Is it better to borrow from a bank or lender?

Isabella Wilson

Isabella Wilson

While each provides money, a smart real estate investor should know the differences the two. Banks are traditionally less expensive, but they are harder to work with and more difficult to get a loan approved with. Private lenders tend to be more flexible and responsive, but they are also more expensive.

What are the advantages of getting a bank loan?

Advantages of term loans While you must pay interest on your loan, you do not have to give the lender a percentage of your profits or a share in your company. Interest rates may be fixed for the term so you will know the level of repayments throughout the life of the loan.

Why do people prefer bank loans?

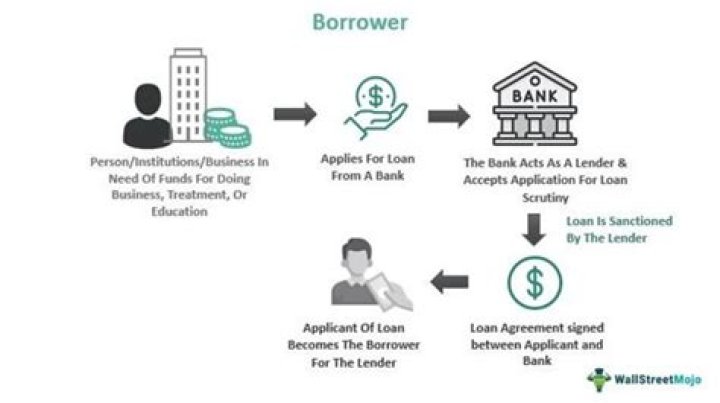

We borrow money because we want to buy something. It may be as large as a property or a car, or something smaller like furniture or a computer. We may borrow money to spend it on experiences. It may be something as large as a loan to travel the world, to something smaller, like using a credit card for a meal out.

Is it better to get a loan from a bank?

Why do bank loans offer lower rates? Banks typically have a lower cost of funds than other lenders. Depositors (their retail customers) keep a lot of money in their checking and savings accounts. Thus, banks have easy access to those funds to lend out.

How can I borrow money for a down payment?

Before you decide on borrowing money for your down payment, it’s important to weigh the pros and cons of each option.

- Take out a HELOC or home equity loan for a down payment.

- Get a loan from a friend or family member.

- Tap your retirement savings.

- Get a bridge loan.

- Explore down payment assistance programs.

What is the advantage of a down payment to the lender?

A larger down payment generally means you’re a less risky borrower, and a less risky borrower means a lower interest rate. A lower interest rate will help you save on your monthly payment and allow you to pay less interest over the life of the loan.

What are the disadvantages of borrowing money from a bank?

Disadvantage: You Risk Foreclosure if You Can’t Repay The Loan. A bank won’t take ownership of your business when you first take out a loan. However, depending on how the contract is drawn up, you risk the bank foreclosing on your business in the event that you are unable to repay the loan.

What are the pros and cons of bank loans?

Business owners should weigh the advantages and disadvantages of bank loans against other means of finance.

- Advantage: Keep Control of the Company.

- Advantage: Bank Loan is Temporary.

- Advantage: Interest is Tax Deductible.

- Disadvantage: Tough to Qualify.

- Disadvantage: High Interest Rates.

What is a good excuse to get a loan?

9 reasons to get a personal loan

- Debt consolidation. Debt consolidation is one of the most common reasons for taking out a personal loan.

- Alternative to payday loan.

- Home remodeling.

- Moving costs.

- Emergency expenses.

- Appliance purchases.

- Vehicle financing.

- Wedding expenses.

What’s the best reason to give for a loan?

One of the best reasons to get a personal loan is to consolidate other existing debts. Let’s say you have a few existing debts to your name—student loans, credit card debt, etc. —and are having trouble making payments. A debt consolidation loan is a type of personal loan that can yield two core benefits.

Is it downpayment or down payment?

Down payment (also called a deposit in British English), is an initial up-front partial payment for the purchase of expensive items/services such as a car or a house. It is usually paid in cash or equivalent at the time of finalizing the transaction.

Can you pay off a loan with the same loan?

While you can often use one loan to pay off another, be sure to read the fine print of your contract first and be wise about your spending habits. For example, “a bank may require the money be used to pay off existing debts, and even facilitate the payments to other lenders,” he said.

Why do most borrowers only pay attention to the monthly payment?

I think most borrowers only pay attention to the monthly payments when taking out a loan because the advantage lies in obtaining income in the form of the interest and finance charges on the loan. In order to increase their investment, lenders often charge other fees when the borrower gets the loan.

Why does the size of your down payment on a loan matter?

The smaller your down payment, the higher your LTV ratio is and the riskier your loan appears in the eyes of lenders. Lenders tend to compensate for making riskier loans by charging higher interest rates, so you might be able to qualify for a better rate if you lower your LTV ratio by putting more money down.

What is the biggest disadvantage of borrowing money from a family member?

What is the biggest disadvantage of borrowing money from a family member? It documents exactly how much cash is available. A business consistently underperformed, failing to generate enough cash to pay its operating expenses.

What is the best reason to give when applying for a personal loan?

Reasons for taking out a personal loan If you lose your job, get your work hours reduced or have an emergency medical bill, a personal loan can meet your needs in the short term. Debt consolidation: You can save money on interest payments when you consolidate high-interest credit card debt with a personal loan.

What do banks look at when applying for a personal loan?

Every lender you apply to will check your credit report and scores. Lenders will usually consider your credit scores when reviewing your application, and a higher score generally qualifies you for better interest rates and loan terms on any loans you seek.

What’s the best purpose of loan?

Most lenders will let you apply for a loan provided it’s for a worthwhile purpose. This includes paying for a wedding, a car, a holiday, home improvements or to consolidate your debt. While there is no “best” reason to put on your loan application, there are a number of things that you’ll be unable to get a loan for.