How do you use the indirect method?

David Craig

David Craig

Under the indirect method, the cash flows statement will present net income on the first line. The following lines will show increases and decreases in asset and liability accounts, and these items will be added to or subtracted from net income based on the cash impact of the item.

Why is an adjustment for depreciation expense necessary using the indirect method?

Reduce net income because cash was not received. Subtract it from net income to arrive at cash from operations. Why is an adjustment for depreciation expense necessary using the indirect method? It is easier for accrual basis income statements.

When preparing your statement of cash flows using the indirect method we would first add back?

Using the indirect method, operating net cash flow is calculated as follows: Begin with net income from the income statement. Add back noncash expenses, such as depreciation, amortization, and depletion.

Why does the FASB recommend the direct method over the indirect method?

FASB has always considered the direct method of reporting cash flows preferable to the indirect method; in FASB’s view, the direct method better achieves the cash flow statement’s primary objective (to provide relevant information about the reporting entity’s cash receipts and cash payments) and the overall objective …

What is the indirect method?

Definition: The indirect method is a reporting format for the cash flow statement that starts with net income and adjusts it for the cash operating activities during the year to arrive at the ending cash balance.

Which of the following methods is an indirect way to gather data?

Among indirect methods are surveys, exit interviews, focus groups, and the use of external reviewers. Surveys: Surveys usually are given to large numbers of possible respondents, usually in writing, and often at a distance.

Why is depreciation added back to net income in the statement of cash flows prepared using the indirect method?

Because accountants deduct depreciation in computing net income, net income understates cash from operations. Under the indirect method, since net income is a starting point in measuring cash flows from operating activities, depreciation expense must be added back to net income.

How do you calculate net cash using indirect method?

With the indirect method, cash flow is calculated by taking the value of the net income (i.e. net profit) at the end of the reporting period. You then adjust this net income value based on figures within the balance sheet and strip-out the effect of non-cash movements shown on the profit and loss statement.

What are the three steps of an indirect proof?

Here are the three steps to do an indirect proof:

- Assume that the statement is false.

- Work hard to prove it is false until you bump into something that simply doesn’t work, like a contradiction or a bit of unreality (like having to make a statement that “all circles are triangles,” for example)

Is the direct method or indirect method better?

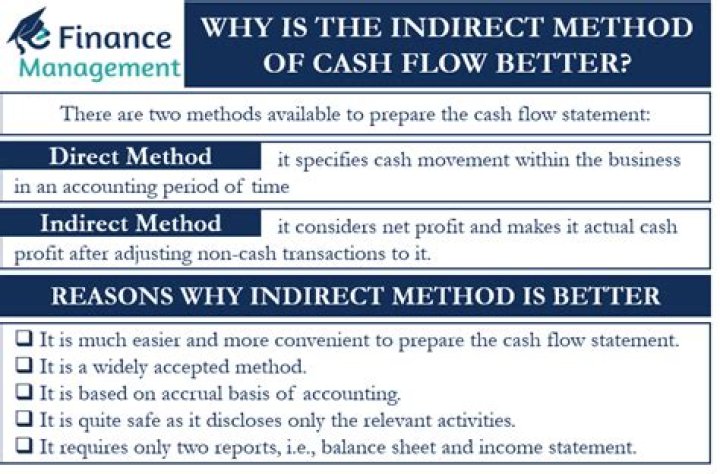

While most businesses like the indirect method because it’s easy to use, the folks at the International Accounting Standards Board prefer the direct method because it gives a clear view of cash flow receipts and payments.

What are the advantages of using the indirect method?

A major advantage of the indirect method of cash flows is that the method provides a reconciliation between net income and cash flows. The indirect method also helps financial-statement users better understand different linkages among financial statements and is a simple way of preparing the statement of cash flows.

How do you differentiate direct income from indirect income?

Direct income is one which is earned directly by way of business activities. Indirect income is one which is earned by way of non-business activities. For example, sale of old newspapers, sale of carton boxes, etc. Direct income is one which is earned directly by way of business activities.

What is the difference between the direct method and the indirect method?

The cash flow direct method determines changes in cash receipts and payments, which are reported in the cash flow from the operations section. The indirect method takes the net income generated in a period and adds or subtracts changes in the asset and liability accounts to determine the implied cash flow.

What is the indirect method in data?

Definition: Indirect assessment methods require that faculty infer actual student abilities, knowledge, and values rather than observe direct evidence. Among indirect methods are surveys, exit interviews, focus groups, and the use of external reviewers.

What is the formula of indirect method?

Which method is said to be indirect method in numerical methods?

2. Iterative Method Simultaneous linear algebraic equation occur in various fields of Science and Engineering. We know that a given system of linear equation can be solved by applying Gauss Elimination Method and Gauss – Jordon Method.

Should the direct or indirect method of reporting be used why?

The indirect method takes the net income generated in a period and adds or subtracts changes in the asset and liability accounts to determine the implied cash flow. The direct method for the statement of cash flows provides more detail about the operating cash flow accounts, although it’s time-consuming.

Which is an example of the indirect method?

It might be helpful to look at an example of what the indirect method actually looks like. As you can see, the operating section always lists net income first followed by the adjustments for expenses, gains, losses, asset accounts, and liability accounts respectively.

How to prepare an indirect method cash flow statement?

Let’s take a look at the format and how to prepare an indirect method cash flow statement. Format The indirect operating activities section always starts out with the net income for the period followed by non-cash expenses, gains, and losses that need to be added back to or subtracted from net income .

Which is the indirect method for net operating income?

The indirect method: Under indirect method (also known as reconciliation method), we convert net operating income (or loss) to net cash provide (or used) by operating activities during the year.

How is net income adjusted in statement of cash flows?

The non-cash expenses and losses must be added back in and the gains must be subtracted. The next section of the operating activities adjusts net income for the changes in asset accounts that affected cash. These accounts typically include: