What do you need to know about sole proprietorship?

Emma Jordan

Emma Jordan

Proof of Sole Proprietorship Ownership A sole proprietor is someone who owns a business individually. They have not separated the business from the owner’s tax or legal liabilities. It is possible that the business is under a different name than the individual, often known as a doing business as (DBA) name.

How to transfer sole proprietorship from father to son?

There are some legal ways to accomplish the transfer of proprietorship from father to the son. The present owner of the business has to execute gift deed or quitclaim deeds in favor of the new owner who is the son in this case. All the assets of the business are to be listed out in the deed to avoid any confusions at a later stage.

What happens to father’s assets after sole proprietorship?

ALL the residual Legal Heirs (children) of Father, can execute a registered “Release Deed” in favor of Mother, permanently relinquishing all their rights over all property, including Prop. Firm, alongwith Assets & Liabilities, floating & fixed Stocks, all relevant licenses & permits etc…. 2.

Who is responsible for the debts of a sole proprietorship?

Sole proprietors are personally liable for all debts of a sole proprietorship business. Let’s examine this more closely because the potential liability can be alarming. Assume that a sole proprietor borrows money to operate but the business loses its major customer, goes out of business, and is unable to repay the loan.

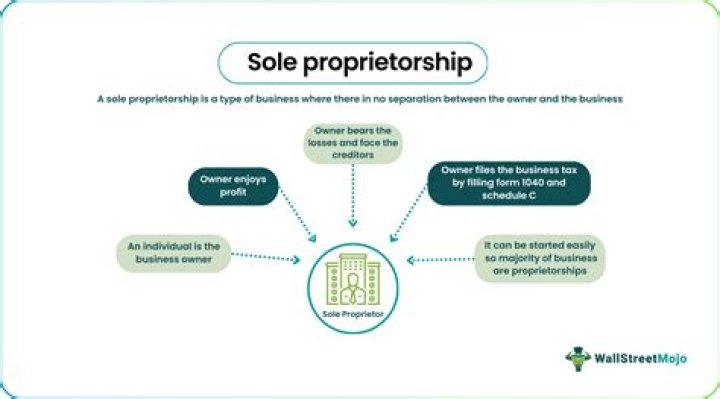

A sole proprietorship is the simplest and most common structure chosen to start a business. It is an unincorporated business owned and run by one individual with no distinction between the business and you, the owner. You are entitled to all profits and are

What is the tax rate for a sole proprietorship?

According to the balance small business, sole proprietorships face a 13.3% tax rate. It’s in your best interest as a sole proprietor to use and maximize the tax deductions. They’ll lessen your tax burden, allowing you to invest that money in your business. Filing taxes as a sole proprietor isn’t easy, but don’t worry.

What are the risks of being a sole proprietor?

Because there is no legal separation between you and your business, you can be held personally liable for the debts and obligations of the business. This risk extends to any liabilities incurred as a result of employee actions. Hard to raise money. Sole proprietors often face challenges when trying to raise money.

Is it hard to raise money for a sole proprietorship?

Hard to raise money. Sole proprietors often face challenges when trying to raise money. You cannot sell stock in the business, which limits investor opportunity. Banks are also hesitant to lend to a sole proprietorship because of a perceived additional risk when it comes to repayment if the business fails.

Who is the sole owner of a business?

A sole proprietorship, also known as a sole trader or a proprietorship, is an unincorporated business with a single owner who pays personal income tax on profits earned from the business.

How does a sole proprietorship form a LLC?

Usually, when a sole proprietor seeks to incorporate a business, the owner restructures it into an LLC. In order for this to work, the owner must first determine that the name of the company is available. If the desired name is free, articles of organization must be filed with the state office where the business will be based.

Which is the simplest form of business ownership?

A sole proprietorship is the simplest form of business ownership. Not surprisingly, the vast majority of small businesses begin their existence as sole proprietorships. A sole proprietorship has but one owner. That sole owner may engage in any form of legal business activity any time and anywhere.

Can a sole proprietorship be registered as a corporation?

Forming a Sole Proprietorship. From the IRS’s perspective, your small business is a sole proprietorship unless you have registered it as a corporation or other business structure such as an LLC. Setting up your proprietorship often does not require registration of the business.

Can a business be taxed as a sole proprietorship?

Incorporated businesses have the ability to be taxed as a pass-through entity formation. If they are not already this formation, they may elect a pass-through entity such as an S Corporation. Sole proprietors, on the other hand, are also responsible for reporting all income on their tax returns.

What are the pros and cons of sole proprietorship?

Learn the pros and cons of a doing business as a sole proprietorship. A sole proprietor is a business of one without a corporation or limited liability status. The individual represents the company legally and fully. Common proprietorship structures include part-time businesses, direct sellers, new start-ups, contractors, and consultants.

Can a sole proprietorship produce a separate business entity?

Sole proprietorships do not produce a separate business entity. This means your business assets and liabilities are not separate from your personal assets and liabilities. You can be held personally liable for the debts and obligations of the business.

Do you have to register your business as a sole proprietor?

Set up a business checking account so you don’t mix up business and personal spending. In addition, your sole proprietorship may have to register with federal or state entities (these registrations are the same for all types of businesses):

What are the costs of a sole proprietorship?

When setting up a sole proprietorship, there are some associated costs involved, depending on the type of business you’re starting. At the state and federal levels, there are licensing fees. Over time, other costs include business taxes, operating costs, and capital improvements or equipment purchases, among other things.

How to prove you are the sole owner of a business?

Between tax returns, business entity filings and stock logs, you should have all the documentation required to prove you are the sole owner of the business. Company financial statements may also show that no other parties are receiving profits from the company. Internal Revenue Service (IRS).

How are sole proprietorships reported on a tax return?

Sole Proprietor Taxes Because you and your business are one and the same, the business itself is not taxed separately-the sole proprietorship income is your income. You report income and/or losses and expenses with a Schedule C and the standard Form 1040. The “bottom-line amount” from Schedule C transfers to your personal tax return.

Can a sole proprietorship sell stock in the business?

Sole proprietors often face challenges when trying to raise money. You cannot sell stock in the business, which limits investor opportunity. Banks are also hesitant to lend to a sole proprietorship because of a perceived additional risk when it comes to repayment if the business fails.

Sole proprietorships do not produce a separate business entity. This means your business assets and liabilities are not separate from your personal assets and liabilities. You can be held personally liable for the debts and obligations of the business. Sole proprietors are still able to get a trade name.

What are the limitations of a sole proprietorship?

Some of the primary limitations of a sole proprietorship are as follows: Resources of a sole proprietor are limited to his savings and borrowings from the relatives. Banks also hesitate or deny giving the long term loans or extend the limit of long term loans due to the weak financial position of the business.

How to report income from a sole proprietorship?

Report income or loss from a business you operated or a profession you practiced as a sole proprietor. Also, use Schedule C to report wages and expenses you had as a statutory employee. Report farm income and expenses. File it with Form 1040 or 1040-SR, 1041, 1065, or 1065-B.

When do you become a sole proprietor or DBA?

You’re either a sole proprietor or a DBA (doing business as), and the bureaucracy surrounding both of those is minimal. If you’re doing business under your own name and you’re the only person who works for you — say, a freelance writer, designer, or painter — you are automatically a sole proprietor.

What are the challenges of being a sole proprietor?

Sole proprietors often face challenges when trying to raise money. You cannot sell stock in the business, which limits investor opportunity. Banks are also hesitant to lend to a sole proprietorship because of a perceived additional risk when it comes to repayment if the business fails. Heavy burden.

When does a sole proprietorship have to pay taxes?

When you operate as a sole proprietorship: With a sole proprietorship, even the money you leave in your business bank account is taxed in the year it is earned. That remains true even if you are saving it to pay for business expenses in the coming year.

In the sole proprietorship business, the sole owner has unlimited liability. In this case, the owner is himself liable to pay all the liabilities. If he takes a loan for its business then he will be liable for all the debts. Hence, he is personally liable for all the debt which can be recovered by his personal estate when funds are insufficient.

A sole proprietorship is a business started and owned by an individual. Little or no legal paperwork is required to begin, other than any necessary professional or local business licenses. Operating as a sole proprietor is one of several common options to start your business.

How much money do you need to start a sole proprietorship?

Typically, with other business setups, company income is taxed and you take out taxes from your personal share of the profits. While the nature of your business may dictate a need for more funds, some people start a sole proprietorship for no more than a few hundred dollars.

What are the disadvantages of sole proprietorship?

With no co-owners or partners, the sole proprietor can sell the business or close the doors at any time, making this form of business organization an ideal way to test a new business idea. Along with the freedom to operate the business as they wish, sole proprietors face several disadvantages: Unlimited liability.

Can a business close down under sole proprietorship?

If you choose to run your business under the sole proprietorship for of entity, then you can cease to operate or close down the business without any legal formalities. In conclusion, these are the seven major reasons why most businesses are operated under the sole proprietorship type of entity.

Do you have to register as a sole proprietorship?

#1 Registering your sole proprietorship as a DBA is the easiest and most affordable way to attract business and get recognized by customers. By taking this approach, you can crate a distinct professional business image without the need to form a corporation or limited liability company (LLC).

Who was the sole proprietor of eBay?

Pierre Omidyar, founder of the online retail giant eBay, started as a sole proprietor, reportedly because he wasn’t sure his business was going to make it big. Omidyar went from a sole proprietor business model to going public and earning millions, all in three short years.

How to establish a sole proprietorship in New Hampshire?

In New Hampshire, you can establish a sole proprietorship without filing any legal documents with the New Hampshire state government. There are four simple steps you should take: Choose a business name. File a trade name with the Secretary of State. Obtain licenses, permits, and zoning clearance.

Can a sole proprietorship be transferred to another party?

A sole proprietorship cannot be transferred to another party. However, it may able to have its assets transferred to a new owner. The new business owner must have his own separate legal business structure in order to receive the assets.