is only the things IN the car, not parts of the car like the spare tire, battery, radios, or DVD players attached to the car. Even if it is a DVD player or accessory that you added you won’t be able to take it.

Can a repo agent charge a storage fee?

Creditors usually only have a right to charge you storage fees pertaining to the car itself. This means that the repo agent hired by a creditor to take the car also cannot charge you money or a “convenience fee” to let you get your things back before the car is towed away.

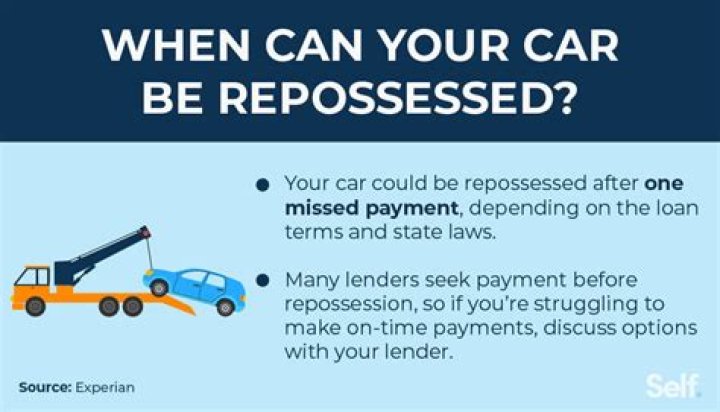

Can a car be repoed for not having insurance?

In some states, not getting insurance stipulated in a loan or lease contract can count as a default, and your car can be repoed because of it. Call your lender before jumping to conclusions so you can clarify how you can set things straight.