Is a new delivery truck eligible for bonus depreciation?

Emily Baldwin

Emily Baldwin

New and used vehicles can qualify, but the law requires that the vehicle be new to you and your business. 100% first-year bonus depreciation is only available when an SUV, pickup, or van has a manufacturer’s gross vehicle weight rating (GVWR) above 6,000 pounds.

Is there a phase out for bonus depreciation?

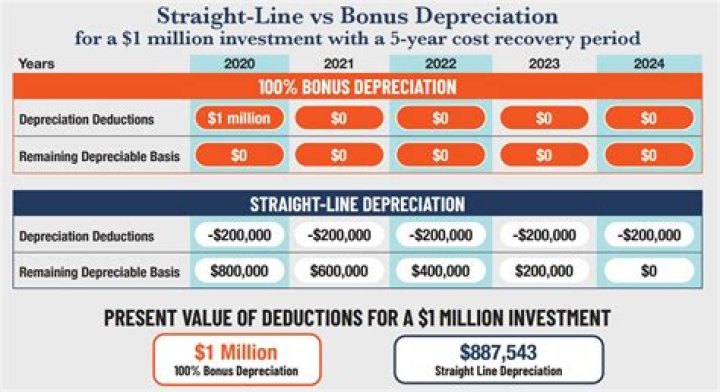

Under current law, 100% bonus depreciation will be phased out in steps for property placed in service in calendar years 2023 through 2027. Thus, an 80% rate will apply to property placed in service in 2023, 60% in 2024, 40% in 2025, and 20% in 2026, and a 0% rate will apply in 2027 and later years.

When did the bonus depreciation change for business?

It allows your business to take an immediate first-year deduction on the purchase of eligible business property, in addition to other depreciation. In December 2017, Congress passed the Tax Cuts and Jobs Act (the Trump Tax Cuts), that included some changes to bonus depreciation, among other changes to business taxes.

How much bonus depreciation can I claim on a vehicle?

For example, vehicles with a gross vehicle weight (GVW) rating of 6,000 pounds or less are limited to $8,000 of bonus depreciation in the first year they’re placed in service. On the other hand, heavy vehicles with a GVW rating above 6,000 pounds that are used more than 50% for business can deduct 100% of the cost.

When do you get bonus depreciation from TCJA?

In December 2017, Congress passed the Tax Cuts and Jobs Act (TCJA) that included some changes to increase the possibility that you can take bonus depreciation. Here are the details of the new provisions: Bonus depreciation doesn’t have to be used for new purchases but must be “first use” by the business that buys it.

What makes a computer eligible for bonus depreciation?

Listed property consists of automobiles and certain other personal property. Computers were listed property under prior law but starting in tax year 2018, they are no longer classified as listed property so there is no over 50% use requirement. Bonus depreciation differs in some important ways from Section 179: