What are accounting changes?

Isabella Wilson

Isabella Wilson

An accounting change is a change in accounting principles, accounting estimates, or the reporting entity. A change in accounting principles is a change in a method used, such as using a different depreciation method or switching between LIFO to FIFO inventory valuation methods.

What are accounting policies examples?

Example of an Accounting Policy Accounting policies can be used to legally manipulate earnings. For example, companies are allowed to value inventory using the average cost, first in first out (FIFO), or last in first out (LIFO) methods of accounting.

Why do companies change accounting methods?

The major reasons why companies change accounting methods are: (1) Desire to show better profit picture. (2) Desire to increase cash flows through reduction in income taxes. (3) Requirement by Financial Accounting Standards Board to change accounting methods. (5) Desire to show a better measure of the company’s income.

What are some examples of change in accounting principle?

Accounting principles impact the methods used, whereas an estimate refers to a specific recalculation. An example of a change in accounting principles occurs when a company changes its system of inventory valuation, perhaps moving from LIFO to FIFO.

What is an example of accounting policy?

Example of an Accounting Policy For example, companies are allowed to value inventory using the average cost, first in first out (FIFO), or last in first out (LIFO) methods of accounting. If it uses LIFO, its cost of goods sold is: (10 x $12) + (5 x $10) = $170.

What are changes in accounting principles?

A change in accounting principle is the term used when a business selects between different generally accepted accounting principles or changes the method with which a principle is applied. Accounting principles impact the methods used, whereas an estimate refers to a specific recalculation.

How do you report change in accounting method?

You can request approval for a change in accounting methods in one of two ways. File Form 3115 in duplicate for an automatic change request. Attach the original Form 3115 to your federal income tax return for the year of the change, including extensions.

What is considered a change in accounting policy?

A change in accounting estimate is an adjustment of the carrying amount of an asset or liability, or related expense, resulting from reassessing the expected future benefits and obligations associated with that asset or liability.

What are the three accounting changes?

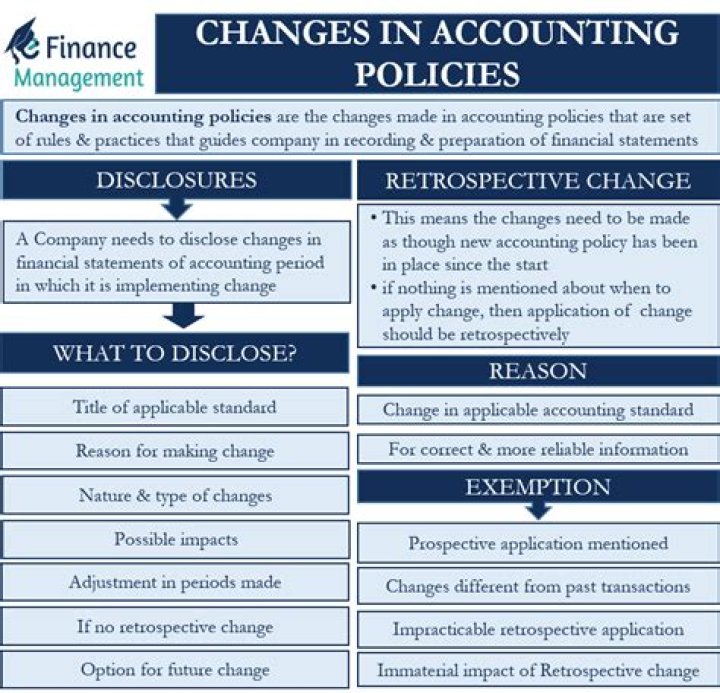

Changes in accounting are of three types. They are changes in accounting principle, changes in accounting estimates, and changes in reporting entity. Accounting errors result in accounting changes too.

When do you need to change the accounting principle?

This is needed so that the users of the statements can ascertain the extent to which an accounting change triggered a variation in the financial statements. A change in accounting principle is a change from one generally accepted accounting principle to another generally accepted accounting principle.

What is the definition of an accounting change?

An accounting change is a change in accounting principle, accounting estimate, or the reporting entity. These changes can trigger modifications in the reported profits or other financial aspects of a business. They are covered in more detail below. An accounting change may require discussion in the notes accompanying the financial statements.

What does retrospective application of change in accounting principle mean?

Change in accounting principle. Retrospective application means that you are applying the change in principle to the financial results of previous periods, as if the new principle had always been in use.

Which is an indirect effect of a change in accounting principle?

An indirect effect of a change in accounting principle is a change in an entity’s current or future cash flows from a change in accounting principles that is being applied retrospectively.