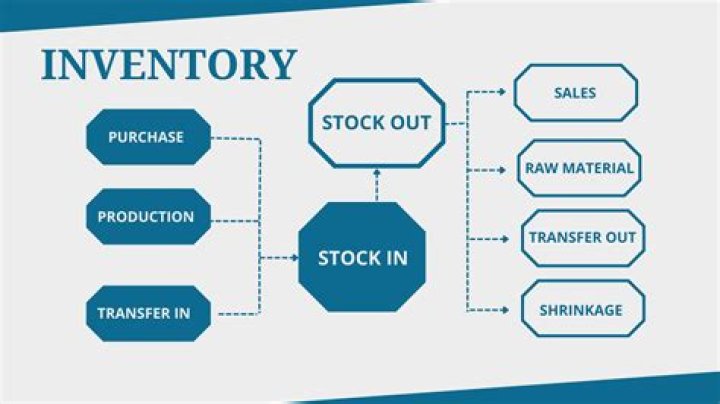

How many inventory accounts exist in a manufacturing firm?

Sophia Bowman

Sophia Bowman

Manufacturing companies normally have three inventory accounts.

What are the 3 basic types of inventory?

Raw materials, semi-finished goods, and finished goods are the three main categories of inventory that are accounted for in a company’s financial accounts. There are other types as well which are maintained as a precautionary measure or for some other specific purpose.

Why does a manufacturing company require three different inventory categories?

Manufacturers separate their inventories into categories because of how costs are calculated. Raw materials are generally listed at cost; a company that pays $600 a ton for steel and has 5 tons of steel on hand would report $3,000 in raw materials inventory on the balance sheet.

What are the types of inventory in the manufacturing company?

There are four main types of inventory: raw materials/components, WIP, finished goods and MRO.

What are the three types of inventory in manufacturing firm?

Manufacturers deal with three types of inventory. They are raw materials (which are waiting to be worked on), work-in-progress (which are being worked on), and finished goods (which are ready for shipping).

What are the two most common inventory flow assumptions?

FIFO and LIFO are the two most common cost flow assumptions made in costing inventories. The amounts assigned to the same inventory items on hand may be different under each cost flow assumption.

What are the three inventories in a manufacturing concern?

What are the three inventory cost flow assumptions?

In the U.S. the cost flow assumptions include FIFO, LIFO, and average. (If specific identification is used, there is no need to make an assumption.) FIFO, LIFO, average are assumptions because the flow of costs out of inventory does not have to match the way the items were physically removed from inventory.

What is meant by inventory cost flow?

The inventory cost flow assumption states that the cost of an inventory item changes from when it is acquired or built and when it is sold. Because of this cost differential, management needs a formal system for assigning costs to inventory as they transition to sellable goods.

What is the major cause of inventory shrinkage?

Retail inventory shrinkage is the difference between a product’s recorded stock count and the amount physically on hand. Lost stock stems from theft or inventory control issues like receiving errors, unrecorded damages, cashier mistakes, and misplaced items can all cause inventory shrink.

Why are the three types of production manufacturing inventory kept separate from each other in accounting?

What are the three inventory accounts used to record manufacturing cost?

To record product costs as an asset, accountants use one of three inventory accounts: raw materials inventory, work-in-process inventory, or finished goods inventory.

What is the inventory account used to record?

The work-in-process inventory account is used to record the cost of products that are in production but that are not yet complete. The finished goods inventory account is used to record the costs of products that are complete and ready to sell.

What is raw materials inventory?

Raw materials inventory is the total cost of all component parts currently in stock that have not yet been used in work-in-process or finished goods production. These are materials not incorporated into the final product, but which are consumed during the production process.

What are the different types of inventory accounts?

The three inventory accounts described above are common among manufacturing companies; however, a fourth inventory account known as manufacturing or factory supplies account is some time maintained by manufacturing companies.

How are inventory accounts reported on a balance sheet?

The above three types of inventory are reported in the balance sheet of manufacturing company as follows: The three inventory accounts described above are common among manufacturing companies; however, a fourth inventory account known as manufacturing or factory supplies account is some time maintained by manufacturing companies.

What kind of inventory does a manufacturing company have?

Manufacturing companies produce goods and sell them to customers or merchandising companies. Manufacturing companies normally maintain three inventory accounts. These are: raw materials inventory, work in process inventory and finished goods inventory. These are briefly explained below:

Why do merchandising companies report only one inventory account?

Merchandising and manufacturing companies maintain and report inventories differently. Merchandising companies buy goods that are ready to use and sell them to customers at a profit. Because merchandising companies do not produce anything, the financial statements of these companies show only one inventory account that is “Merchandise Inventory”.