How do you prepare closing entries?

David Craig

David Craig

Four Steps in Preparing Closing Entries

- Close all income accounts to Income Summary.

- Close all expense accounts to Income Summary.

- Close Income Summary to the appropriate capital account. Owner’s capital account for sole proprietorship.

- Close withdrawals/distributions to the appropriate capital account.

What is included in closing entries?

What Is a Closing Entry?

- A closing entry is a journal entry made at the end of the accounting period.

- It involves shifting data from temporary accounts on the income statement to permanent accounts on the balance sheet.

- All income statement balances are eventually transferred to retained earnings.

What are the 4 steps to closing entries?

We need to do the closing entries to make them match and zero out the temporary accounts.

- Step 1: Close Revenue accounts.

- Step 2: Close Expense accounts.

- Step 3: Close Income Summary account.

- Step 4: Close Dividends (or withdrawals) account.

What is the proper order in posting closing entries?

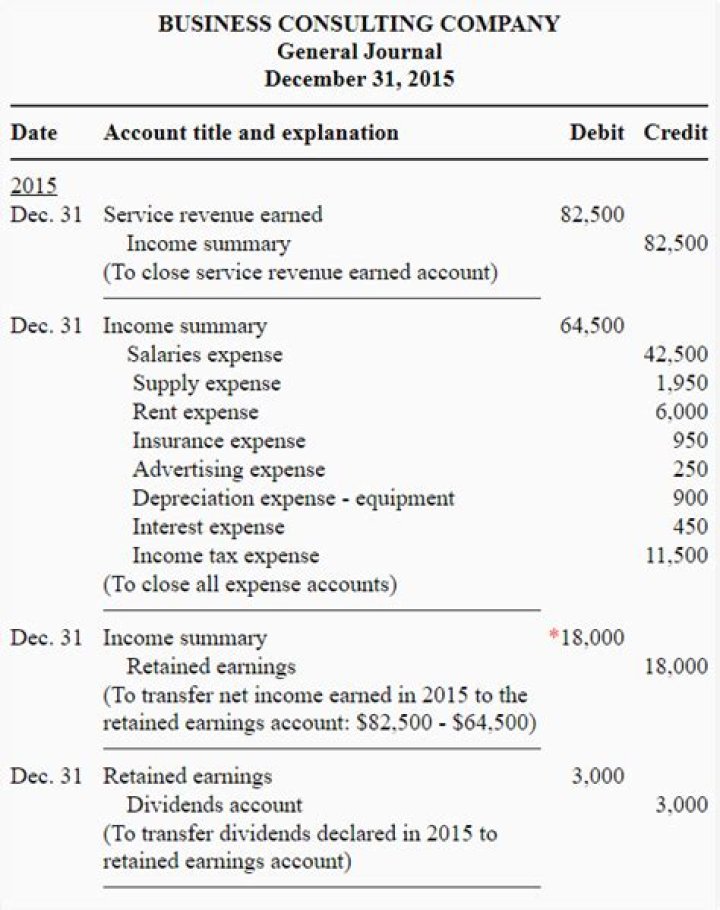

The sequence of the closing process is as follows:

- Close the revenue accounts to Income Summary.

- Close the expense accounts to Income Summary.

- Close Income Summary to Retained Earnings.

- Close Dividends to Retained Earnings.

Why are closing entries needed?

Closing entries take place at the end of an accounting cycle as a set of journal entries. The closing entries serve to transfer the balances out of certain temporary accounts and into permanent ones. This resets the balance of the temporary accounts to zero, ready to begin the next accounting period.

What are the two closing entries?

Recording closing entries: There are four closing entries; closing revenues to income summary, closing expenses to income summary, closing income summary to retained earnings, and close dividends to retained earnings.

What is income Summary In closing entries?

The income summary is a temporary account used to make closing entries. The income summary account then transfers the net balance of all the temporary accounts to retained earnings, which is a permanent account on the balance sheet.

How is the preparation of closing entries explained?

The preparation of closing entries is a simple four step process which is briefly explained below: Transfer the balances of all revenue accounts to income summary account. It is done by debiting various revenue accounts and crediting income summary account. This step closes all revenue accounts.

How are closing entries related to temporary accounts?

Closing Entries. The amounts in one accounting period should be closed or brought to zero so that they won’t be mixed with those of the next period. Temporary accounts consist of all revenue and expense accounts, and also withdrawal accounts of owner/s in the case of sole proprietorships and partnerships.

What happens to service revenue after closing entries?

After preparing the closing entries above, Service Revenue will now be zero. The expense accounts and withdrawal account will now also be zero.

What happens to income and expense accounts after closing?

In other words, the income and expense accounts are “restarted”. After preparing the closing entries above, Service Revenue will now be zero. The expense accounts and withdrawal accounts will now also be zero.