In which accounting method are expenses and revenues not matched in time?

David Craig

David Craig

Accrual accounting is an accounting method where revenue or expenses are recorded when a transaction occurs rather than when payment is received or made.

When should revenue and expense be recognized in the accrual basis?

Under the accrual basis of accounting, revenues and expenses are recorded as soon as transactions occur. This process runs counter to the cash basis of accounting, where transactions are reported only when cash actually changes hands.

How many methods are recognize for accounting?

There are two methods of accounting: cash-based and accrual-based.

How are expenses and revenues related in accounting?

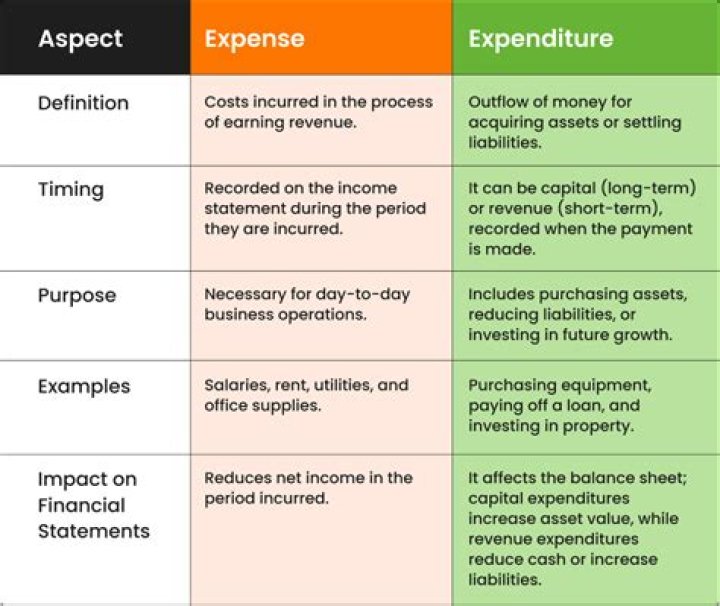

Expenses are matched with revenues or with the period of time shown in the heading of the income statement, not in the period when the expenses were paid. This reflects the basic accounting principle known as the matching principle. The financial statements also reflect the basic accounting principle known as the cost principle.

When does the cash method of accounting recognize revenue?

The cash method of accounting recognizes revenue and expenses when cash is exchanged. For a seller using the cash method, if cash is received prior to the delivery of goods, the cash is recorded as earnings.

How are income and Expenses reported in cash method?

Under the cash method, income and expenses are reported and deducted in the tax year they are received and paid, respectively. On the other hand, under the accrual method, both income and expenses are generally reported in the tax year when they are realized, regardless of when they are received.

When do you not need to accrue revenues and expenses?

If companies received cash payments for all revenues at the same time when they were earned, and made cash payments for all expenses at the time when they were incurred, there wouldn’t be a need for accruals.