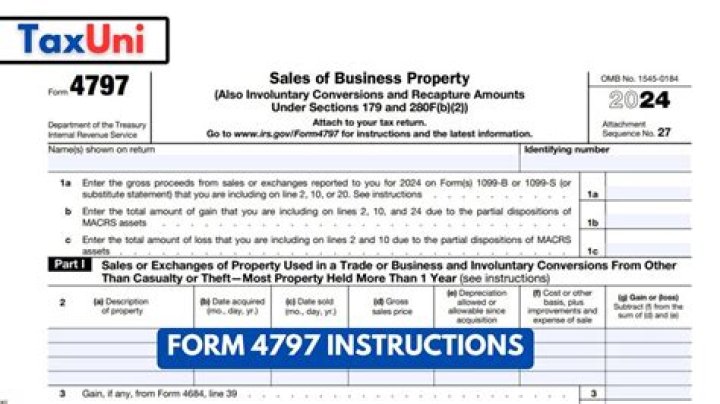

How to fill out Tax Form 4797 after sale of a property?

David Craig

David Craig

If by line 20, you mean the 4797, I put only the building, because that’s the Sec. 1250 property. I separated the sales price into land and building based on the purchases, and got $185,610 on line 20, and then on line 21 goes the sales price minus whatever you depreciated it at.

What makes up Part I of Form 4797?

Part I – most property held more than 1 year. Long-term assets sold at a loss . Nondepreciable long-term assets sold at a gain. Income from Part III, line 32. Nonrecapture net §1231 losses from prior years. 6

How to redetermine a loss on Form 4797?

Identify as from “Form 4797, line 18a.” See instructions.. b Redetermine the gain or (loss) on line 17 excluding the loss, if any, on line 18a. Enter here and on Form 1040, line 14

Where to report gains on sale of depreciable property?

Generally, the gain is reported on Form 8949 and Schedule D. However, part of the gain on the sale or exchange of the depreciable property may have to be recaptured as ordinary income on Form 4797. Use Part III of Form 4797 to figure the amount of ordinary income recapture. The recapture amount is included on line 31 (and line 13) of Form 4797.

Do you have to file tax return when you sell rental property?

The task of filing a tax return when you own or sell rental real estate can be tricky without expert knowledge and experience. The IRS views rental properties in a similar way to business real estate, and as such, it’s not possible to add gains and losses incurred through the sale of your property to your 1040 form.

How to report the sale of rental property?

Report the gain or loss on the sale of rental property on Form 4797, Sales of Business Property or on Form 8949, Sales and Other Dispositions of Capital Assets depending on the purpose of the rental activity. Individuals typically use Schedule D (Form 1040), Capital Gains and Losses together with Form 4797 or Form 8949.

How is rental income reported on an income tax return?

Rental Income and Expenses. Any rent payments you receive when you rent out your property are subject to income tax and must be declared in your income tax return. Rental income refers to the full amount of rent and related payments you receive when you rent out your property.

What do I need to report on Form 4797?

The types of property that often show up on form 4797 include things like property used for generating rental income, as well as property that’s employed as part of industrial or agricultural enterprises. If you sell a home that you were renting out full-time, for instance, you will likely need to report any gains or losses on form 4797.

How is disposition of property reported on Form 4797?

The disposition of each type of property is reported separately in the appropriate part of Form 4797 (for example, for property held more than 1 year, report the sale of a building in Part III and land in Part I).

Where does the sale of a house go on the 4797?

Make sure you allocate the selling fees, unless you have them already broken out. The sale of the house goes in Part III of the 4797 as a Sec. 1250 Property. The sale of the land goes on Part I of the 4797.

Is the sale of land reported on 4797?

The sale of the land goes on Part I of the 4797. It gets combined on line 13 of your Form 1040 as a capital asset. So the answer to your last question is this does count as two sales on your 4797, but one as a Schedule D capital asset.

Where do I find the instructions for Form 4797?

Section references are to the Internal Revenue Code unless otherwise noted. For the latest information about developments related to Form 4797 and its instructions, such as legislation enacted after they were published, go to Use Form 4797 to report the following.

How to calculate gain or loss on Form 4797?

In order to determine how much of a gain or loss you might need to report on IRS form 4797, you’ll to do a bit of math. First off, you’ll have to calculate the so-called “amount realized” for the sale of the asset.

How to take the mystery out of Form 4797?

Form 4797 Part I – most property held more than 1 year Long-term assets sold at a loss Nondepreciable long-term assets sold at a gain Income from Part III, line 32 Nonrecapture net §1231 losses from prior years 6 Form 4797 Part II – ordinary gains and losses Assets held less than 1 year All ordinary gains or losses Income from Part III, line 31 7

Where to find recapture amount on Form 4797?

Use Part III of Form 4797 to figure the amount of ordinary income recapture. The recapture amount is included on line 31 (and line 13) of Form 4797. See the Instructions for Form 4797, Part III. If the total gain for the depreciable property is more than the recapture amount, the excess is reported on Form 8949.

What do you need to report on Form 4797?

Use Form 4797 to report: •The sale or exchange of: 1. Real property used in your trade or business; 2. Depreciable and amortizable tangible property used in your trade or business (however, see Disposition of Depreciable Property Not Used in Trade or Business, later); 3. Oil, gas, geothermal, or other mineral properties; and 4.

What kind of loss is reported on form 8949?

Generally, loss from the sale or exchange of depreciable property not used in a trade or business but held for investment or for use in a not-for-profit activity is a capital loss. Report the loss on Form 8949 in Part I (if the transaction is short term) or Part II (if the transaction is long term).