Is it better to pay principal or interest on car loan?

Isabella Wilson

Isabella Wilson

As a general rule, making extra payments just toward the principal balance can help you pay off a loan faster and reduce the overall cost of the loan. But you’ll want to make sure your lender accepts principal-only payments and won’t penalize you for making them or paying off your loan early.

Can you pay extra principal on a car loan?

Paying off a car loan early can be beneficial. Once you’ve confirmed with your lender that they’ll apply amounts in excess of your regular monthly payment to the principal of the loan, you can either make larger-than-usual payments or send extra money when your budget allows.

Is it better to pay off a car loan early?

Paying off your car loan early frees up a good chunk of extra cash to keep in your pocket. If your car loan’s rate is low compared to other types of debt, like credit cards, consider paying off the debt with the highest interest rate first. That way you save more on total interest owed.

What happens if I pay extra on my car loan?

As long as your loan doesn’t have precomputed interest, paying extra can help reduce the total amount of interest you’ll pay. You’ll pay off your loan faster.

How much principal do you pay off in 5 years?

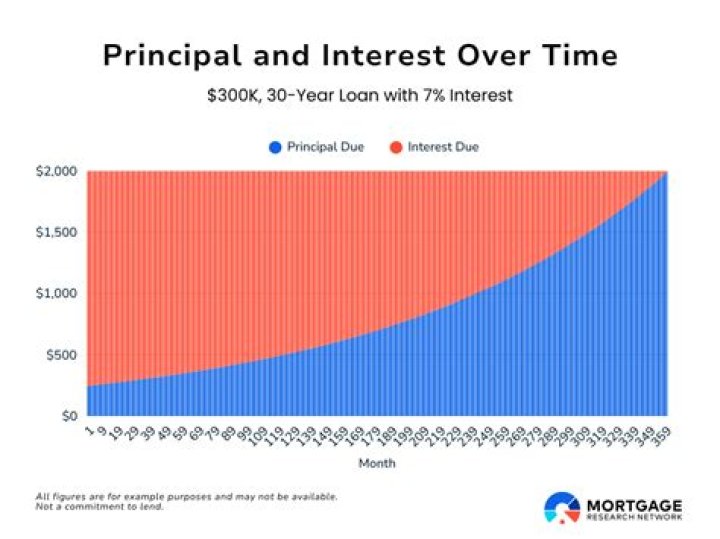

15-Year Mortgages While your first payment is larger than with a 30-year loan, you also pay off $1,332 in just one month. After five years, your principal payment goes up to $1535 and keeps climbing. For the last five years of your loan, you will pay at least $1,784 per month in principal, increasing every month.

What happens if I pay an extra $200 a month on my mortgage?

If you’re able to make $200 in extra principal payments each month, you could shorten your mortgage term by eight years and save over $43,000 in interest.

What happens if I make a lump sum payment on my car loan?

Making a lump-sum payment reduces the amount owed on your auto loan. Say you borrowed a $20,000 loan with a five-year term and a 4.55% APR (interest rate plus fees), so you’re paying $373 a month. You’ve just received a work bonus, so you can put $1,000 or $3,000 toward your loan as a lump sum.

How much does your credit score go up when you pay a car off?

In short, while the general result of a paid-off car loan is a small drop in credit score, there’s no one-size-fits-all rule, and you won’t know the exact impact of paying off your car loan until it’s already done.

What is a good monthly car payment?

Many financial experts recommend keeping total car costs below 15% to 20% of your take-home pay. For example, if your monthly paycheck is $3,000, your car payment would be about $300 and you’d plan on spending another $150 on automotive expenses.

How can I negotiate a lower car payment?

How To Negotiate a Low Rate on Your Car Loan

- Make sure your credit is in good standing.

- Shop around at local banks and credit unions.

- Compare rates at national lenders.

- Negotiate with the lender who has the lowest rate.

- Negotiate with the Dealer.

What happens if you make 1 extra mortgage payment a year?

3. Make one extra mortgage payment each year. Making an extra mortgage payment each year could reduce the term of your loan significantly. For example, by paying $975 each month on a $900 mortgage payment, you’ll have paid the equivalent of an extra payment by the end of the year.

What happens if I pay an extra $1000 a month on my mortgage?

Paying an extra $1,000 per month would save a homeowner a staggering $320,000 in interest and nearly cut the mortgage term in half. To be more precise, it’d shave nearly 12 and a half years off the loan term. The result is a home that is free and clear much faster, and tremendous savings that can rarely be beat.

Should I make a lump sum payment on my car loan?

Making a lump-sum payment reduces the amount owed on your auto loan. Say you borrowed a $20,000 loan with a five-year term and a 4.55% APR (interest rate plus fees), so you’re paying $373 a month. This chart can give you a better sense of how long it’ll take to pay off a car loan with extra payments.

Is paying off a car good for credit?

A high interest rate loan means you’re paying more each month on your initial loan amount. If you have the cash to pay off your car loan, without neglecting other debts, then paying off your car loan is a great idea. A car loan helps to improve your credit mix, which contributes to a better credit score.

What car can I afford with 50k salary?

Dave Ramsey takes a balance sheet approach. Rather than looking at monthly transportation costs, Dave recommends buying cars that cost no more than 50% of your annual income. So if you make $50,000 a year, you should not spend more than $25,000 for a car(s).

Is 500 a month too much for a car payment?

A $500 car payment is about average right now. The concept of “too much” is going to depend on your income and living expenses, your insurance expense, and other budget factors.

As we’ve mentioned, if you have a simple-interest loan, you can pay it off more quickly by making additional payments toward the principal. Because you’ll pay off the principal faster, you’ll pay less interest and reduce the overall cost of the loan.

Are principal-only payments better?

A principal-only payment can accelerate your debt pay off and save you money in interest. If you can make an extra principal-only payment on your credit card each month, your interest will accrue much slower, helping you get rid of your credit card debt that much faster.

Does paying principal lower monthly?

Putting extra cash towards your mortgage doesn’t change your payment unless you ask the lender to recast your mortgage. Unless you recast your mortgage, the extra principal payment will reduce your interest expense over the life of the loan, but it won’t put extra cash in your pocket every month.

What happens if I pay principal-only?

The principal is the amount you borrowed. The interest is what you pay to borrow that money. But if you designate an additional payment toward the loan as a principal-only payment, that money goes directly toward your principal — assuming the lender accepts principal-only payments.

Should you pay interest or principal first?

Loan principal is the amount of debt you owe, while interest is what the lender charges you to borrow the money. Interest is usually a percentage of the loan’s principal balance. When you make loan payments, you’re making interest payments first; the the remainder goes toward the principal.

What happens if I pay principal only?

What does it mean to pay principal only?

The principal is the amount you borrowed. The interest is what you pay to borrow that money. If you make an extra payment, it may go toward any fees and interest first. The rest of your payment will then go toward your principal.

What’s the difference between interest and principal on a loan?

Normally, when you make a payment on a loan, the lender applies part of your payment to interest and fees before it reduces the principal. Let’s say your monthly payment amount on a $5,000 loan at 6% APR is $96.66. Your interest payment is $13.33.

Is it better to make principal only payments on a home loan?

Making principal-only payments can benefit you in a couple ways. By putting more money toward the principal, you can usually pay off the balance more quickly and reduce the overall length of the loan. Making principal-only payments can lower the total interest paid on the loan.

What’s the difference between a principal payment and an extra payment?

On the first payment of $500, the balance is $9500. After interest, it’s ~$9579. If you make a second payment in the first month, after interest the balance is ~$9075. What is the advantage to mark the extra payment as “principal only” payment then?