What are the 6 principles of the AICPA Code of Professional Conduct?

Isabella Wilson

Isabella Wilson

The AICPA Code of Conduct is based on six principles; (1) responsibilities (2) serve the public interest (3) integrity (4) objectivity and independence (5) due care and (6) scope and nature of services. These principles are required practices for all certified public accountants who are members of the AICPA.

What are the principles of professional conduct?

Principles of Professional Ethics

- Adhere to the highest standards of professional conduct.

- Strive for impartiality and objectivity when dealing with others.

- Communicate openly and honestly with colleagues and clientele.

- Maintain confidentiality in professional relationships.

How many principles are there in the aicpa code of ethics?

Six

It Consists of Six Main Principles Outside of the six main principles we’ll cover below, the AICPA Code of Conduct notes that these are the basic principles of professional conduct.

What are the four parts of the AICPA Code of Professional Conduct?

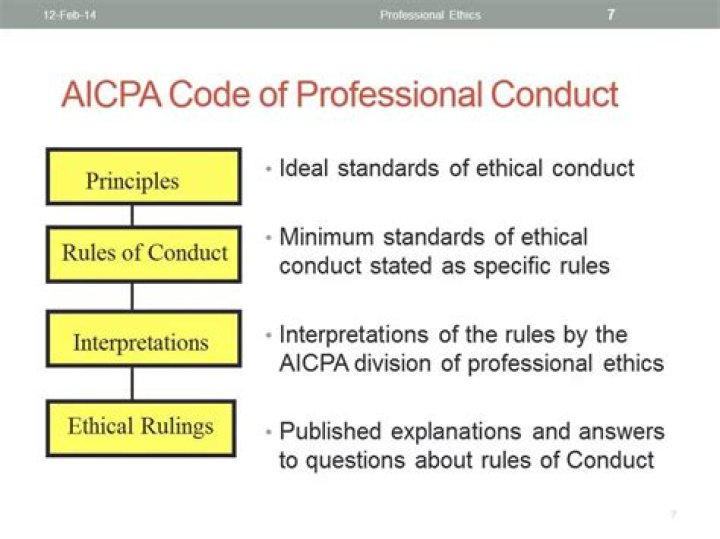

The four parts of the AICPA Code of Professional Conduct are principles, rules of conduct, interpretations of the rules of conduct and ethical rulings.

What are the 5 basic principles in professional ethics?

It is divided into three sections, and is underpinned by the five fundamental principles of Integrity, Objectivity, Professional competence and due care, Confidentiality, and Professional behaviour.

What is the aicpa code of ethics?

The AICPA Code of Professional Conduct (AICPA Code) is a set of principles, rules and interpretations that guides CPAs in the performance of their professional responsibilities. A national effort is underway to encourage more state boards of accountancy to adopt the robust ethical standards in the AICPA Code.

What is general standard rule?

General Standards Rule (AICPA) Undertake only those professional services that the member or the member’s firm can reasonably expect to be completed with professional competence. (b) Due Professional Care. Exercise due professional care in the performance of professional services. (c) Planning and Supervision.

What are codes of professional conduct?

The code of professional conduct sets out the elements of professional standards and ethical considerations, which the Institute requires from members and shall be binding on all members of the Institute.

What is aicpa code ethics?

What are the ethical principles of accounting?

The fundamental principles within the Code – integrity, objectivity, professional competence and due care, confidentiality and professional behavior – establish the standard of behavior expected of a professional accountant (PA) and it reflects the profession’s recognition of its public interest responsibility.

What is the purpose of the aicpa code?

The AICPA Code of Professional Conduct (AICPA Code) is a set of principles, rules and interpretations that guides CPAs in the performance of their professional responsibilities.

What is the compliance with standards rule?

When a member is engaged to perform a professional service that, based on his or her professional judgment, cannot be covered by established standards, the member will not be considered to be in violation of the “Compliance With Standards Rule” if only the alternative standards are applied.

What is an example of professional conduct?

Examples of professional behavior include, but are not limited to: Showing compassion for others; responding appropriately to the emotional response of patients and family members; demonstrating respect for others; demonstrating a calm, compassionate, and helpful demeanor toward those in need; being supportive and …

The principles are: Responsibilities Principle, The Public Interest Principle, The Integrity Principle, Objectivity and Independence Principle, Due Care Principle, and the Scope and Nature of Services Principle.

What is prohibited by the AICPA Code of Professional Conduct?

The AICPA Code of Professional Conduct states that a CPA shall not disclose any confidential information obtained in the course of a professional engagement except with the consent of the client.

What are the purposes of the three parts of the AICPA’s code of professional conduct?

The code establishes standards for auditor independence, integrity and objectivity, responsibilities to clients and colleagues and acts discreditable to the accounting profession. The AICPA is responsible for drafting, revising and reissuing the code annually, on June 1.

What are the AICPA Code of Professional Conduct rules?

Additionally, all AICPA members are required to follow a rigorous Code of Professional Conduct which requires that they act with integrity, objectivity, due care, competence, fully disclose any conflicts of interest (and obtain client consent if a conflict exists), maintain client confidentiality, disclose to the …

Which of the following is most likely to violate the aicpa code?

A member firm buys computer time at wholesale prices from another CPA firm and sells it at retail prices to clients is most likely a violation of the AICPA Code of Professional Conduct because it violates basic principles of integrity, scope and nature of services of CPAs.

What are the principles of Professional Conduct?

Where can I download the AICPA Code of Professional Conduct?

PDF Versions of the AICPA Code of Professional Conduct are also available for download. Additional archives of the Code of Professional Conduct can be viewed in the University of Mississippi Libraries, Digital Accounting Collection.

What are the rules and principles of the AICPA?

The code consists of principles and rules as well as interpretations and other guidance which are discussed in 0.100.020. The principles provide the framework for the rules that govern the performance of their professional responsibilities. .02 The AICPA bylaws require that members adhere to the rules of the code.

Is there a redesigned Code of Professional Conduct?

Learn more about the Project that resulted in the redesigned Code of Professional Conduct. A national effort is underway to encourage more state boards of accountancy to adopt the robust ethical standards in the AICPA Code. Video Player is loading. This is a modal window.

What is a threat to an AICPA member?

A threat that, due to a long or close relationship with a client, a member will become too sympathetic to the client’s interests or too accepting of the client’s work or product. A threat that a member will take on the role of client management or otherwise assume management responsibilities]