What are adjustments needed at the end of an accounting period?

Emma Jordan

Emma Jordan

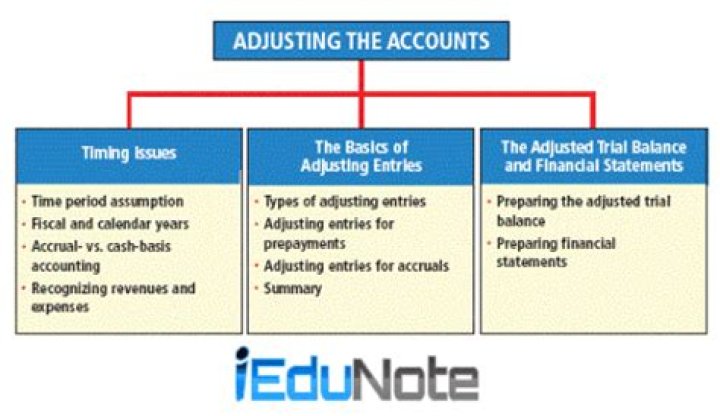

Adjusting entries are necessary at the end of an accounting period to bring the ledger up to date. Four different categories of adjusting entries include prepaid expenses (deferred expenses), unearned revenues (deferred revenues), accrued expenses (accrued liabilities), and accrued revenues (accrued assets).

What is a year-end adjusting entry?

Year-end adjustments are journal entries made to various general ledger accounts at the end of the fiscal year, to create a set of books that is in compliance with the applicable accounting framework. The number of these adjustments that are needed has a direct impact on the time required to close the books.

Does accrual accounting require end of the period adjustments?

Under accrual accounting, the company must make adjustments for accrued and prepaid items, those that have been earned or incurred in the year but not yet recorded, or those that have been paid in advance for multiple years.

How do you record accrued adjusting entries?

The accountant would make an adjusting journal entry in which the amount of cash received by the customer would be debited to the cash account on the balance sheet, and the same amount of cash received would be credited to the accrued revenue account or accounts receivable account, reducing that account.

Do companies need to make adjusting entries at the end of every month?

Understanding Adjusting Journal Entries The construction company will need to do an adjusting journal entry at the end of each of the months to recognize revenue for 1/6 of the amount that will be invoiced at the six-month point.

When do you adjust entries in an accounting cycle?

Adjusting entries. Posted in: Accounting cycle (explanations) Adjusting entries (also known as end of period adjustments) are journal entries that are made at the end of an accounting period to adjust the accounts to accurately reflect the revenue and expenses of the current period.

When do journal entries need to be adjusted?

What are Adjusting Entries? Adjusting entries are journal entries that are made in the accounting journals at the end of an accounting period after the preparation of the trial balance.

When do you need to make an adjusting entry?

Adjusting entries are made at the end of an accounting period to properly account for income and expenses not yet recorded in your general ledger, and should be completed prior to closing the accounting period. Overview: What are adjusting entries? Adjusting entries are Step 5 in the accounting cycle and an important part of accrual accounting.

What’s the difference between adjusting entries and reversing entries?

Adjusting Entries and Reversing Entries. Reversing entries are the entries post at the beginning of the accounting period which aims to eliminate the accrue adjusting entries which we made at the end of the accounting period. Without reversing entries, the accountant is highly likely to make a double posting for the same transaction.