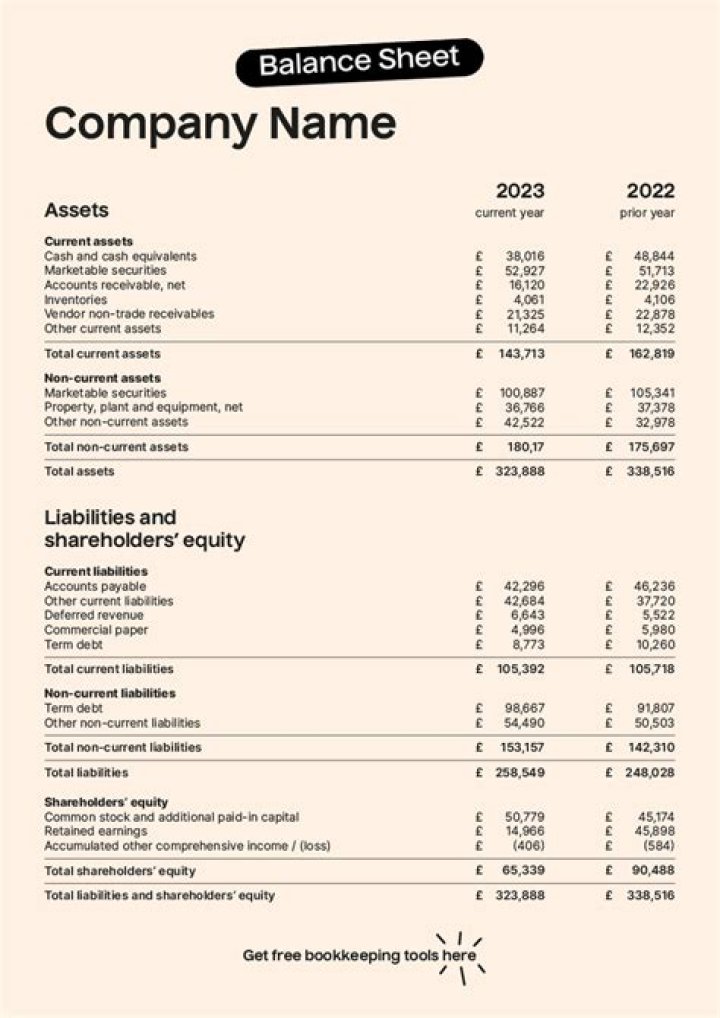

What accounts do not appear on a balance sheet?

Joseph Russell

Joseph Russell

Off-balance sheet (OBS) assets are assets that don’t appear on the balance sheet. OBS assets can be used to shelter financial statements from asset ownership and related debt. Common OBS assets include accounts receivable, leaseback agreements, and operating leases.

How do accountants use financial statements?

Financial statements are written records that convey the business activities and the financial performance of a company. Financial statements are often audited by government agencies, accountants, firms, etc. to ensure accuracy and for tax, financing, or investing purposes. Financial statements include: Balance sheet.

Which account does appear on the balance sheet?

Examples of a corporation’s balance sheet accounts include Cash, Temporary Investments, Accounts Receivable, Allowance for Doubtful Accounts, Inventory, Investments, Land, Buildings, Equipment, Furniture and Fixtures, Accumulated Depreciation, Notes Payable, Accounts Payable, Payroll Taxes Payable, Paid-in Capital.

Are derivatives off balance sheet?

Off-balance-sheet items are contingent assets or liabilities such as unused commitments, letters of credit, and derivatives. These items may expose institutions to credit risk, liquidity risk, or counterparty risk, which is not reflected on the sector’s balance sheet reported on table L.

Is depreciation expense on the balance sheet?

Depreciation expense is not a current asset; it is reported on the income statement along with other normal business expenses. Accumulated depreciation is listed on the balance sheet.

What are some examples of off-balance-sheet items?

Off-balance sheet activities include items such as loan commitments, letters of credit, and revolving underwriting facilities. Institutions are required to report off-balance sheet items in conformance with Call Report Instructions.

How are derivatives shown on balance sheet?

Derivative financial instruments are stated at their market value in the balance sheet and are classified as current assets or liabilities, unless they form part of a hedging relationship, where their classification follows the classification of the hedged financial asset or liability.