How to calculate the overhead variance?

John Peck

John Peck

To obtain the fixed overhead volume variance, calculate the actual amount as (actual volume)(assigned overhead cost) and then subtract the budgeted amount, calculated as (budgeted volume)(assigned overhead cost).

How to calculate variable overhead cost variance?

VOH expenditure variance is the difference between the standard variable overheads for the actual hours worked, and the actual variable overheads incurred. The formula is as follows: VOH Exp. Variance = AVOH – SVOH for actual hours worked.

What is overhead variances?

Overhead variance refers to the difference between actual overhead and applied overhead. You can only compute overhead variance after you know the actual overhead costs for the period. The difference between the actual overhead costs and the applied overhead costs are called the overhead variance.

How to calculate standard overhead?

The standard overhead rate is calculated by dividing budgeted overhead at a given level of production (known as normal capacity) by the level of activity required for that particular level of production.

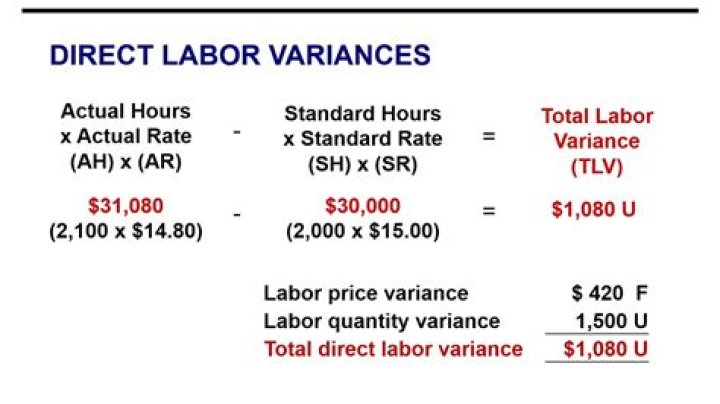

How do you calculate labor rate variance?

The labor rate variance is found by computing the difference between actual hours multiplied by the actual rate and the actual hours multiplied by the standard rate.

What is the formula of Labour mix variance?

Can be computed using the formula: Labour Cost Variance = (SH x SR) – (AH x AR) where, AH = Actual hours AR = Actual Rate SH = Standard hours for actual output SR = Standard RateStandard time for actual output =When the actual labour cost is more than standard cost, there will be adverse variance. 27.

How do you calculate standard variable overhead cost?

Using the flexible budget, we can determine the standard variable cost per unit at each level of production by taking the total expected variable overhead divided by the level of activity, which can still be direct labor hours or machine hours.

How do you calculate labor cost in standard time?

You calculate the standard price by multiplying the direct labor hourly price by the standard job completion time. For example, one employee can produce 10 completed units in two hours. The direct labor hourly cost is $9 per hour and the standard direct labor time is two hours.

What is idle time example?

Idle time is that time for which the employer pays, but from which he obtains no production. For example, if out of eight hours that a worker is supposed to put in the factory, the worker’s job card shows only seven hours spent on jobs, one hour will be the idle time in such a case.