Is there a tax benefit to contributing to an IRA?

John Peck

John Peck

For 2020 and 2021, there’s a $6,000 limit on taxable contributions to retirement plans. Those aged 50 or over can contribute another $1,000. In the eyes of the IRS, your contribution to a traditional IRA reduces your taxable income by that amount and, thus, reduces the amount you owe in taxes.

Which IRA contributions are not tax-deductible?

If you have a 401(k) at work and your salary surpasses $76,000, or $125,000 for couples if both spouses have a 401(k), you may not be able to deduct your contributions to a traditional IRA. Those who don’t qualify for a traditional IRA or Roth IRA may choose to make nondeductible IRA contributions.

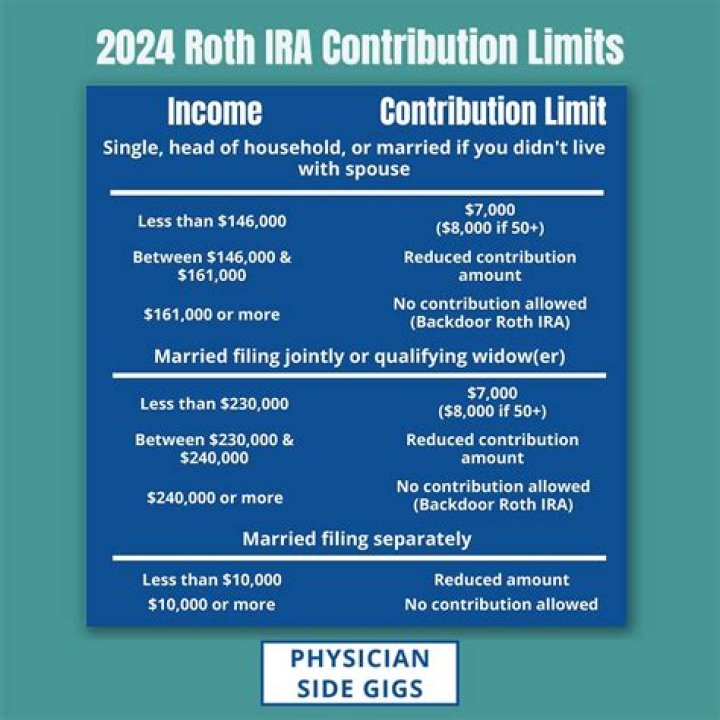

Are there income limits on contributions to both IRAs?

Your total contributions to both your IRA and your spouse’s IRA may not exceed your joint taxable income or the annual contribution limit on IRAs times two, whichever is less. It doesn’t matter which spouse earned the income. Roth IRAs and IRA deductions have other income limits.

What do you need to know about IRA contributions?

IRA FAQs 1 Contributions. How much can I contribute to an IRA? 2 Distributions (Withdrawals) 3 Distributions while still working. 4 Required minimum distributions. 5 Qualified charitable distributions. 6 Rollovers and Roth Conversions. 7 Recharacterization of IRA Contributions. 8 Investments. …

How much tax do you pay on a Roth IRA?

For example, if 20% of your current IRA balance consists of nondeductible contributions and the remainder is deductible contributions and earnings, you will owe income tax on 80 cents of each dollar you convert to Roth IRA status.

How to figure out the tax owed on an early withdrawal from a Roth IRA?

Question: How do I figure out the tax owed on an early withdrawal from a Roth IRA? Answer: Good question. If you do a conversion, your Roth IRA can include money from (1) your annual after-tax contributions (2) contributions from one or more converted regular IRAs, and (3) earnings on both types of contributions.