What are the method for apportionment of joint costs to joint product?

Emily Baldwin

Emily Baldwin

(a) Physical Units Method: Under this method the joint costs are apportioned among the joint products in the ratio of physical units of output produced at the point of separation. For example, the physical base like raw material weight in physical quantity is used as the base for apportioning the joint costs.

What is joint product in cost accounting?

Joint products are multiple products generated by a single production process at the same time. These products incur undifferentiated joint costs until a split-off point, after which each product incurs separate processing. Prior to the split-off point, costs can only be allocated to the joint products.

How is joint product treated in cost accounts?

The costs incurred in the process are shared between the joint products alone. The by-products do not pick up a share of the costs, like normal loss. The sales value of the by-product at the split-off point is treated as a reduction in costs instead of an income, again just the same as normal loss.

What methods can be used to allocate joint costs to main products?

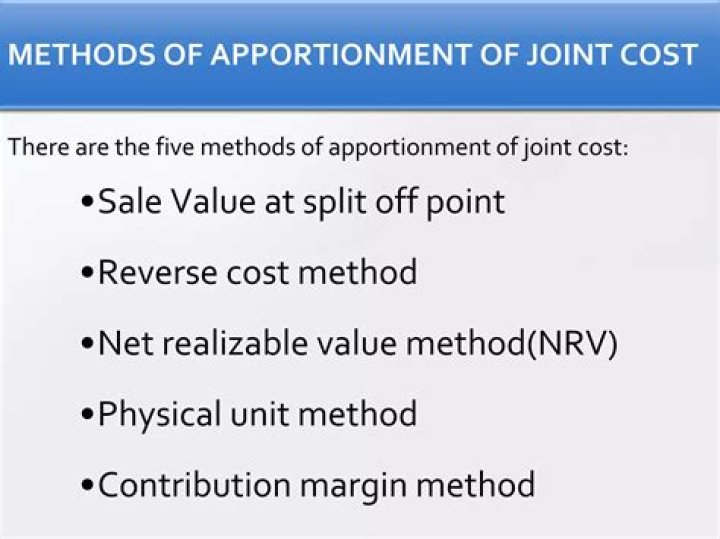

Three methods of allocating joint product costs are the physical units method, the market value method, and the net realizable method. The constant gross margin percentage method is also used to allocate joint cost.

What will justify the treatment of a product as a joint product?

Justification of the treatment of joint product as by-product: A joint product is normally treated as a by-product if its sales value is relatively minor compared to other joint products.

Which is an example of joint product?

Joint products are two or more products that are generated within a single production process; they cannot be produced separately and incur undifferentiated joint costs. Examples of join products include: Milk – butter, cream, cheese. Crude oil – fuel, gas, kerosene.

What is accounting for by-product?

Accounting for by-products There are two ways of accounting for a by-product: the production method and the sales method. Under the production method, product’s sales value is recognised in the accounting period in which the product is produced, and the by-product is considered as inventory.

Which is an example of joint products?

Examples. The processing of crude oil can result in the joint products naphtha, gasoline, jet fuel, kerosene, diesel, heavy fuel oil and asphalt, as well as other petrochemical derivatives. The refinery process has variable proportions depending on the distilling temperatures and cracking intensity.

Why do organizations allocate joint costs?

With so much attention these days paid to fundraising ratios, many nonprofits feel pressure to minimize their fundraising expenses. This makes allocating joint costs — costs associated with activities that have both fundraising and other functions — appealing.

What are joint costs and how are joint costs recorded?

A joint cost is the cost of a single production process that yields multiple products simultaneously. The purposes for allocating joint costs to products include inventory costing for financial accounting and internal reporting, cost reimbursement, insurance settlements, rate regulation, and product-cost litigation.

There are two main methods of apportioning the common process costs at the split-off point: Physical measurement (weight or volume) of output. Market value (sales or net realisable value) of output. The apportionment of common process costs between joint products is arbitrary whichever method is used.

There are two common methods for allocating joint costs. Add up all production costs through the split-off point, then determine the sales value of all joint products as of the same split-off point, and then assign the costs based on the sales values.

What are joint products in cost accounting?

Joint products are multiple products generated by a single production process at the same time. These products incur undifferentiated joint costs until a split-off point, after which each product incurs separate processing.

What are examples of joint products?

Should we allocate joint costs among joint products?

Key Takeaway. Two or more products made from a single input are called joint products. The costs of the single input and related manufacturing process costs must be allocated to each of the joint products.

How are joint costs allocated in cost accounting?

In this method, joint costs will be apportioned to the products in the ratio of selling price of respective individual products. The rationale underlying this approach is that product with higher sales value should be allocated with a larger proportion of joint costs than the products with lower sales value.

How are joint products valued in an accounting?

Under this method, the total units produced at that point divide the total cost incurred up to the split-off point to get average cost per unit of production. All joint products are valued at the average cost. This method can be used when all products are expressed in terms of same units.

How to calculate joint and byproduct production costs?

The calculation methods are as follows: Allocate based on sales value. Add up all production costs through the split-off point, then determine the sales value of all joint products as of the same split-off point, and then assign the costs based on the sales values.

What’s the difference between by-product costing and joint product costing?

By-product costing and joint product costing. A joint cost is a cost that benefits more than one product, while a by-product is a product that is a minor result of a production process and which has minor sales.