Is CAPM cost of equity?

Sophia Bowman

Sophia Bowman

CAPM is a formula used to calculate the cost of equity—the rate of return a company pays to equity investors. For companies that pay dividends, the dividend capitalization model can be used to calculate the cost of equity.

How do you calculate the cost of equity using the CAPM approach?

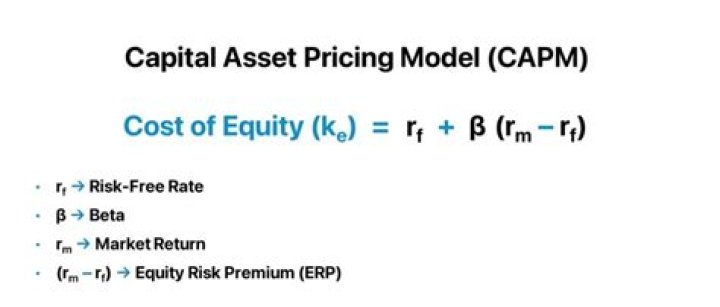

We need to calculate the cost of equity using the CAPM model.

- Company M has a beta of 1, which means the stock of Company M will increase or decrease as per the tandem of the market.

- Ke = Risk-Free Rate of Return + Beta * (Market Rate of Return – Risk-free Rate of Return)

- Ke = 0.04 + 1 * (0.06 – 0.04) = 0.06 = 6%.

How is CAPM calculated?

The CAPM formula (ERm – Rf) = The market risk premium, which is calculated by subtracting the risk-free rate from the expected return of the investment account. The benefits of CAPM include the following: Ease of use and understanding. Accounts for systematic risk.

Why does CAPM calculate cost of equity?

CAPM provides a formulaic method to model the cost of equity, or risk-return relationship of an investment. It helps users calculate the cost of equity for risky individual securities or portfolios. Investors need compensation for risk and time value when investing money.

What does the CAPM tell us?

The Capital Asset Pricing Model (CAPM) describes the relationship between systematic risk and expected return for assets, particularly stocks. CAPM is widely used throughout finance for pricing risky securities and generating expected returns for assets given the risk of those assets and cost of capital.

What are the strengths of CAPM?

Advantages of CAPM

- i) Eliminates Unsystematic Risk.

- ii) Systematic Risk.

- iii) Investment Appraisal.

- iv) Ease of Use.

- i) Too Many Assumptions.

- ii) Assigning Values to CAPM Variables.

- iii) Ability to Borrow at Risk-free Rate.

- iv) Determination of Project Proxy Beta.

How do you know if a stock is undervalued using CAPM?

If a security’s expected return versus its beta is plotted above the security market line, it is considered undervalued, given the risk-return tradeoff.